Online retail sales growth slowed in May following a fairly strong April

Insight

US and European equities showed signs of stabilisation on Friday, but still ended with sharp declines on the week which was not helped by Fed Chair Powell's words that the Fed has unconditional commitment to restoring price stability.

https://soundcloud.com/user-291029717/turning-up-the-rhetoric?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

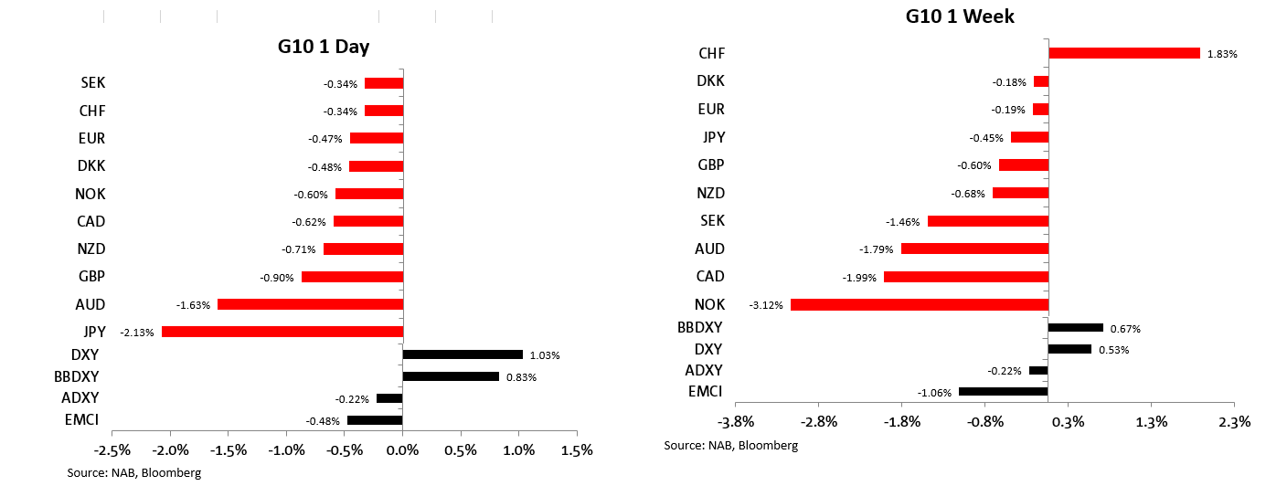

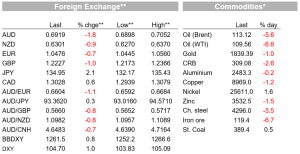

US and European equities showed sign of stabilisation on Friday, but still ended with sharp declines on the week. Sentiment was not helped after Fed Chair Powell said the Fed has unconditional commitment to restoring price stability. Remarks that were further reinforced over the weekend with Fed Governor Waller stressing he only cares about bringing inflation down, backing another 75bps hike in July. The US Treasury curve bear flattened on the day but closed the week with higher yields across all tenors. After two days of decline, the USD regained its mojo, stronger on the day and on the week too, JPY the big underperformer on Friday, NOK the big underperformer on the week with AUD not far behind down 1.8% over the past five days. Sharp declines in oil prices on Friday, amid recession concerns not helping commodity linked pairs while China’s uncertain recovery weighed on iron prices.

