NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Markets took the strong US payroll gains on Friday as affirming the near-term path for continued Fed tightening.

Markets took the strong US payroll gains on Friday as affirming the near-term path for continued Fed tightening. Good news was bad news, then, for risk assets with US equities lower. The report showed a solid but slower 390k jobs gain for May as the unemployment remained at 3.6% with gains filled from returning participation. Hourly earnings growth steady at 0.3% m/m.

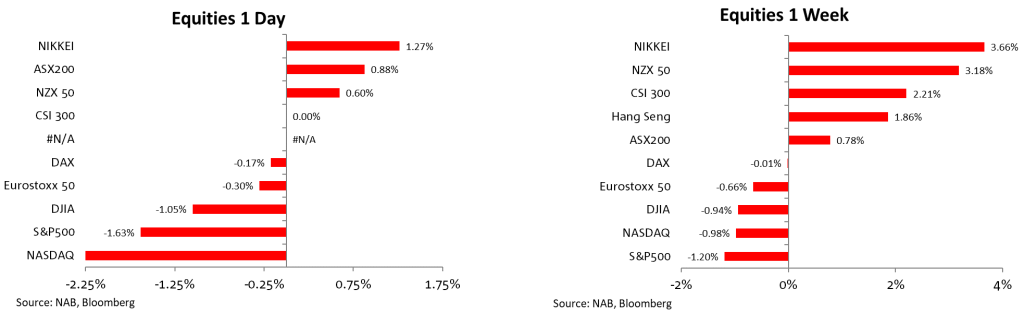

The S&P500 fell 1.6% on Friday, back into negative territory for the week after solid gains on Thursday. The index ended the week 1.2% lower, its 8th weekly decline of the last 9 weeks, interrupted only by last week’s 6.6% gain. The S&P500 is now 14.7% off its January highs, after recovering 7.8% from its 20 May intraday low. Friday’s declines were led by consumer discretionary and IT, while energy bucked the trend, managing a 1.4% gain as oil prices rose. The Nasdaq was 2.5% lower on Friday to be 1.0% lower over the week. Tesla shares weighed on Friday, down 9.2% after Elon Musk signalled the company may need to cut around 10% of its workforce. Asian shares outperformed over the week. The Nikkei up 3.7%, with other Asian bourses also in the green.

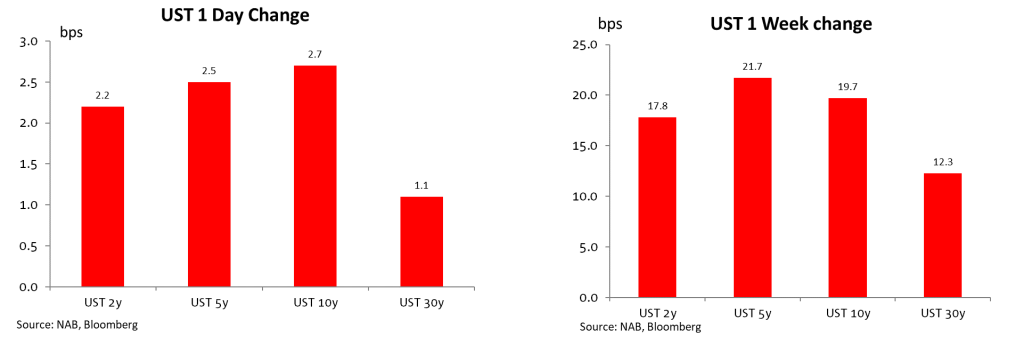

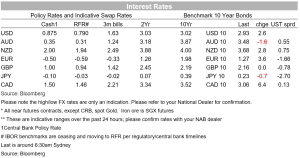

The US 2yr yield bounced 6bp higher on the payrolls release but ended the day just 2bp higher. Moves in rates were larger looking over the week . In the US, yields were higher across to curve, with the 2yr 18bp higher, the 10yr up 20bp, and the belly outpacing those moves with the 5yr up 22bps. Markets stepping back from hopes of a reprieve from consecutive 50bp hikes at the September Meeting that helped yields lower last week. Futures markets are pricing 143bps of tightening over the next three meetings, 10bp more than a week ago. European yields moved further than their US counterparts. The 10yr Bund was 4bp higher on Friday to 1.27%, up 31bp over the week. European spreads widened, with Italian bonds up 10bp on Friday and 51bp over the week to 3.40%, its highest since 2018.

Comments on Friday from Cleveland Fed’s Mester reiterated support for 50bp moves at the next two meetings. As for September, it’s a decision of whether to go 25bp or 50bp, saying “if I don’t see compelling evidence, then I could easily be a 50 basis-point in that meeting as well.” Mester’s comments were the last scheduled comments from fed officials ahead of the 14-15 June meeting.

