More price increases are likely for food and grocery. If they continue to rise in Q3 and Q4, it is hard to see US core inflation numbers moderate sufficiently for the Fed to pivot.

US equities fall -1.2%, partly driven by Walmart’s warning on the consumer

Alphabet reported post-close with mixed earnings, stock up 3% post-market

EU agrees to voluntarily cut gas consumption by 15%; gas prices surge again

US yields little moved ahead of the FOMC, German 10yr yield -9.3bps to 0.93%

Coming up: AU Q2 CPI; CH Industrial Profits; FOMC 75bp hike; US Durable Goods

“Woke up to reality; And found the future not so bright; I dreamt the impossible; That maybe things could work out right; I thought it was you”, Johnny Hates Jazz 1987

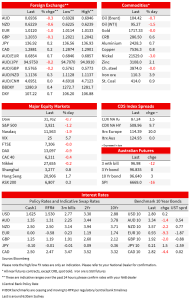

A night of negative news flow that has seen US equities down and USD strength ahead of the FOMC tonight (DXY +0.7%; EUR -1.0%). The big news was Walmart’s profit warning late Monday with Walmart reporting consumers were pulling back on general spending because of rising food inflation, and casting some doubt on the resilience of the consumer. The S&P500 fell -1.2, led by retailers which were down -4.4%. Post close Alphabet (google) reported, missing on earnings and revenue, but less than feared in the wake of Snap with Alphabet up 2% in post-market trade. The IMF as foreshadowed ahead of the G20 downgraded global growth forecasts for 2022 and 2023. In Europe gas prices have surged in the wake of the EU agreeing to voluntarily agreeing to cut gas consumption by 15%. While European bonds have rallied, US yields are little changed on net ahead of the FOMC. Markets have sharply repriced the Fed given growing recession risk with a peak Fed Funds rate now 3.39% in February 2023 against the June FOMC Dot plot of 3.8%, and 52bps of cuts are priced for 2023. The risk going into the FOMC is the Fed pushes back on market pricing given elevated inflation and a still tight labour market.

First to the Q2 earnings season which contained a number of snippets for the outlook. The first was Walmart’s profit warning, noting higher food prices is causing consumers to pull back on discretionary spending. Walmart is seen as a bellwether for retailers and consumers given it makes up 21% of grocery spending in the US. Walmart’s stock plunged -7.6% with other retailers also feeling the effect with the retailers sub-index down -4.4%. The key takeaway here is that with food/grocery making up a bigger share of household budgets due to inflation, discretionary spending is likely to be impacted. Shopify also gave a warning, noting that consumers are pulling back on online orders, perhaps indicative of consumers reverting to pre-pandemic trends (“ what we see now is the mix reverting to roughly where pre-Covid data would have suggested it should be at this point. Still growing steadily, but it wasn’t a meaningful 5-year leap ahead”). Shopify said it was going to cut 10% of its global workforce, or 1,000 people with its stock down -14%.

The other snippet from profit reporting worth highlighting is that more price increases are likely for food and grocery. The WSJ notes that executives told retailers last week of another round of price hikes in the mid-single digits, with Coca-Cola noting overnight its average prices increased 12%, Unilever said its prices rose 11.2% across its brands and Kimberley Clark said it increased prices by 9% (see: WSJ Don’t Expect Big Consumer Brands to Lower Prices Soon ). If food and grocery prices continue to lift in Q3 and Q4, it is hard to see US core inflation numbers moderate sufficiently for the Fed to pivot. The risk from the profit reporting season is that inflation proves to be a little more sticky over the next few quarters, meaning the risk from the Fed is that they continue to be aggressive, even with signs of slowing in activity. On slowing activity, Whirlpool and Weber noted weaker demand for its products, but this may also reflect a pivot away from goods spending associated with the pandemic.