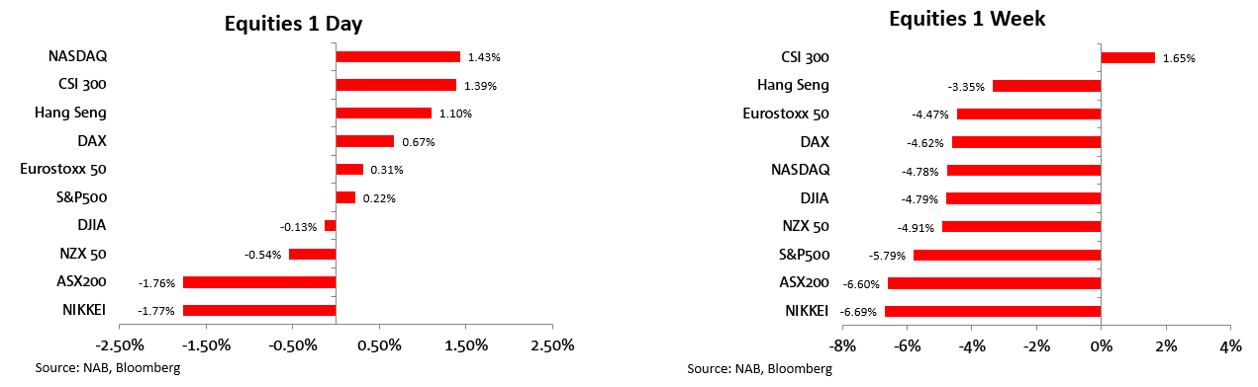

Equity markets showed signs of steadiness on Friday with the S&P 500 recording a very modest, but still positive return of +0.2%. The positive take would be that this could be an early indication for better fortunes ahead with six of the 11 index’s sectors recording gains on the day, with the communication services and consumer discretionary leading the gains. A look at the index’s performance for the week, however, tells a different story with the benchmark recording its biggest weekly decline since March 2020, down 5.79%. Market volatility has also remained elevated with the VIX index closing the week at 31.12, a theme that goes beyond equities with a spike in FX and rates volatility alongside wider credit spreads. Central Banks hawkish rhetoric and concerns over a global economic slowdown/recession, not helping sentiment and this stage it is hard to see a turn in fortunes until we see evidence of a material ease in inflationary pressures.

Looking at other US equity indices, the tech-heavy Nasdaq rose 1.2% on Friday but fell 4.76% on the week while in Europe, while the Stoxx Europe 600 Index was little changed on Friday, falling 4.6% on the week, its biggest weekly drop since March with miners and energy shares leading the declines. China CSI 300 was the notable performer on the week, up over 1% as investor begin price a reopening of the economy and an ease in tech regulation.

Speaking for the first time since his post FOMC meeting remarks, Fed Chair Powell said, “My colleagues and I are acutely focused on returning inflation to our 2% objective ,”. Then, the Fed released its semi-annual monetary report to Congress where Powell will be facing Q&A from lawmakers later this week and the message could not be clearer, with Powell’s testimony noting “The committee’s commitment to restoring price stability — which is necessary for sustaining a strong labor market — is unconditional.”. Hammering the unconditionality theme, Fed Governor Waller said over the weekend that “The Fed is ‘all in’ on re-establishing price stability,” and that he would support another 75-basis-point rate increase at the central bank’s July meeting should economic data come in as he expects.

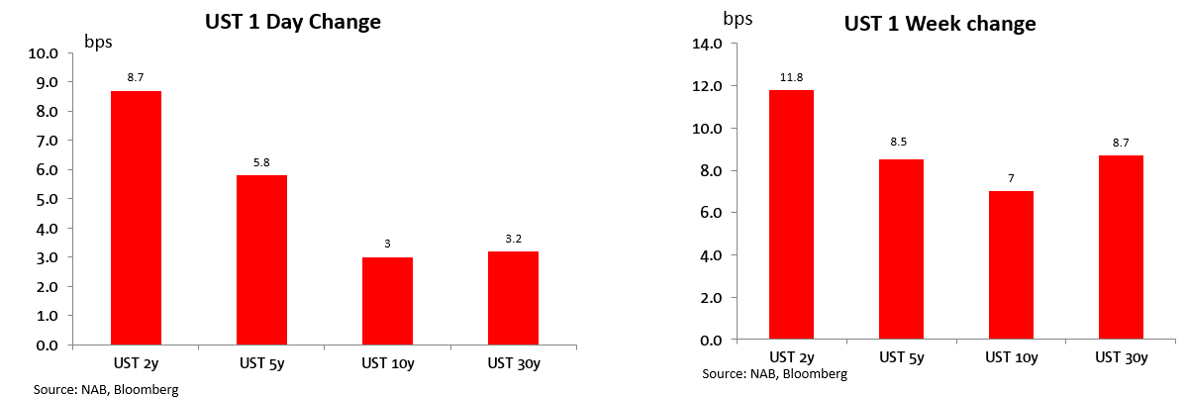

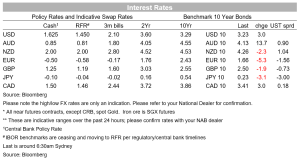

The US treasury curve bear flattened on Friday with the move led by an 8bps rise in the 2y Note to 3.18% while the 10y tenor climbed 3bps to 3.22%, after trading down to an intraday low of 3.20%. That said the theme for the week was for a broad rise in yields with gains of 12 to 8bps across all tenors. Two weeks ago, the 10y UST yield was trading at 3.01%, then last week the benchmark yield traded to an intraday low of 3.49% and ending the week 27bps lower. Fed funds futures are pricing in a 78% probability of a 75 basis points hike in July, and an 22% chance of a 50 basis points increase.