As for the Payrolls data, still solid job growth, ongoing recovery in participation, and no further acceleration in wages growth made for positive reading. Together they indicate a robust US labour market and contain nothing to dissuade the Fed in the near-term. Non-farm payroll growth of 390k was stronger than the 318k consensus, but a little lower than the 428k gain in April. The marginal slowing from April “a good thing ” according to Mester, but too soon to change the outlook on policy. The household survey showed a similar 321k jobs gain. The participation rate rose a tenth to 62.3% and the unemployment rate was steady at 3.6% as jobs growth was filled by continued return of people to the labour force as labour supply continues to recover. Importantly, average earnings per hour grew 0.3% m/m against expectations for a 0.4% rise. That was weighed down by a slowdown in growth in wages for supervisory worker, but nonetheless leaves the door ajar to a soft landing for the Fed.

In other data on Friday, the US Services ISM was a touch softer than expected at 55.9 from 57.1 (consensus 56.5). That was its lowest reading since February 2021 but the 24th consecutive month in growth territory. In the detail, prices paid fell back 2.5ppt from a record high in April, but firms continued to struggle to replenish inventories, the inventories figure slowing to 51.0 from 52.3. In Europe, retail sales for April fell 1.3% m/m, their first monthly drop this year and against expectations for a 0.1% m/m rise. That could overstate weakness in consumption amid a rebound in services spending. The decline was led by a 2.6% drop in food spending.

Market relevant news flow elsewhere has been reasonably quiet. In the UK, PM Boris Johnson reportedly expects a no confidence vote against his leadership as soon as this week. Beijing on Monday will further unwind restrictions, resuming public transport in most districts, and allowing workers to return to offices and restaurants to resume dining-in.

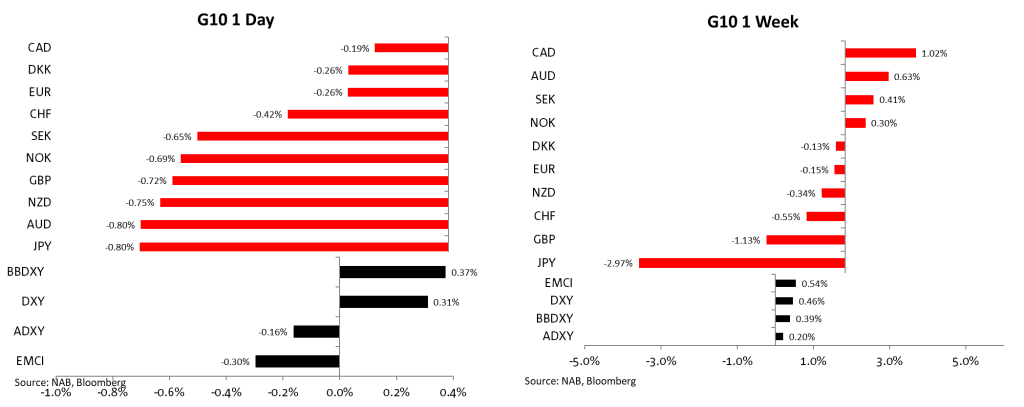

In currency markets, the US dollar was higher on Friday , up 0.3% on the DXY and gaining against all G10 currencies. Over the week, the dollar snapped a two-week losing streak to be 0.5% higher but remains 2.7% below its recent high on 13 June. The AUD was 0.8% lower to 0.7202 on Friday but held on to earlier gains to be 0.6% higher over the week. The dollar rose 0.8% against the yen on Friday and 3.0% over the week. That puts the pair back above 130 at 130.87, just shy of the 131.35 level reached on 5 May, which was a near two decade high.

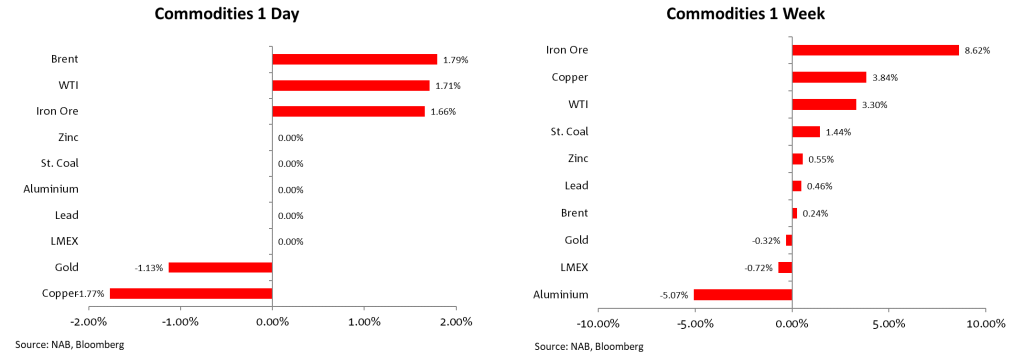

In Commodities, oil was higher on Friday , Brent gaining 1.8% to $119.7. Oil was little changed over the week. Iron ore (+8.6%) and copper (+3.8%) were higher over the week as easing of restrictions in China boosted expectations for demand. UK markets were closed at the end of last week for the Queens Platinum Jubilee. Of note over the weekend were comments from Vitol group, the biggest independent crude trader that the US may allow more sanctioned oil out of Iran even without a revived nuclear deal, while Reuters reported the US may allow shipments of Venezuelan oil to Europe.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.