Online retail sales growth slowed in May following a fairly strong April

Insight

US equity markets have begun the new week on the back foot with a clear lack of conviction.

https://soundcloud.com/user-291029717/heading-for-a-choppy-end-to-q2?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

US equity markets have begun the new week on the back foot with a clear lack of conviction. Meanwhile core yields have pushed higher not helped by soft auctions on both side the Atlantic, 10y UST yields now trade at 3.20%. The USD is mixed, losing a bit ground against EU currencies but edging a bit higher against pro-growth/risks sensitive pairs, AUD and NZD are down ~0.3%, relative to levels this time yesterday. Oil prices trade higher amid output concerns and no news on price cap.

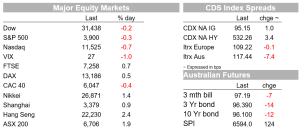

After solid gains last week, overnight US equities traded in and out of positive territory before ending the day with small losses, the S&P 500 closed 0.3% lower while the NASDAQ was 0.72%. There is a clear lack of conviction by investors with light trading volumes favouring the notion of an exhausted market with big declines set to be recorded this quarter, notwithstanding the outsized gains logged last week. Month end rebalancing plays to the view that some buying should be seen over coming days given the need for portfolios to increase their equity exposure after the big loses during the quarter (S&P 500 -14% qtd), then again may be the gains recorded last week were part of this flow. European equities had a more positive start to the week with the Stoxx Europe 600 Index closing 0.5% higher, although this was after trading to an intraday high of 1.4%.

A decent move up in core global bond yields didn’t help the mood overnight. A soft 5y auction, triggered a Bunds sell off with the 5y tenor ending the day 12bps higher while the 10y climbed 10bps to 1.55%. A weak reception to both 2y and 5y auctions in the US didn’t help sentiment either, the 2-year note auction tailed by 0.7bp drawing a yield of 3.084%, the highest since December 2007 meanwhile the US 5-year auction drew 3.271% vs WI yield of 3.236%. The lack of demand can partly be attributed to the big moves lower in yields recorded last week, for instances 10 Bunds fell from a peak of 1.79% to a trough of 1.35% while 10y UST yields traded down from a high of 3.29 to 3.01%, so once seen in that context, 10y UST yields at 3.20% today are just above the middle of recent ranges.

Overnight US data releases were mixed and of second tier nature . The June durable goods orders report was slightly stronger than expected, with core capex orders rising 0.5%m/m, sa. On face value this is good news, but the numbers are reported in nominal terms. Order growth on a %3m/3m, saar, basis has stabilized around 8%, while growth in nominal shipments on the same basis has moderated to 9.4%, but taking some of the gloss, in the past 3 quarters of actual data (21Q3-22Q1) the deflator in equipment spending has averaged 6.3%. Meanwhile the June Dallas Fed survey fell 10 point to -17.7, this after soft prints from the NY and Philly survey, the Richmond survey (more below) is out tonight and is also expected to print lower, together regional surveys are pointing to the risk of a disappointing ISM print on Friday . The market is looking for an ease in the headline reading from 56.1 to 54.5, but the regional surveys are suggesting a print closer to 50 (if not below) is now looking more likely. The other data release was Pending home sales which rose 0.7% against an expected fall of 3.9% after a 4.0% decline in April. Not the most telling of indicators but at the margin a little better for once, less bad.

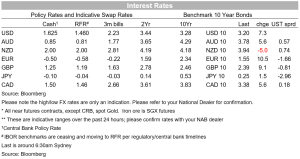

Moving onto FX, it has been a quite start to the new week with the USD a little changed in index terms. The greenback lost a bit of ground against EU pairs with the euro 0.25% stronger and now trading at 1.0583. The Group of Seven nations are still discussing a cap on the price of Russian oil that would work by imposing restrictions on insurance and shipping, but there still remain a great deal of uncertainty on how the cap will work and whether the cap itself will replace the current sanctions.

The AUD and NZD have traded a little bit lower over the past 24 hours with softness in US equity markets probably the main driver. That said, both pairs are trading within recent ranges with the AUD starting the new day at 0.6925 and NZD just above 63c. Month end flows are also likely to be a distraction for FX markets this week.

Oil prices rose overnight (+2%) in a choppy session with WTI climbing to $109.81 while Brent reached $115.15. In addition to the uncertainty in the price cap discussion, prices were supported by news of potential oil production cuts, Libya’s National Oil Corp. signalled a potential dent in supply due to a worsening political crisis. Ecuador could halt oil production even quicker due to anti-government unrest, the energy ministry there said

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.