Total spending grew 0.9% in June.

Risk sentiment improved over the past 24 hours.

https://soundcloud.com/user-291029717/a-glimmer-of-hope-except-for-boris?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

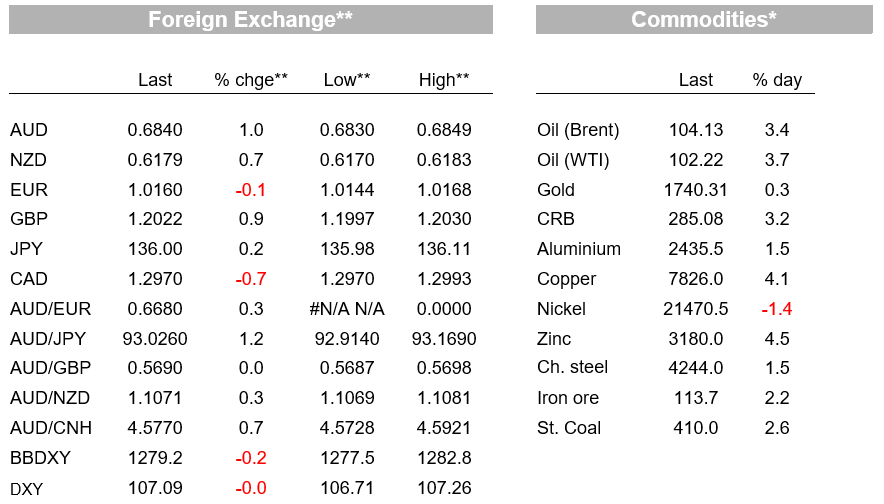

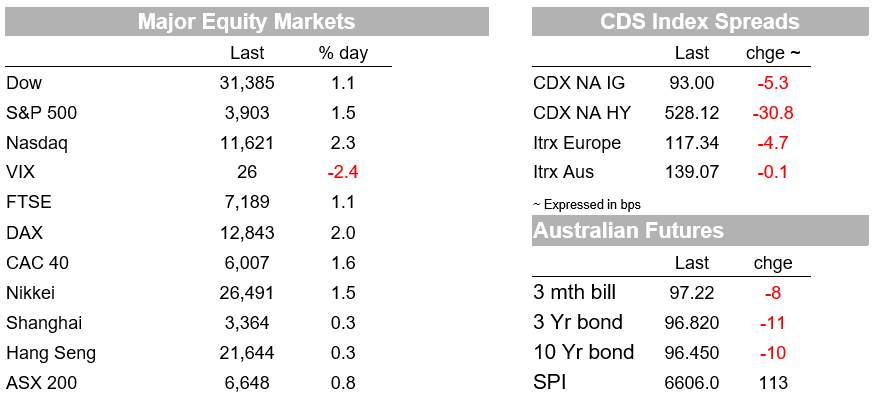

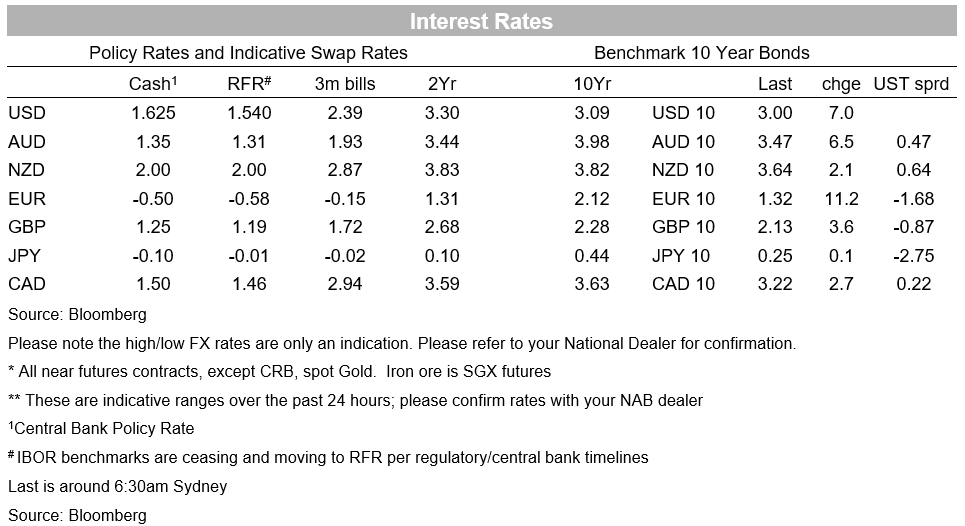

Risk sentiment improved over the past 24 hours. Equities are up with the S&P500 +1.5%, its fourth consecutive day of increase. Sizeable gains were seen in energy (energy sub-index +3.5% as WTI oil rose +4.1% to $102.66) and tech stocks following Samsung’s earnings beat yesterday (IT sub-index +2.1%; NASDAQ +2.3%). Helping turn sentiment positive yesterday was a Bloomberg report that China is considering letting local governments sell an additional $220bn (~1.3% of GDP) in special bonds to fund infrastructure investment to shore up the economy. Also adding post-market was clothing firm Levi Strauss reporting better-than-expected earnings and remaining optimistic on the outlook, contrasting with the recession talk pessimism. More on the earnings season will be revealed next week. Yields have pushed higher in this environment for the second consecutive day with the US 10yr +7.6bps to 3.00%. Nominal yields outpaced real yields (TIP yield +2.7bps to 0.66%) with the implied inflation breakeven +4.4bps to 2.34%. Yield curves have steepened, though 2s10s remains slightly inverted at -2.9bps.

