Confidence and Conditions Lift

Insight

Kremlin confirms 20% cut of gas to Europe from Wednesday. Gas up 9%

https://soundcloud.com/user-291029717/then-there-was-one-turbine?utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

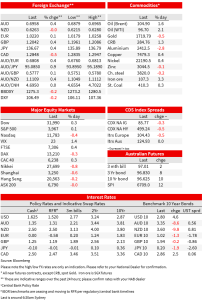

Apparent nervousness over what this week’s big tech.sector earrings will show (Alphabet, Meta, Amazon, Apple) is keeping the NASDAQ subdued, but it has just closed well off its lows (-0.43%) albeit weaker than other indices (S&P500 +0.13%). Meanwhile US Treasury yields have pulled up from their 2.75% Friday lows at 10-years (2s also) in front of Wednesday’s FOMC outcome, in turn lifting USD/JPY (+0.4%). Gains for all other G10 currencies – including a small rise for the EUR despite a weak German IFO report and Russia confirming gas supplied to Germany will be cut to 20% from tomorrow – sees the DXY USD index off about 0.25% into the New York close. A light calendar today – the fireworks begin early tomorrow morning with Alphabet’s results then Australia CPI followed later in the night by the Fed.

News flow such as there is has been concentrated in Europe, which date-wise featured a bigger than expected fall in the German IFO survey, following on from the slump in German PMI readings to below 50 last Friday. The headline Business Climate index fell to 88.6 (lowest since June 2020), IFO noting broad-based falls in confidence across sectors of the economy, with higher energy prices and the threat of a gas shortages weighing on the economy. The fall was led by the Expectations component (80.3 from 85.5) with the Current Assessment down by a lesser 1.7points to 97.7, suggesting Germany’s real economic pain still lies ahead, notwithstanding the literal reading of Friday’s PMIs was that both manufacturing and service sectors contracted in recent weeks.

On the matter of gas supplies, a few noses might have grown an inch or two when the Kremlin announced last night that Russia was not interested in cutting off gas to Europe and that it intended to ship as much gas as technically possible via NordStream1, only to promptly confirm that from Wednesday, supplies into Germany would be cut from 40% to 20% , citing the need to take another gas turbine off-line. The Kremlin also said that the Odesa missile strike shouldn’t affect grain shipments. Right. A German government spokesman said there was no technical reason for a reduction in deliveries. The news of the imminent reduction in gas flow saw prices on the Netherlands exchange up about 9%, still off their earlier-July peaks but up over 15% since late last week.

US economic news has been limited to the July Dallas Fed manufacturing inde x, which at -22.7 from -17.7 (-18.5 expected) is the lowest since May 2020. Along with other regional PMIs published last week and of course the S&P Global PMIs, this adds more to the softening growth story if not true “recession”. Production & shipments were up, new orders down and delivery times shortening. On the inflation front, prices paid and received both reflect lower rates of growth (both though still elevated), wages growth down (also still high, as was employment), all alluding to somewhat lower inflation coming down the pipe.

Central Bank speak was confined to Europe with Fed official of course in their pre-FOMC cone of silence. ECB Governing Council member Kazaks from Latvia suggests the need for another 50bps hike at the next meeting in September, while Italy’s GC member Visco was more open-minded, saying there “was no way to say now” whether a 25bps or 50bps hike in September should be needed, it would depend on the data. Market have already decided 50bps is highly likely, currently pricing 47bps of tightening out of the 8 September meeting.

In markets, US equities have closed well off their low, a loss off about 1% for the NASDAQ coming into the last ‘hour of power’ reducing to just -0.43% and for the S&P500 from about -0.5% to +0.13%.A mixed picture across sectors, energy faring best by a long chalk (3.7%) thanks to higher oil and gas prices (WTI crude +$1.82 to $96.50) and consumer discretionaries worse at -0.85%. The latter sector is exactly where you would expect ‘demand destruction’ from higher interest rates/debt servicing costs and the hits to real income from higher inafltion, to be showing up. Earlier European stocks closed mostly higher, e.g., Eurostoxx 50 +0.2%.

In bonds, US Treasury yields are ending the New York day with both 10s and 2s up 5bps, so 10s at 2.80% after Friday’s (2.75%) lowest close since 31 May 2022. In Europe, of most note was a 17bps fall in Greek 10-yar yields, suggestive of confidence in the ECB’s new-fangled TPI anti-fragmentation tool being put to use here at some point if deemed necessary, not just in Italy.

Finally in FX, AUD ended in New York 0.4% up on the day but the high of 0.6965 was still a shade below last Friday’s high print of 0.6977. CAD and NOK have both fated better than AUD and indeed top the G0 scoreboard thanks to higher oil prices, while USD/JPY ended 0.4% higher thanks to the aforementioned rise in US Treasury yields.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.