Consumers lead the way

Insight

The ECB hiked rates by a more-than-expected 50bps, taking the deposit rate back to 0% and ending its negative interest rate policy that has been in place since 2014

https://soundcloud.com/user-291029717/ecb-makes-it-to-zero?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

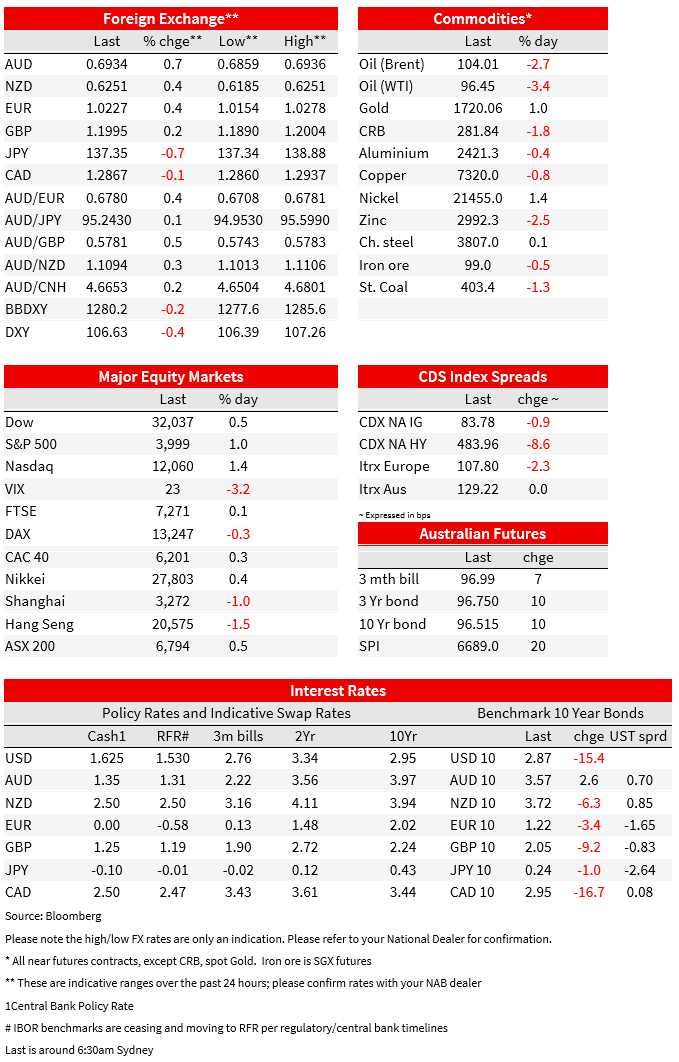

A volatile night with the ECB hiking rates by a more-than-expected 50bps (only 50% priced into the meeting), but moves being tempered by light details on the new anti-fragmentation tool which came in the wake of the Italian PM resigning and fresh elections being called for 25 September. Later in the session second-tier US data printed weaker than expected with Jobless Claims at 251k (vs. 240k expected), while the Philly Fed Manufacturing Index plunged to -12.3 (vs. -0.3 expected). That turn in the US data has seen some hawkishness come out of US Fed pricing with a peak in the Fed Funds rate now at 3.46% in December 2022, from 3.55% in March 2023 yesterday, and 56bps of cuts are still priced for 2023. Those moves were reflected in US yields with the 10yr -13.2bps to 2.90% (nominals moved more than real yields with the implied inflation breakeven -7bps to -2.31%). Meanwhile equities continue to rebound driven by tech, with a 9.8% rise in Tesla helping to propel the S&P500 +1.0%. Global growth fears remain with oil prices -3%.

First to the ECB. The ECB hiked rates by a more-than-expected 50bps (only 50% chance of a 50bp hike was priced into the meeting), taking the deposit rate back to 0% and ending its negative interest rate policy that has been in place since 2014. Importantly forward guidance was dropped with the ECB going forward taking a “meeting-by-meeting approach”. The market has brought forward rate hike pricing for the ECB, with some chance of a 75bps at the next meeting in September and around a 70% chance of another 50bps hike priced for October but little change in the expected peak in the cycle. The ECB also unveiled its anti-fragmentation tool, called the ‘Transmission Protection Instrument’, which is a potential tool that provides “unlimited ” bond buying to prevent “unwarranted” moves in peripheral bond markets. The details, conditionality and what would justify activation was vague and did little to inspire confidence in light of the Italian political situation.

