Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Weaker US consumer confidence dents equities

https://soundcloud.com/user-291029717/less-us-confidence-tough-talking-ecb?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

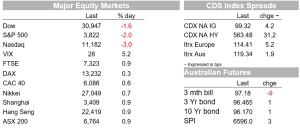

The positive tone that took hold in the Asian afternoon helped by news of China easing quarantine restrictions for inbound travellers turned sharply through the US session, the obvious culprit being a softer-than-expected consumer confidence reading. US equities opened higher, but tracked lower through the day, the S&P500 closing 2.0% lower.

The 2.0% fall in the S&P500 takes losses to 15.7% quarter-to-date and puts it on track for its worst first-half performance since 1970 , down more than 19% this year. Declines were led by consumer discretionary and IT, with energy the only industry in the green, managing a 2.7% gain. Oil extended gains for a third day, Brent up 2.5% to $118, amid a tight supply backdrop and a G7 agreement to look into a price cap on Russian oil. The Nasdaq outpaced declines in other US indexes, falling 3.0%. The Dow was 1.6% lower. Before the US session, Asian and European equities were generally higher.

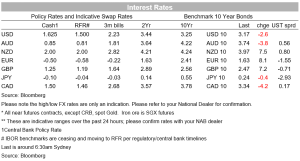

European yields were mostly higher, the German 10yr gaining 8bp to 1.63%. That was helped by hawkish sounding noises from ECB officials. Lagarde said that “inflation pressures are broadening and intensifying,” and said that the ECB would act “in a determined and sustained manner, incorporating our principles of gradualism and optionality.” A shift in emphasis perhaps, from previous comments to raise rates gradually, while also noting that “ clearly conditions in which gradualism would not be appropriate” (that is, de-anchoring inflation expectations). The ECB will start targeting “unwarranted fragmentation” in bond markets using flexibility in reinvesting of PEPP assets from the start of July. Also capturing some interest were comments from Governing Council member Kazaks, who said “front-loading” hikes, including a possible larger move next month (despite strong guidance for a 25bp first move) could be reasonable. In a Reuters interview, Belgium’s Wunsch said “the next 200 basis points (of rate hikes) are a no brainer for me,” and “I think we need to do it relatively fast. Such a move is priced in by next March.”

In contrast, US yields relatively muted, the 10 yr yield down 3bp to 3.17%. Fed speakers did little to shift the needle . The New York Fed’s Williams, in his first comments since the 75bp June hike, said 50bp and 75bp were on the table for July with more increases to come after that, in line with comments from Chair Powell. He also said that a 3.5-4% fed funds rate is ‘perfectly reasonable’ and noted he had one of the lowest forecasts amongst committee members for GDP growth, to slow this year to 1-1½%, “…but that is not a recession.” Mary Daly talked down recession risk, saying “I wouldn’t’ be surprised, and it’s actually in my forecast, that growth will slip below 2%, but it won’t actually pivot down into negative territory.”

In terms of data flow, the key release was the US Conference Board measure of Consumer Confidence, which came in at 98.7 in June from a downwardly revised May number of 103.2 (expectations were for 100). That’s a weak reading to be sure, but stands in contrast to the record low seen in the University of Michigan Consumer Sentiment read. The decline was due to the expectations component, which fell sharply from 73.7 to 66.4 and is at its lowest since March 2013. The Present Situation read held up, declining only marginally to 147.1 from 147.4. The Consumer Confidence measure askes directly about the labour market, which remains strong and has supported the series relative to the UMich measure.

In other data, preliminary US wholesale inventories rose a healthy 2% in May, while the Richmond Fed Manufacturing Index joined it Dallas counterpart yesterday in surprising softer , 10 points weaker at -19 compared to expectations for a small improvement and flagging risk of a softer ISM Manufacturing print on Friday. Shipments and New Orders declined sharply from −14 and −16 in May to −29 and −38 in June. While the employment index rose to 23 from 8. There was some indication of supply chain relief as the indexes for vendor lead time and order backlogs both decreased in June. The US trade deficit narrowed marginally further in May to -$104.3. The April and May numbers so far pointing to a positive contribution to Q2 GDP growth.

Helping the more risk positive mood that permeated prior to the US session was news in our afternoon yesterday that China will cut is quarantine period for international travellers. Inbound arrivals will now need to quarantine for 7 days in a hotel and 3 days home, down from up to 21 days previously. The news comes after Monday marked the first day since recent outbreaks that zero new cases were reported in either Beijing or Shanghai. It’s a positive signal of some give on covid restrictions, though a National Health Commission spokesperson said “The shortening of the quarantine period is an improvement rather than a relaxation of the country’s Covid-prevention strategy. ” With no fundamental shift in the containment strategy, the recent recovery in activity remains fragile, but there is perhaps some movement in the direction of balancing covid containment with economic activity. President Xi last week urged officials to try to meet economic and social target for this year, despite the 5.5% growth target looking out of reach.

In currency markets, the US dollar was stronger. The DXY gained 0.5% to 104.49, appreciating against all of the G10 except CAD and CHF. The AUD was relatively resilient to the rising dollar, down just 0.3%. The AUD got a boost on the headlines of China easing restrictions, rising 0.5% to 0.6964, before moving lower to be around 0.6908 currently.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.