On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Yields rose notably in what was a quiet night for data and events.

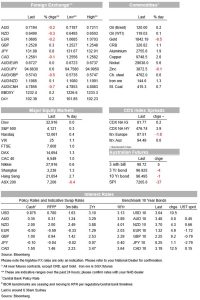

Yields rose notably in what was a quiet night for data and events. The US 10yr yield is up 10.5bps to 3.04% with most of the move reflected in real yields with the 10yr TIP yield +8.9bps to 0.26% and the implied inflation breakeven was little changed at 2.79%. Helping drive yields higher was higher corporate flow with firms expected to raise around $10bn, while the first Treasury auctions since the beginning of the Fed’s QT are also slated for this week (3, 10 and 30yr are planned). Ahead of the Fed next week markets are fully priced for 50bp hikes at the June and July meetings, and another 50bps hike is 88% priced for September.

Equities started the week with a positive tone too with the S&P500 +0.3%, though at one stage the index was up 1.5% before the move in yields weighed. Positive news out of China was the driver of the initial positivity with reports Chinese regulators were planning lifting restrictions on DiDi – taken as a signal that the authorities were pivoting away from the regulatory crackdown on tech and towards supporting the economy; Beijing also eased some Covid restrictions. Given key risk events later in the week of the ECB and US CPI, its likely markets will be treading water until then.

There has been little in the way of news. The UK PM survived a no-confidence motion vote by 211 vs. 148. GBP had lifted initially 0.6% on news of the leadership challenge, but has given up around half of its gains since the announcement of Johnson surviving to be up 0.3%. GBP though overall has been an outperformer in what has been a night of mild USD strength with DXY +0.2%. The AUD (-0.2%) and NZD (0.3%) have broadly moved in line with USD strength. The Yen also depreciated further with USD/Yen +0.8% to 131.89.

As for what drove the initial positivity yesterday, the WSJ reported that Chinese regulators were planning to lift restrictions on ride-hailing app Didi. This was seen as a signal that the regulatory crackdown on Chinese tech firms was starting to end as signalled last week, as China focuses on stabilising the economy following Covid restrictions. Chinese equities certainly saw it that was with the HK Tech Sector up some 5% and Shanghai was up 1.3%. Beijing also eased up on Covid restrictions with public transport to resume in most of Beijing, which will allow most workers to return to the office, while restaurants and cinemas in the city will be allowed to reopen.

A weaker than expected Caixin Services PMI (41.4 vs. 46.0 expected and 36.2 previously) only had a fleeting impact given the ongoing easing in covid restrictions. It remains to be seen whether China can keep Omicron out, with Shanghai reporting three new cases out of quarantine on Sunday. Nevertheless commodities took their que from China with copper prices are 2.6% higher overnight and nickel 5% while the CSI300 equity index was almost 2% higher, symptomatic of less pessimism around the Chinese growth outlook.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.