US data was second-tier. The Conference Board measure of US consumer confidence fell by more than expected to a 17-month low of 95.7 versus 97.0 expected. It is worth noting the conference board measure has been more resilient than the University of Michigan Survey. The survey noted “The decrease was driven primarily by a decline in the Present Situation Index—a sign growth has slowed at the start of Q3. The Expectations Index held relatively steady, but remained well below a reading of 80, suggesting recession risks persist ”. The regional Richmond Fed Manufacturing Index was better than expected at 0 against -14 expected. Meanwhile new home sales plunged 8.1% to their lowest level in over two years, providing further evidence that the housing market was rapidly slowing. Supply of unsold new houses is now 9.3 months of sales, a 12-year high, suggesting an over-supplied market and plenty more downside potential in activity.

Across the pond it is all about the gas situation with the EU agreeing voluntarily cut their gas usage by 15% from 1 August through next winter , in anticipation of a complete halt of Russian gas supply. Gasprom is about to cut supply via Nordstream to just 20% of capacity, increasing the chance of gas shortages later in the year. Reduced gas consumption now might help Europe to refill storage to 80%, ahead of winter, but that might still not be enough to get through winter without power rationing. The fear also is if Europe is showing signs of rebuilding gas storages, Russia may further reduce gas flows in order to prevent such re-building so that it continues to have leverage. Regardless of that possibility, higher gas prices are likely to be sustained, which is likely to crimp the European economy, making a recession more likely. Note European natural gas prices rose another 15%, on top of yesterday’s 10% increase, to €202/MWh, their highest level since the early-March spike

Also out overnight was the IMF downgrading global growth forecasts as largely flagged at the G20. The IMF cut it global growth forecasts by 0.4pts to 3.2% for 2022 and by 0.7pts to 2.9% for 2023. Interestingly global inflation was revised higher and is projected to remain elevated for longer. The IMF noted an “increasingly gloomy and uncertain outlook”, with stalling growth across the US, euro area and China. Risks to the outlook were “overwhelmingly” tilted to the downside and it cited a plausible scenario that would send the global economy into recession.

As for market moves, lower European bond rates initially dragged down US Treasury yields, with Germany’s 10-year rate down 9bps to 0.92%, but then US yields reversed ahead of the FOMC to be little changed at 2.80%. In FX it has been a story of USD strength, while there has been a risk-off vibe with CHF and JPY outperforming. Euro weakness continues to be one driver of USD strength with EUR -1.0% to 1.0120. The risks for the Euro appear one sided to the downside given the energy crisis and fragility risks given ECB rate hikes. One hedge fund, EDL Capital, is betting that EUR/USD will plunge to 0.80, with Europe on the brink of disaster. GBP shows a much smaller loss. The NZD (-0.6%), AUD (-0.3%) and CAD (USD/CAD +0.2%) are all weaker, the NZD again being the worst of the commodity currencies.

Coming up today:

AU: CPI-Q2: Consensus is for Headline at 1.9% q/q and 6.3% y/y. The RBA’s preferred core trimmed mean measure is expected to be 1.5% q/q and 4.7% y/y, which would be the highest quarterly core print since the 1990s. A print higher than 1.5% for the core trimmed mean would likely spur speculation of a 75bp hike in August, as well as debate on whether the RBA needs to go well into restrictive territory.

CH: Industrial Profits: no consensus is available

US: FOMC Decision: We expect a 75bp hike which is also the consensus. The key focus for markets is whether Chair Powell pushes back against market pricing which has the peak of the Fed Funds rate lower than the June dot plot (3.382% vs. 3.8% in the dot plot) and is also pricing in 51bps of cuts in 2023. Given how elevated inflation is, it is possible he pushes back on market pricing. If the Fed continues to be hawkish, there will be more talk around recession risk. According to CNBC’s Fed survey, 63% believe the Fed’s effort to bring down inflation to its 2% target would create a recession. Of those who predict a recession in the next 12 months, most believe it will begin in December and most think it will be mild. Meanwhile one of Chair Powell’s favoured recession indicators, the 18m forward 3m less the current 3m tipped into negative territory overnight.

US: Durable Goods/Inventories/Trade Balance: The last of the pre-GDP partials ahead of Thursday’s Q2 GDP print. The Atlanta Fed GDP Now has a Q2 print of -1.6% annualised and the number will be updated post these numbers ahead of the GDP print; consensus for GDP sits at 0.4% annualised. The consensus for core durables is 0.2% m/m and the advanced goods trade balance is expected to be little changed at -$103bn.

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.