Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Announcing the end of the Asset Purchase Programme (APP) as of July 1, the ECB also pre-announced a 25bps rise in interest rates out of its July meeting with a further rise planned out of the Sept meeting.

https://soundcloud.com/user-291029717/ecb-set-to-turn-up-the-dial?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

(incidentally, the only band who’s record sales went down after their (opening act) appearance at Live Aid – they were awful)

The ECB was obviously the main event overnight, the net result of which was higher Eurozone bond yields and a weaker Euro after an initial pop higher. But a couple of hours before that, a frisson of excitement came from a Bloomberg source report saying Chinese financial regulators have started early stage discussions on a potential revival of Ant Group Co.’s initial public offering. An hour or so later, China’s Securities Regulatory Commission (CSRC) said it was “not conducting a review and research work regarding Ant IPO revival, but that it supports eligible platform companies to list overseas”.

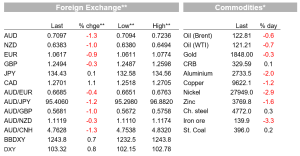

USD/CNH had fallen as much as 3 big figures to 6.665 on the original report, bur currently sits back above 6.70, aided by broad-based USD strength, in which respect the Bloomberg BBDXY’s index is up 0.7% and AUD/USD is opening in our time zone below 0.7100 amid sharp falls in global equity markets – the S&P500 has closed down 2.4% and the NASDAQ 2.75% – their worst day in 3 weeks. US rates market have been tracking broadly sideways ahead of the all-important US May CPI report tonight.

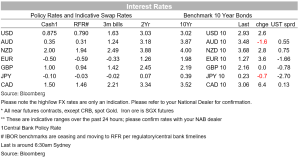

The ECB meeting didn’t throw up any big curved balls. Alongside announcing the end of the Asset Purchase Programme (APP) as of July 1, the ECB pre-announced a 25bps rise in interest rates out of its July meeting (so taking the Deposit Rate to -0.25%) with a further rise planned out of the September meeting, the size of which is said to depend on the updated medium-term inflation outlook at that time. This is currently interpreted as meaning 50bps is more likely than 25bps, and which is quite fully priced.

The ECB messaging, including that post September, they intended to enact a ‘series of hikes’, was interpreted as somewhat hawkish, EUR/USD rising to as high as 1.0774 from around 1.0720 pre-ECB and the 10yr Bund yields spiking by some 10bps to 1.46%. Yet while most (but not all) of the EZ yield back-up has held, the single currency quickly gave back its gain, and then some, ending in New York 0.9% lower on the day at 1.0617 (a three-week low).

Of some note here is that Euro-peripheral bond spreads have blown out, something historically associated with a weaker EUR, by some 15bps in Italy, following warnings by the ECB of increased fragmentation. While they stress the willingness to use the PEPP programme to alleviate stresses here (“PEPP reinvestments can be adjusted flexibly over time”) the post-ECB statement only refers explicitly to Hellenic (i.e. Greek) bonds. Hence, we would suggest, why Greek 10-year yields are only up 14bps on the day against 22bp for Italy.

In other news, US jobless claims rose by a higher than expected 229k last week and while the holiday shortened week and seasonal adjustment issues means not too much should be read into the rise, it does fit with anecdotal evidence of layoffs in various sectors and is consistent with the recent rising trend in claims.

Sharply weaker US equity market took their cue from European market which didn’t take kindly to the ECB’s messaging (including its warnings about fragmentation, albeit countered by the above PEPP references) comments. For the US, our BNZ colleagues note headlines about $5 gasoline prices ‘rippling through” the economy might have caught some attention, in which respect Janet Yellen has been out saying that while its ‘amazing’ how pessimistic consumers are given job gains, it’s unlikely gas prices will fall anytime soon.

For these or other reasons, including perhaps some pre-US CPI apprehension, US equities have endured their worst day in three weeks with loss of 2.75% for the NASDAQ and 2.4% for the S&P500, losses for the latter very broad based. 10 year Treasuries at 3.04% meanwhile, are 2bps up on the day.

The risk-off mood has been supportive of the USD with all G10 currencies lower, save that USD/JPY is barely changed, though this does mean it has pulled back up after losing a whole yen in late Asia/morning European trade. NZD, CAD, AUD and NOK all show losses on the day of 1% or more (EUR/USd a slightly lesser 0.9%) with BBDXY ending NY +0.7% and DXY +0.8%

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.