Total spending grew 0.9% in June.

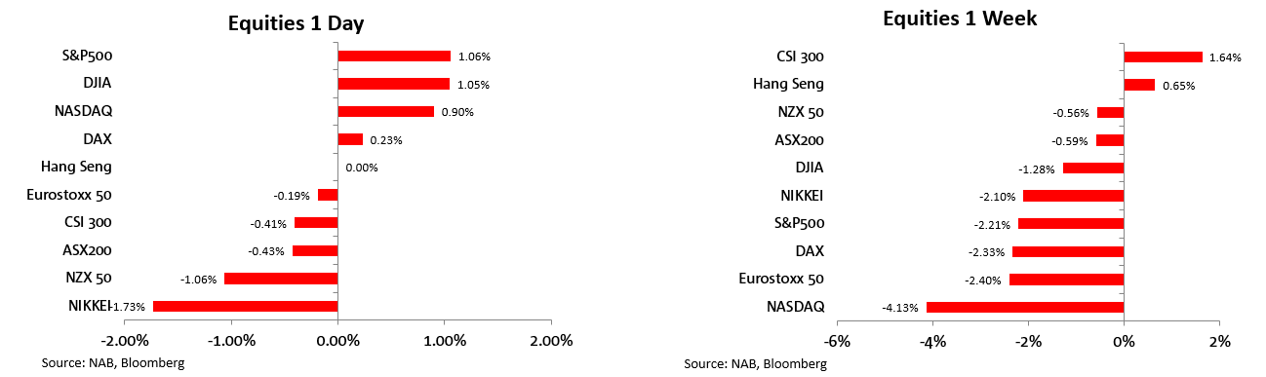

After a dismal first half, US equities start H2-22 with a positive tone

https://soundcloud.com/user-291029717/independence-day-recession-resurgence?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

At least for equities, bad news continues to be good news. Notwithstanding increasing recessionary concerns and after a dismal first half, US equities started the second half of the year on a positive note. The US ISM manufacturing printed softer than expected with the new orders subindex falling into contractionary territory, fuelling US recessionary concerns alongside a less aggressive Fed tightening cycle. Meanwhile, EZ inflation reached a new record high in June, heightening the debate over more aggressive ECB hikes. In a volatile environment, core global yields accelerated their decline while the USD was broadly stronger. Amid global growth concerns, AUD and NZD print new 2-year lows, a theme also evident in industrial commodities with copper down on Friday and on the week too.

The US ISM manufacturing index fell to 53.0 from 56.1, below the consensus, 54.5, and a two-year low. The decline in the headline reading was weighed down by a heavy decline in the new orders subindex, falling 5.9 points to 49.2. The orders sub-index tends to lead the index and suggests further weakness should be expected in July both in terms of the ISM and actual activity (i.e., industrial production). The employment index also underwhelmed, falling further into contraction in June. The softer ISM was yet another piece of evidence that the US economy is slowing, after the weaker than expected consumer (confidence and spending) and investment figures last week. Importantly too, while the data is suggesting a US economic slowdown is coming, we are not yet seeing signs of an ease in inflationary pressures, an important distinction given the Fed will continue with its aggressive tightening approach until it sees evidence of the latter.