The Italian-German 10yr yield spread widened by 19bps to 230bp, reflecting greater political risk with the announcement of the anti-fragmentation tool having no impact on spreads . Note the Italian PM resigned just prior to the ECB meeting with fresh elections slated for 25 September. European yields initially spiked higher on the ECB’s 50bp hike, but have now mostly reversed. German 2yr yield initially +15bps, now +5bps to 0.68%. German 10yr yield initially +9bps, now -6bps to 1.22%. The EUR told a similar story, up 0.8% initially and then partly reversing to be up 0.2% to 1.0212. In more positive developments gas flows have resumed through the Nord Stream 1 pipeline from Russia to Germany. Indications are the gas flow will restart at 40% of capacity, around what it was before the maintenance shutdown, which is more than the market was expecting. Russian President Putin however warned flows could yet fall to around 20% as soon as next week. After initially falling as much as 8%, European natural gas futures are back to unchanged on the day.

US data disappointed and was market moving despite being mostly second-tier. Jobless claims rose to 251k against 240k expected and 244k previously, some evidence perhaps of a turn in the labour market. Some analysts point out that July data is volatile due to seasonal adjustment issues, but the trend higher in jobless claims is consistent with growing anecdotes of hiring freezes and layoffs at several multinational companies, particularly tech firms such as Google, Apple and Microsoft. Industrials are also planning to cut workers with Ford noting it was planning to cut 8,000 jobs. A loosening labour market is being sought after by the Fed to put downward pressure on inflation, but with inflation remaining high we shouldn’t expect any pivot from the Fed. Separately, the Philadelphia Fed business survey was much weaker than expected with the headline at -12.3 against -0.3 expected and -3.3 previously. The real alarm point was around future activity with the index falling 12 points to -18.6, its lowest reading since December 1979. Such a weak reading would suggest business confidence has fallen to the same recessionary levels as consumer confidence (see: Philly Fed: July 2022 Manufacturing Business Outlook Survey).

In FX currently moves have been modest outside of the EUR which was volatile after the ECB; up 0.8% and then falling back to be up 0.2% to 1.0212. The broad USD BBDXY is -0.2%. The JPY is the strongest currency on the day, USD/JPY down around 0.7% to 137.35 given the fall in global yields means a narrower US-Japan spread. That has seen the narrower USD DXY -0.4%. Most currency pairs are higher against the USD with the AUD +0.7% and NZD +0.4%. Of the other majors, GBP was +0.2%.

In equities, the bear market rally continued overnight with the S&P500 +1.0%, helped along by a 9.8% rise in Tesla. So far in this bear market rally the S&P500 is up 9.1%, though is still -16.6% away from its peak. The profit reporting season for the tech firms at least has been better than feared, though for the non-tech and non-financial sectors guidance has been weak on the outlook and consistent with a slowing economy. Overnight US telco AT&T said there had been an increase in overdue payments of phone bills. The company lowered its free cash flow projection for this year from $14b to $12b, around half of the fall due to the increase in overdue payments, seeing its share price slump by 7.6%. Meanwhile airline stocks fell with American Airlines -7.4% and United Airlines -10%, both reported a cutting in growth plans. European equities also rose despite the large ECB rate hike.

The BoJ also meet yesterday, but with little market impact. The Bank indicated it was sticking with ts ultra-easy monetary policy stance, including its 0.25% cap on the 10-year bond rate. The BoJ upgraded its inflation forecasts, with CPI ex fresh food forecast to be 2.3% this year (largely due to higher oil prices) before falling back to 1.4% next year. Inflation risks are now seen to the upside, but given underlying inflation remains low, Kuroda signalled the BoJ was in no rush to abandon its accommodative stance, saying it had “no intention at all” of raising rates and “zero intention ” of lifting the 0.25% cap on the 10-year bond rate. Kuroda also pushed back against suggestions that a small increase in the cash rate could support the yen, which recently hit a 24-year low, claiming it would require “significant hikes” to reverse the currency’s trend which, in turn, would hit the economy hard.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Consumers lead the way

Insight

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.