Online retail sales growth slowed in May following a fairly strong April

Insight

Overnight, the BoE’s Pill references ‘Matterhorn’ versus ‘Table Top Mountain’ approaches to monetary policy

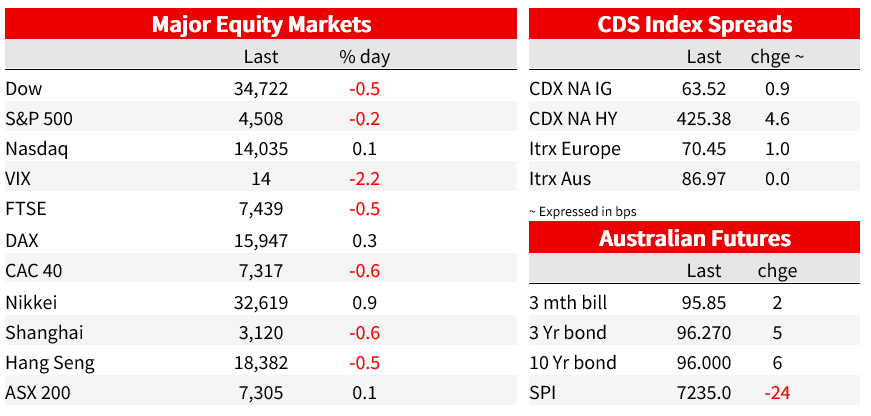

US equities are ending in New York narrowly mixed (S&P 500 -0.16%, NASDAQ +0.11%) after modest falls for all European bourses bar German (Dax +0.35%). Treasury yields are slightly lower with a mild bull steepening of the curve evident. In FX the DXY is up 0.5% thanks largely to losses for the EUR and GBP, in line with reduced pricing for ECB and BoE policy tightening this month, the former in particular but also in the UK following BoE chief economist Huw Pill’s mountain analogy to how UK rates policy could play out from here (more below). It’s US payrolls Friday, where after this week’s JOLTS data showing a big fall in job openings and a slower quit rate, the ‘whisper numbers’ for both non-farm payrolls and earnings growth will likely be on the low side of official consensus expectations, for 170k and 0.3% respectively.

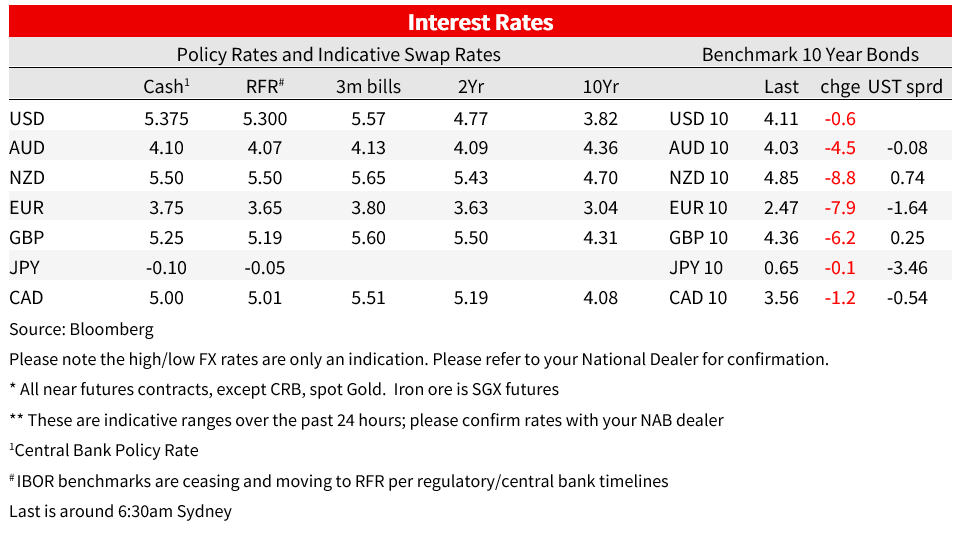

Plenty of data and central bank speak to digest overnight. After earlier German and Spanish data, Eurozone CPI came in at 0.6% against the earlier expected 0.4%, so no great shock, to keep the headline y/y rate at 5.3% against 5.1% expected, though core CPI still fell, to 5.3% from 5.5% in line with the earlier consensus so in the circumstances a pleasant surprise. .

Speaking after the data, ECB Vice President Guindos said the ECB’s new forecasts will show that the outlook for inflation hasn’t changed much over the summer even though prospects for the economy worsened. The data signal weaker economic activity in Q3 and maybe Q4, Guindos says, and that the September rates decision is still open and subject to data in the next few days. Earlier in the day, the ECB’s Schnabel (hawk) said underlying inflation pressures were stubbornly high but also that economic activity had moderated visibly. Monetary policy remains a meeting by meeting proposition in her view, such that she failed to offer a view on what should happen this month.

US July core PCE deflator rose by 0.2% as expected, lifting the annual rate to 4.3% from 4.2% also as expected. Note the market-based core PCE measure has been a benign at 0.12%, 0.10% in the last two months, down from 0.32% earlier, while market based overall PCE has been on a 0.1% handle for the last three months. Weekly jobless claims were a tad softer at 228k (235k expected) and versus 232k in the prior week. Likely still distorted a bit by auto sector annual re-tooling. Finally the MNI Chicago PMI rose to (still contractionary) 48.7 from 42.8, above the 44.2 expected.