Despite the positivity, Fed speak remains overwhelmingly hawkish. Governor Waller noted “we need to move to a much more restrictive setting“, adding he wanted to do so “as quickly as possible.” As for rates guidance: “I’m definitely in support of doing another 75 basis point hike in July, probably 50 in September, and then after that we can debate whether to go back down to 25s,”. Importantly “If inflation just doesn’t seem to be coming down, we have to do more”. To leave markets in no doubt of the Fed’s resolve he said the Fed is “dead set” on getting prices under control and sees fears of a recession being “overblown” and that there is a “ good shot” of a soft lending. The Fed’s Bullard also made similar comments noting that if we did 75bp in July, we would be at neutral and wants to get to 3.5% this year. Markets are well priced for July at a 94% chance of a 75bp hike, but still see the Fed overtightening and price in 54bps worth of cuts in 2023 after a peak of 3.47% in March 2023.

China stimulus news was the other big news yesterday and one driver behind the positivity. According to Bloomberg, China’s Ministry of Finance is considering allowing local governments to sell 1.5 trillion yuan ($220 billion) of special bonds in the second half of this year. The details of the proposal suggests it is not as rosy as the headline suggests with bond sales being a bring forward from next year’s quota according to sources. While Chinese policymakers are considering boosting stimulus, the headwind from COVID-19 restrictions remain given China is still running a zero-COVID policy. Shanghai reported 54 local Covid infections for Wednesday, including two that were found outside of quarantine meaning the virus could be spreading through communities. Shanghai is undergoing mass testing over a three-day period. Meanwhile the BA.5.2 Omicron subvariant has been detected in Beijing

Political news centred around the UK PM resigning, as was widely expected. A new PM is likely to be chosen by the ruling Conservative party by September/October. In the interim, Johnson plans to remain as PM. As for who is the likely successor, Ben Wallace is the marginal favourite in betting markets, though it is a long process with the parliamentary party whittling down candidates to two, and then the party membership voting on which to choose as leader. GBP took the news positively with GBP +0.9% over the past 24 hours to recover back above 1.20. In contrast, the EUR remains under pressure, falling to a fresh 20-year low below 1.0150 and bringing parity into closer view. The EUR is down almost 2.5% this week alone against a backdrop of continued concerns around an energy crisis in the region. There has been no let-up with gas prices in Europe, with natural gas futures rising.

In FX, the USD has been little changed on the DXY and commodity currencies have rebounded overnight amidst the recovery in risk sentiment and commodity prices – copper was +4.1% along with oil. Potential China stimulus was one driver behind commodities. In FX The AUD has led the charge, up around 1.0% over the past 24 hours to back above the 0.68 mark. The AUD may also have benefited from news that the Australian and Chinese foreign ministers plan to meet on the sidelines of the upcoming G20 meeting, offering a chance to improve relations which have been strained over recent years, and also came in the wake of a stellar trade balance (more on that below) The CAD and NZD were also higher by around 0.7%.

Economic data was close enough to consensus and not market moving. US Initial Jobless claims were 235k against 230k expected and remain at extremely low levels. The US trade deficit was $85.5bn against $84.7bn expected. The Atlanta Fed GDP Now still points to a sizeable negative in Q2 at -1.9% annualised (slightly revised from -2.1%). Payrolls of course the big statistic later today where consensus is for 265k jobs and for the unemployment to be steady at 3.6%. High frequency data suggests upside risks to headline payrolls, though most focus is likely to be on average hourly earnings. Across the pond in Germany Industrial Production missed at 0.2% m/m against 0.4% expected.

Finally in Australia, a record trade surplus was recorded in May of $16bn, smashing even our top of the range forecast for $11.5bn. The result was driven by a surge in coal (+20% m/m) and LNG (+12% m/m) export volumes. Large increases were expected in these categories as high prices continued to flow through to assessed export values, with much of the surprise coming on the back of a sharp upward revision to the April balance to $13.2bn from $10.5bn (that revision also largely through coal export values). Exports overall were 9.5% higher, outpacing a 5.8% rise in imports. Underscoring the exceptional strength in export values, the record trade surplus came despite a new record high for import values in the month, partly driven by the oil price.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.