In Europe 10y Bunds yields eased 5bps to 1.66% while Italian 10-year BTPS fell -17bps to 3.58% after ECB President Lagarde pledged borrowing costs for weaker nations won’t be allowed to rise too far or too fast. Money markets pare ECB tightening bets, pricing 174bps of hikes by year-end versus 186bps on Thursday. Meanwhile, in a more hawkish tone, ECB Knot said several half-point increases in interest rates could be needed if inflation worsens – indicating a possible move of that size in September may not be a one-off.

Moving onto FX , the BoJ was the big event on Friday and after many central banks surprising with hawkish actions including the widely unexpected 50bps hike by the SNB, the market was gearing up for a BoJ capitulation . In the end, we got exactly the opposite with the Bank reaffirming its ultra-esay monetary policy and commitment to keep policy supportive until the Bank sees evidence of a rise in wages and core inflation beyond the spike driven by energy prices, JPY was the underperformer on the day with USD/JPY up 2%, testing levels above ¥135, the pair starts the new week ¥134.95. A rebound on the Japanese economy plus some evidence of a broadening in price pressures including an uplift in wages remains a possibility later in the year and with it a possible tilt in the BoJ approach.

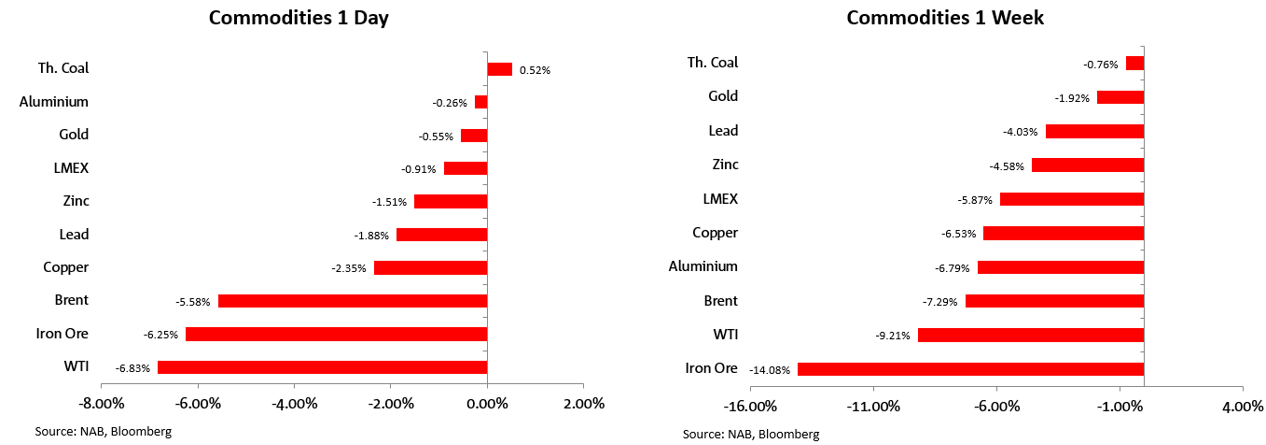

Commodity linked currencies also struggled on Friday and on the week amid growing concerns over the global economic outlook. Recession fears have not only resulted in an increase in market volatility, not a friendly environment for pro-growth/risk pairs such as the AUD, but we have also seen commodities come under pressure too. Oil prices fell 6% on Friday to settle at US$113.12 a barrel, while WTI fell US$8.03 or 6.8% to settle at US$109.56. In addition to a decline demand amid growth concerns, oil prices were also negatively impacted by comments from the Russian deputy energy minister noting he expects Russia oil exports to increase in 2022 despite Western sanctions and a European embargo. Iron ore prices were the underperformers on the week, down 14% amid concerns over China’s recovery path given ongoing covid lockdown risks.

Against this backdrop, NOK was the big underperformer in the past week, down 3.12% while the AUD and CAD were not too far behind down around 1.8%. AUD opens the new week at 0.6921. Meanwhile NZD performed a little bit better, only down 0.68% and now trading just above the 63c mark. Concerns over China’s growth outlook weighing more on the AUD relative to the kiwi with the AUD/NZD cross starting the new week just below 1.10. The recent unwinding of net short speculative positioning in the NZD has also been a supporting factor for the kiwi, in contrast there has been no notable unwinding of positions in for the AUD.

On weekend news, French President Macron is projected to suffer a major blow, with his centrist alliance failing to keep its outright majority in the French parliament. The euro has opened a tad softer following the news, now trading at 1.0476. Meanwhile on Sunday, Germany unveiled new measures to reduce its Russia energy. Germany will restart coal-fired power plants and offer incentives for companies to curb natural gas consumption, marking a new step in the economic war between Europe and Russia.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.