Overnight, the PBoC and main financial regulator lowered the down payment requirement to 20% for first-time home buyers, in an effort to boost the property market, according to a joint statement. Separately, China approved a rate cut on existing mortgages for first homes effective Sep 25, according to a separate statement.

Just after our close yesterday speaking in South Africa, Bank of England chief economist Huw Pill said that service sector inflation is ‘developing less benignly’ and that the UK faces ‘second round’ (i.e. wages driven) effects and that the MPC needs to see the job through on inflation. He nevertheless admits to the possibility of doing much on rates and says a lot of rate hikes have yet to impact the UK economy.

While Pill’s comments appear consistent with another quarter-point turn of the screw on 21 September – but not necessarily thereafter – Pill later reference two scenarios for policy. One was what he called the ‘Matterhorn profile’ for rates (sharply up then down – hence referencing the large, pyramid shape peak in the Alps). A second scenario is one where rates are held restrictive for longer in a more steady but resolute way. Pill referred to this as the ‘Table Top mountain approach’ (not as high as the Matterhorn but long and flat at the top). Pill then noted the profile for CPI coming lower on both paths is almost exactly the same, adding “I would tend to follow the latter approach as it probably imposes fewer financial stability risks”. As such, while a September rise to 5.5% looks more likely than not, we shouldn’t now rule out a pause. Either way, a move to above 5.5% is looking less and less likely.

Other central bank speak overnight included the Atlanta Fed’s Bostic, a 2023 FOMC non-voter, speaking just after our local close, said rates are restrictive enough to see 2% inafltion but that he would support more tightening if inflation quickens.

The upshot of the Eurozone and UK data and central bank speak is that pricing for another 25bps hike from the ECB this month has come in from a little over 50% to a little under 25%, and for the BoE from a little over 100% to just under 90%.

Yesterday, Australia Q2 Capex reportedly rose 1.9% q/q, above NAB and consensus expectations for +1.0% q/q. Leading the increase was a 3.5% q/q increase in Buildings and Structures. However, it is Equipment, Plant and Machinery that feeds directly through to investment in Wednesday’s GDP outcome. This component rose 1.9% q/q and implies a 0.1ppt contribution to GDP growth in the quarter, a little stronger than NAB economists. They will publish its full GDP preview tomorrow, while additional partial indicators, including for trade and inventory contributions are released early next week ahead of Wednesday’s Q2 GDP release.

Released overnight, CoreLogic house price data for August showed price momentum picked backup last month, to 1.0% for the month for the combined capital cities, led by Sydney from 0.9% in July to 1.1%, with Melbourne 0.5% after 0.3%. The RBA has been on hold the past two months, improving mortgage rate optics, might be a relevant factor.

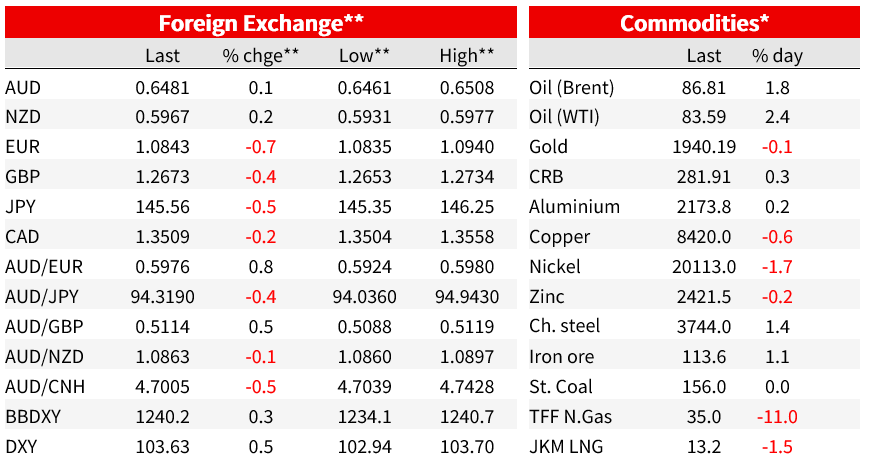

In FX, the biggest fallers overnight were EUR/USD (-0.7%) and GBP (-0.4%) in keeping with the previously mentioned downward repricing of September rate hike expectations, while USD/JPY dropped by 0.6% (to ¥145.42) which is somewhat outsized move relative to the less than 1bp fall in 10 year Treasuries, though we’d note 2-year yields are off a larger 2.5bps to 4.86%. European bond markets ended with yields 6-8bps lower everywhere (10-year Bunds and OATs -8bps, Gilts -6bps).

On AUD (+0.1% in the last 24 hours, ditto NZD) there is some evidence of AUD supply into the 4pm London fix, suggesting a need for some rebalancing of hedges on international assets given the weakness in global equity market last month. Yet AUD/USD slippage such as there was (down to 0.6461) was mostly recouped during the New York afternoon (back to above 0.6480).

Finally in commodities, crude oil benchmarks are up between $1.50 (Brent) and $1.90 (WTI) possibly helped by updated data from the US Energy Information Administration that oil demand in the US topped pre-pandemic level in both May and June. Gold is down $2.5 to $1940, base metals narrowly mixed save for a 1.7% drop for nickel while Dalian iron ore futures are up 0.24%

Coming Up

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.