Total spending grew 0.9% in June.

Inflation is back in focus with European inflation at its highest ever level of 8.1% y/y helping rates extend yesterday’s selloff.

https://soundcloud.com/user-291029717/eu-sanctions-more-in-the-pipeline?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Inflation is back in focus with European inflation at its highest ever level of 8.1% y/y helping rates extend yesterday’s selloff. Higher inflation and higher yields helped a cautious tone in equity markets with US equities failing to continue the rebound last week. Comments from ECB officials still tend to emphasise a gradual approach to end negative rates by Q3. US President Biden, in a rare meeting with Fed Chair Powell, emphasised the Fed’s independence and said that he would give the Fed “the space they need to do their job.”

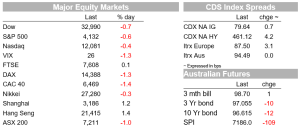

The S&P500 was down 0.6% on Tuesday, failing to extend last week’s rally after markets were closed for Memorial Day on Monday. That leaves the index broadly flat for month of May, after a sharp 8.4% recovery from flirting with a bear-market defining 20% decline on 21 May. The Nasdaq was 0.4% lower, while the Dow lost 0.7%. European stocks were lower, the Euro Stoxx 50 down 1.4%.

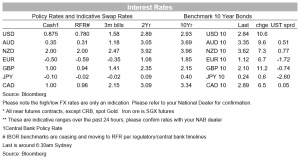

Bond yields were higher, extending yesterday’s moves. German 10yr yields were 7bp higher at 1.12% and Italian yields were up 12bp to 3.12%, extending yesterday’s rise to their highest since 10 May. US yields followed Europe higher, with the US 10yr 12bp higher to 2.86% and the 2yr 8bp higher to 2.56%. The US dollar gained against most G10 currencies. Higher yields helped the yen lower, with the dollar 0.9% higher against the currency to 128.7. Elsewhere, currency market moves were mostly modest. The AUD was 0.3% lower at 0.7178. The currency hit a high of 0.7204 in our morning yesterday, before choppy price action saw it as low as 0.7150 overnight. The euro lost 0.4% against the dollar.

The main data was Euro area inflation coming in 0.8% m/m and 8.1% y/y in May. That was above the consensus forecast for 0.6% m/m rise, but had been well telegraphed by higher German and Spanish upside surprises earlier in the week. High food and energy prices were the key driver, but the closely watch core measure also outpaced expectation, rising 3.8% y/y against forecasts for 3.6%y/y, a sign cost pressures are bleeding more broadly into the inflationary backdrop. Energy prices increased 39.2% y/y and food, alcohol and tobacco rose 7.5 y/y.

ECB Speakers were generally in line with recent comments pointing to 25bp hike in July and September as the ‘benchmark’ pace. De Cos said that the ECB can exit negative rates by the end of Q3, but the aim is to avoid abrupt movements and emphasised rate increases should be gradual. Visco said that the rate-hike pace must be orderly to avoid stress, noting that wages growth has been moderate so far. Slightly more hawkish comments came from Kazimir, who said he is open to talk about 50bp, saying in an interview with Reuters “I expect that we will go with 25 in July, then the 50 basis points could be in September. What’s important for me is to start hiking in July. The time for waiting, lingering, is gone. ” Kazimir indicated concern about second round effects and pinned neutral at somewhere between 1-2%, but closer to 2%. In contrast, De Cos suggested the natural rate was around 1%.

The EU found in-principle agreement to ban Russian crude and refined fuels that arrive on ships, which account for at least two-thirds of imports from Russia, with oil from pipelines exempted to get the agreement over the line. By the end of the year, with Germany and Poland stopping buying oil via pipelines, the embargo would cover 90% of previous Russian oil imports, EU officials said. The measures would also block insurers from covering Russian cargoes of crude anywhere in the world. In other energy news, the WSJ reported that some OPEC members were exploring exempting Russia from an oil supply deal, which could allow OPEC members to expand production. Brent Oil was 1.2% lower to $116.2.

US Conference Board Consumer confidence dipped to 106.4 from 108.6, a little less than the 103.8 expected. Despite further weakening, the Conference Board measure continues to hold up better than the University of Michigan gauge, which puts more weigh on personal financial situation and less on business and labour market conditions. The present situation gauge fell to 149.6 from 152.9, helped by some perceived softening in labour market conditions with differential of those saying jobs are easy vs hard to get down 5.4-points to a still-elevated 39.3. Perhaps an indicator of some welcome give at the margin in US labour market tightness? The measure covering consumers’ short-term outlook fell to 77.5 from 79.

China PMIs came in a little stronger than expected. The official Manufacturing PMI rose from 47.4 to 49.6 (49 expected). That’s still in contraction territory, but much milder than recent months. Virus containment measures continue to play a part, with some containment measures remaining and supply chain disruptions evident in lengthening delivery times and inventories drawdown. With Authorities still focussed on strict virus control, any recovery in activity remains on shaky ground. Easing virus containment measures in much of the country also helped the service index up to 47.1 from 40.0. The Caixin manufacturing PMI is coming up today, and the services PMI in Monday.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.