Online retail sales growth slowed in May following a fairly strong April

Insight

Some relief in equities with a strong bounce back from last week’s decline

https://soundcloud.com/user-291029717/brighter-days-ahead?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Equities came back from the holiday Monday in the US to a reprieve. The S&P500 was 2.4% higher, some relief after their worst week since March 2020 last week. Across other assets, price movements were relatively muted in the context of recent price action, but consistent with rebound in risk sentiment. Long-end yields were generally a little higher globally, and the US dollar edged lower across all G10 currencies bar the yen.

It was another day of light news flow. Central Bank speakers continued to be the highlight but overall there was little change in tune out of ECB, Fed or BoE messaging. Recession risk is still front of mind. On that, Biden said that he had spoken to Larry Summers, who yesterday talked up the necessity of higher unemployment to cool inflation and concluded that a recession was ‘not inevitable’ . Domestically, it was a big day for RBA communication yesterday with a speech by Governor Lowe, the June Meeting minutes, and the release of a review into the experience with yield targeting. More detail below, but the short version is 75bp in July all but ruled out, current interest rates below 1% still ‘highly accommodative’ and more hikes needed, and the RBA focussed on charting a ‘credible path’ back to 2-3% inflation.

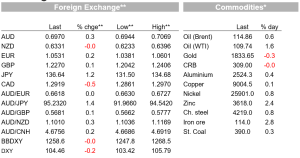

The dollar was -0.2% lower on the DXY. Broad-based weakness across most of the G10 enough to offset renewed weakness in the yen. The Aussie was 0.3% higher at 0.6970, having ranged between 0.6935 and 0.6994 while NOK and CAD led the gains against the dollar. Yen weakness renewed, the dollar gaining 1.2% against the currency to a new 24-year high of 136.7. Of some note was analysis done out with some analysis highlighting the scale of the BoJ’s recent efforts to defend the 10-year yield cap. The BoJ has bought over 25% more JGBs than it has in any month previously so far in June and now owns close to half the JGB market, underscoring the scale of the BoJ’s recent fight to defend the yield target.

The S&P500 was 2.4% higher, with gains broad-based across industries and led by energy and consumer discretionary. The Dow rose 2.1%, and the Nasdaq was 2.5% higher. European share were also higher, the Euro Stoxx 50 up 0.7%, the US playing some catch up for yesterday’s holiday. As for yields, longer-end yields were generally higher globally . The German 10yr was up 2bp to 1.77%, while 10yr gilt yields were 5bp higher. The US curve steepened, with the 2yr yield 2bp higher and the 10yr yield managing a 7bp increase to 3.3%., helping the 2s10s spread back up to 7bp after dipping negative last week.

From the ECB, Governing Council member Olli Rehn said next months rate increase would be 25bp and called a larger-than-25bp move at September ‘very likely,’ while Kazimir sees a 50bp move in September as ‘highly probable.’ Markets are already ahead of that, of course, with 88bp priced by September. From there, Rehn said that gradual increases would follow. On the anti-fragmentation tool in development, Rehn said it is designed to fight ‘unwarranted’ deviations in the euro-area sovereign bond market, and said there has to be plenty of room for judgment. “To my mind it is very clear that there is no automaticity, there is no one single benchmark,”

Fed Richmond President Barkin, a non-voter this year, backed Powell’s guidance that another 50 or 75bp move was on the table in July. Barkin said “we are in a situation where inflation is high, it’s broad based, it’s persistent, and rates are still well below normal.” 75bp was on the table at June due to the May CPI report, Barkin said, and “if it’s possible to do it, why wouldn’t you do it?” Barkin summarised the spirit of the Fed’s task as “ you want to get back to where you want to go as fast as you can without breaking anything.” All-in-all supportive of getting out of accommodative settings fast, but not of blindly marching well beyond neutral if the data flow starts to give. Barkin was on the wires again in the last couple of hours noting the while he understands why some are forecasting a recession, he still sees the case that Fed can moderate demand without dipping into recession.

BoE Chief Economist Pill reiterated the message out of the meeting last week that the Bank is ready to act more aggressively if needed. Pill highlighted the risks of self sustaining momentum in inflation and said it was crucial to ward off second round effects. Signs of breadth in May CPI due today then, will be watched with interest. Pill sees a need for more interest rate rises, and there was a willingness to sacrifice growth to lean against second round effects if necessary. “ We will do what we need to do to get inflation back to target. And, at least in my view, that will require further tightening of monetary policy over the coming months.”

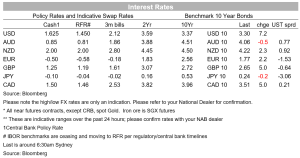

We had a slew of communication from the RBA yesterday. For markets, the key comment came in the Q&A with Governor Lowe effectively ruling out a 75bp rate rise in July, saying that he expected the same discussion between 25bp and 50bp options as in June . With no potential catalyst in the data flow until then markets diligently took the risk of 75bp out of July pricing, but kept some risk of a larger-than-50bp move priced into the August meeting, coming after Q2 CPI on 27 July. Lowe’s observation that market pricing implied the sharpest tightening in the inflation targeting regime, would have large economic impacts, and in his view was not very likely to be matched, was also of some note, though he did concede markets had been a better predictor of late. The AU 3yr yield was 5bp lower at 3.55%.

Overall, there was nothing in the RBA communication to preclude follow up 50bp hikes at the next two meetings, and a clear shyness with regards to shaping expectations for the upcoming cycle. Governor Lowe’s speech stayed close to the talking points in his 7:30 report interview last week. The RBA sees inflation staying high over 2022, but expects it to be coming down by the first half of 2023. The task at hand, then, is to “chart a credible path back to an inflation rate of 2 to 3%.” The June Minutes noted that a cash rate below 1% is still “highly stimulatory, and that further increases would be required.” And that in June the decision to move 50bp won the day over arguments for a ‘steady approach’ of 25bps per meeting through until the end of the year.

It was a relatively quiet night for the data flow. US existing home sales fell 3.4% to 5.41m in April, close to the consensus for a 3.7% fall. That’s the fourth consecutive monthly fall as housing sales track the ongoing fall in mortgage applications alongside the sharp shift higher in mortgage rates. Prices of single-family homes rose 3.1%, but that’s a seasonal phenomenon. Increases were lower that usual for that time of year. Canadian retail sales were strong in April, with preliminary May results also pointing to a solid Q2 outturn.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.