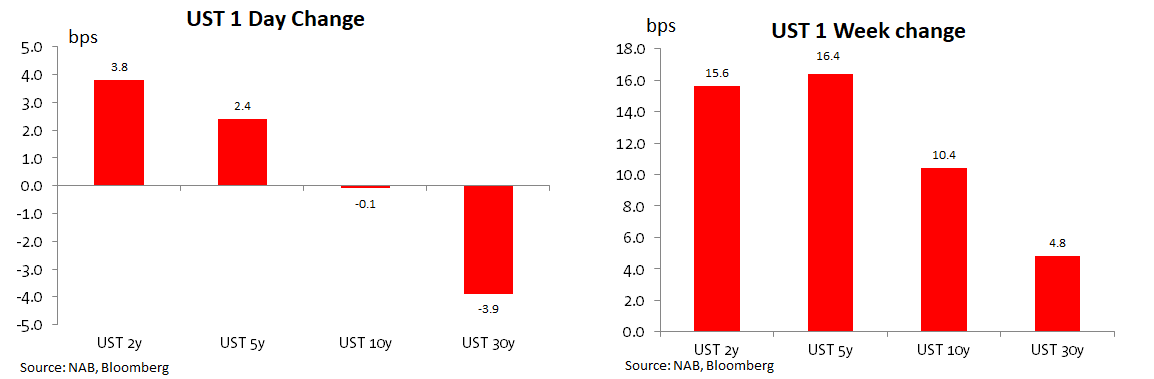

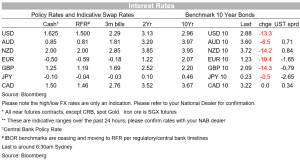

10y UST yields traded in a 3.02% to 2.78% range on Friday, that is a very wide 23bps range for the day, before closing the week at 2.88%. The highs printed early during our time zone and then it was mostly a downtrend pattern briefly interrupted by the stronger than expected Eurozone inflation print which lifted the 10y Note to a high of 3.0% early in the European session. The UST rally resumed following a softer than expected ISM Manufacturing print. 10-year yields dropped to a low of 2.787% in the aftermath before recovering very quicky and ending the day at 2.88%.

Rates’ volatility was not limited to just the 10y UST Note, the 2y UST yield traded in a 2.98 to 2.72% range on Friday (a 26bps range), closing the week at 2.83%. Similarly, the 2y Bund fell 14bps to 0.499% on Friday, two weeks ago they were trading at 1.14%. On the week core global yields traded lower, 10y UST down 25bps while 10y Bunds and Gilts fell 21 and 20bps respectively

Lack of liquidity as the Northern Hemisphere summer kicks in, is one contributing factor for the rates market volatility, but importantly too investors are struggling to reconcile concerns over higher inflation and aggressive central bank policy tightening (pushing yields higher) versus softer economic data and a policy induced economic slowdown (pushing yields lower).

Eurozone inflation printed a record 8.6%yoy in June vs estimate for an 8.5% outcome and 8.1% previously. The core reading ease to 3.7%yoy from 3.8% against expectations for a rise to 3.9%. Food and energy price spikes were the main culprit driving the headline higher while Germany and its temporary measures to ease fuel and transport costs (train tickets) prevented the core measure from reaching 4%. The ECB is widely expected to lift the deposit rate by 25bps in July, but the higher-than-expected inflation print and prospect of higher numbers over coming months (German subsidies expire in August), is now fuelling the debate over ECB rate hike path. The market now prices a 28bps hike in July followed by a 75bps hike in September.

Meanwhile in the US, the market is still pricing an aggressive near-term rate hike path for the Fed, with around a 70% chance of a 75bps hike priced in for the meeting later this month, in-line with Fed officials’ recent messaging. But the market has moved to price in an increasingly aggressive rate cut profile for the Fed into 2023 and 2024, consistent with a growing chance of recession. Around 60bps of Fed cuts are now priced in for 2023.

In contrast to the rise in rates market volatility, equity volatility has been on a steady decline over the past fortnight, after trading to a an intraday high of 34.82 on June 17, the VIX index ended Friday close to the lows for the day at 26.7 . Meanwhile over the same period, rates volatility has been on the rise with the Move Index closing the week at 144.17, a new post pandemic high and well above its 97.13 level printed at the start of June.

May be, after a dismal first half (the worst since the early 1970s), all the bad news are already priced in alternatively the recent decline in equity volatility is a red herring with more pain on the way. The upcoming US earning reporting season, which begins July 15, is going to be a big test with many highlighting the risk of some significant downward revisions to earnings.

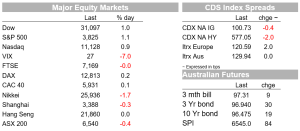

So, notwithstanding the bad economic news, Friday’s US equity price action was about bargain hunters with the S&P 500 clawing it way back into positive territory, after opening the day lower. The Dow rose 1.05% and the S&P 500 gained 1.06% while the Nasdaq added 0.90%. Utilities led the S&P 500 gains with all sectors finishing the day in the green. Looking at the week, however, the S&P 500 fell 2.2%, recording its eleventh decline over the past 13 weeks. The NASDAQ was the big underperformer down 4.13% while the Hang Seng (0.65%) and China’s CSI 300 (+1.64%) were the outperformers over the past 5 days.

