Online retail sales growth slowed in May following a fairly strong April

Insight

Reaction to a strong set of US data releases has been the main story overnight

https://soundcloud.com/user-291029717/rates-boosted-as-strong-data-support-aggressive-fed-hikes?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

US equities started the new month on the back foot with solid economic news unsettling investors. The US ISM beat expectations and the JOLTS report reaffirmed tightness of US labour market, the solid data releases supported the notion of a hawkish Fed, a view that was reinforced by JPM Dimon warning to prepare for an economic hurricane. UST have led a move up in core global bond yields and the USD is broadly stronger, although the AUD and CAD have held their own with the latter supported by a hawkish BoC, hiking by 50bps overnight and prepared to act more forcefully ahead.

Reaction to a strong set of US data releases has been the main story overnight. The US ISM manufacturing beat expectations, climbing to a solid 56.1 from 55.4 and against expectations for a decline to 54.5 . Looking at some of the details within the survey, the prices paid index moderated to 82.2, down on the previous month but still consistent with extremely strong inflationary pressures, while the employment index fell below 50 for the first time since late 2020, indicating, at face value, negative employment growth in the manufacturing sector. The services sector is the big US employer so it will be important to see what the Services ISM reveals on Friday.

US activity tends to lag what happens in China by about 3 months, so the strength in the ISM in May to some extent reflects what was going on in China around February. So, looking ahead some moderation in activity should be expected given the contraction in China activity over April and May with the impact on supply delays also likely to manifest themselves over coming months.

That said whatever that impact may be, the US economy starting point is a strong one with the JOLTS report overnight also reinforcing the notion that the US labour market remains very tight . Job openings in the US fell slightly in April, albeit to still exceptionally high levels. There are almost two job openings for every unemployed person in the US. Fed Chair Powell specifically referenced the job openings to unemployed ratio as one indicator he is watching for some early evidence of a potentially cooling in the labour market, and clearly there is no cooling yet.

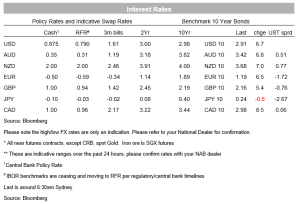

The idea that Central Banks will need to step up their pace of tightening given a backdrop of solid activity, high inflation and tight labour markets was further reinforced overnight after the Bank of Canada delivered a 50bps hike and a very hawkish forward guidance . Canada’s official cash rate was lifted to 1.50% overnight with the Bank noting inflation had come in much higher than expected while “the risk of elevated inflation becoming entrenched has risen” and “the economy is clearly operating in excess demand”. Then in no uncertain terms the statement made it very clear that the Bank “is prepared to act more forcefully if needed to meet its commitment to achieve the 2% inflation target,”. Canadian short-term rates blasted higher, with the market now attaching a moderate probability to a 75bps hike in July (~20% priced) and pricing a terminal rate of around 3.20%.

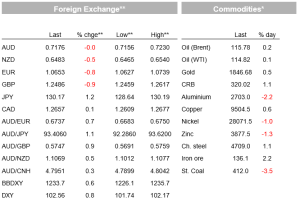

Reaction the solid US data releases triggered a sell-off in US Treasuries with yields jumping by about 9 to 10bps in the 2 to 5 year part of the curve while after trading to an overnight high of 2.9496%, 10y UST yields settled at 2.9060%, still 6.5bps higher on the day. Meanwhile in Europe, Germany’s 10-year rate was 7bps higher, closing at its highest level since 2014 at 1.19%.

Supporting the move up in global yields, oil prices have remained in the ascendency with spot Brent up close to 2% to $122.61 while the August contract gained over 1% to $115.79. The move up in oil prices took place ahead of the OPEC+ meeting today at which the cartel is expected to agree to another 430k increase in supply from July, as it continues to slowly rebuild production levels after the pandemic. The market has been seemingly unruffled by reports from earlier in the week that Russia could be suspended from OPEC+ production caps, which some have suggested could possibly allow Saudi Arabia to make up for the shortfall.

China’s reopening has been another theme playing into the expected increase in oil demand. Amid ongoing concern of a slowdown in activity, overnight Beijing ordered state-owned policy banks to set up an 800 billion yuan ($120 billion) line of credit for infrastructure projects as it leans on construction to stimulate an economy battered by coronavirus lockdowns.

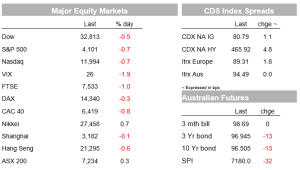

The move up in UST yields rattled US equity markets with all major US equity indices heading south after the stronger than expected data releases. The S&P 500 trading down to an intraday low of around -1.8%, but then recovered before the close to end the day at -0.75% while the NASDAQ closed -0.72%. Equity investors have been rattled by the prospect of an aggressive Fed given the strength of the US economy, playing into this theme comments from JPM Dimon added fuel to the uncertainty with the Bank’s CEO warning investors to prepare for an economic “hurricane” as the economy struggles against an unprecedented combination of challenges, including tightening monetary policy and Russia’s invasion of Ukraine. Financials were notable underperformers overnight, down 1.67% with JPM shares down 1.75%. Earlier in the session the Europe’s Stoxx 600 Index extended its declines in the wake of Tuesday’s stronger than expected euro-zone CPI figures, the index closed 1.04% lower.

The USD is broadly stronger on the back of the increase in Fed rate hike expectations (Dec Fed funds rate now seen at 2.80%, up ~5bps ) and as risk sentiment turns more cautious. The higher rates backdrop has seen USD/JPY (+1.1%) break above the 130 mark for the first time in four weeks while the EUR has fallen to around 1.0650. The commodity currencies have held in better, with the Bank of Canada’s hawkish policy update helping the CAD appreciate around 0.1% and the AUD up by a similar amount and now trading at 0.7175, after trading to an overnight high of 0.7230. The NZD is just below 0.65, down around 0.4% over the past 24 hours but slightly higher than it was at the NZ market close.

ECB Governing Council member – and one of the hawks on the committee – Holzmann reiterated his call for a 50bps rate hike in July, calling for “decisive action” to reduce the risk that inflation expectations become unanchored. Holzmann added that a 50bps hike would help support the EUR, noting that the downtrend in the currency was exacerbating inflationary pressures in the region. The committee still seems fairly split between the hawks, such as Holzmann, arguing the case for aggressive and frontloaded action and the more moderate members, such as President Lagarde and Chief Economist Lane, who appear to prefer the standard 25bps rate hike pace. Deutsche Bank is now calling for a 50bps ECB hike in either July or September while the market is pricing just under a 50% chance of a 50bps ECB hike in July. The increase in ECB rate hike expectations hasn’t done much to support the EUR overnight, however.

Lastly the Fed Beige book was also out last night reporting a mixed picture from regional anecdotes. Four of the twelve regions explicitly highlighted a slowdown in the pace of economic growth while labour shortages were noted as the main difficulty facing businesses at present. Inflation was “strong or robust” across all the regions although three regions observed some moderation in price pressures. Meanwhile, San Francisco Fed President Daly voiced her support for getting the cash rate to neutral quickly, including 50bps hikes at the upcoming two meetings, with the policy outlook beyond that point to be guided by the data. Fed Bullard was also out speaking reiterating his call to policy makers to raise interest rates aggressively to bring down inflation adding that the Fed credibility is at stake, noting “This situation is risking the Fed’s credibility with respect to its inflation target and associated mandate to provide stable prices in the US”.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.