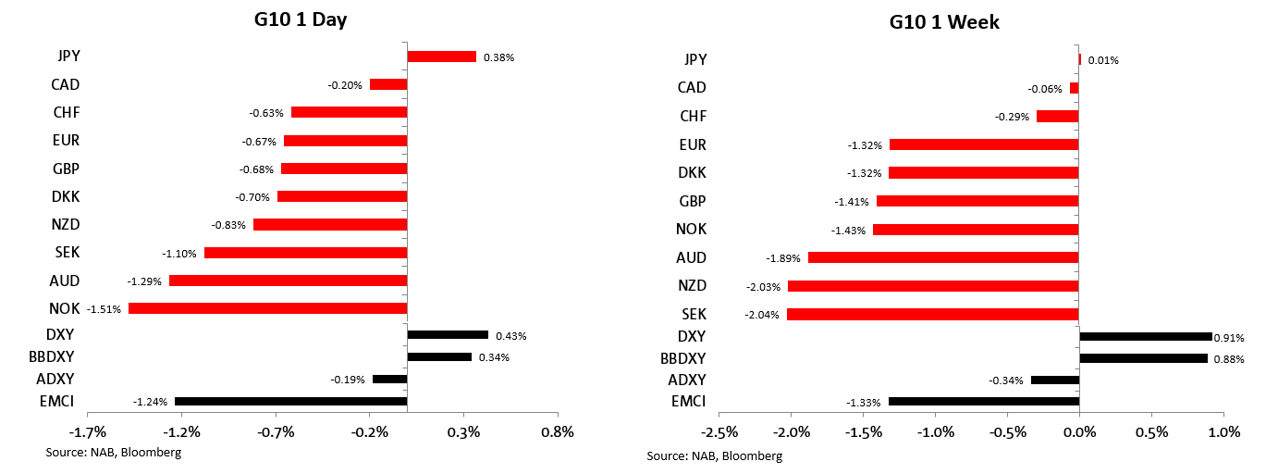

Concerns over an economic global growth slowdown supported the USD on Friday, helping the greenback reverse its losses recorded on Thursday. The BBDXY index gained 0.34% on Friday with the DXY index climbing 0.43%. Friday’s bounce helped the USD extend its gains on the week with both indices up close to 1% over the past five days.

USD gains on Friday were broad based with JPY the notable exception. The move lower in UST yields helped the yen recover some of its safe-haven attributes, after testing levels above ¥137 earlier in the week, USD/JPY traded to an intraday low of ¥134.75 on Friday before closing the week just above ¥135.

Meanwhile against a recessionary concern backdrop, the AUD (0.6764) and NZD (0.6148) printed new 2-year lows on Friday night, before recovering ahed of the NY close. The AUD starts the new week at 0.6813 and NZD is at 0.6194. Both antipodean pairs were amongst the G10 underperformer for the week, down 1.9% and 2.03%, reflecting their sensitivity to the global growth outlook.

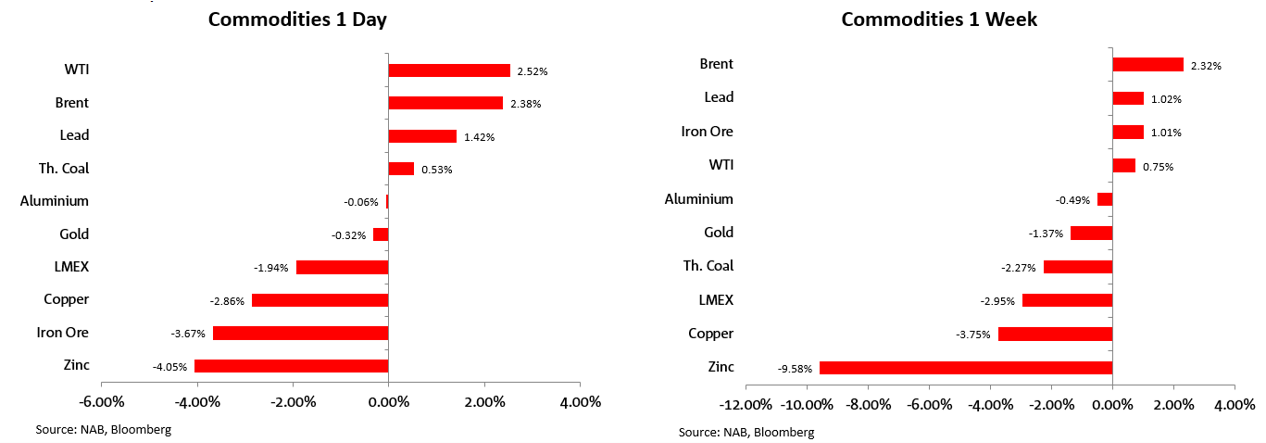

Looking at commodities, copper’s decline on Friday (-2.86%) and on the week (-3.75%) has been one of the big stories. Copper, often seen as a bellwether of global economic activity, is now some 25% off its peak reached in early March. Other industrial metals also fell, Nickel down 3.9% while Zinc fell close to 10% on the week. Oil prices, in contrast, were slightly higher last week. JP Morgan’s research team published a note suggesting oil prices could reach as high as $380 a barrel in a scenario where Russia retaliated by cutting its production by 5 million barrels per day.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.