We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Neither the Fed nor President Biden could have scripted Friday’s US payrolls report any better had they tried

Friday’s data highlights:

Fed chair Powell, or President Biden for that matter, probably couldn’t have scripted a better August employment report if they’d tried. The Goldilocks metaphor is much used and abused in economic and financial circles, but in relation to the various ‘soft landing’ signals emanating from the report, on this occasion it does seem entirely appropriate. The upshot of Friday’s report is that the market-implied chances of a Fed rate hike of 20 September have reduced to about 7% from 12% beforehand (only a major upside CPI surprise next week would seem to stand in the way of no-change). Market wise, perhaps the biggest surprise Friday was that compared to pre-payrolls levels, US 10-year Treasury yields ended some 7bps higher, and the DXY US dollar index 0.6% stronger – though when we think about the shape the US economy looks to be in at the moment compared to just about every other part of the words, perhaps we shouldn’t really be that surprised.

To the detail, while the 187k rise in non-farm payrolls was both a mild upside surprises and depressed by the loss of 37k trucking jobs last month from Yellow’s bankruptcy – and a further 17k displaced entertainment industry workers from the ongoing writers’ strike – this was more than offset by a net 110k worth of downward revisions to June and July payrolls.

As for the rise in the unemployment rate, up to 3.8% from 3.5% – its highest since February 2022 from where it has fallen to as low of 3.4% – this reflected a surge in the number of people entering the labour force last month, 736k according to the household survey – far outstripping the reported 222k gain in household employment. The participation rate accordingly rose from 62.6% 62.8% – it was last higher than this (63.3%) in February 2020, just as the pandemic struck.

Finally on the employment report, and doubtless to the delight of the Fed, the 0.2% rise in Average Hourly Earnings (AHE) against 0.3% expected was the first time in just over 12 months the monthly rise has not been either 0.3% or 0.4%. This might just be noise but is certainly consistent with the reported fall in the Quit Rate within recent JOLTS reports. That the annual change only fell to 4.3% from 4.4%, as expected, was largely because May was revised up to now show a 0.4% gain from 0.3% originally reported.

The other notable US release Friday was the ISM Manufacturing report, showing a bigger than expected improvement, to 47.6 from 46.4 versus 47.0 expected. Still quite deep in contraction territory, but at a reduced rate of decline. The Price Paid component rose by much more than expected, to 48.4 from 42.6 (consensus 44.0 expected) but largely because of the jump in commodity prices last month. The underlying trend in manufactured goods prices still looks to be down. Anyone minded looking at the ISM report for the about-turn in US Treasury yields after the knee-jerk drop following the employment report should note that the reversal was well underway before the ISM report was published.

Elsewhere Friday, Canada’s much softer than expected Q2 GDP outcome showing an (annualised) contraction of 0.2% against a 1.2% expected gain, saw the chances of another Bank of Canada rate hike on Wednesday, from the current 5.0%, reduce to less than 1%.

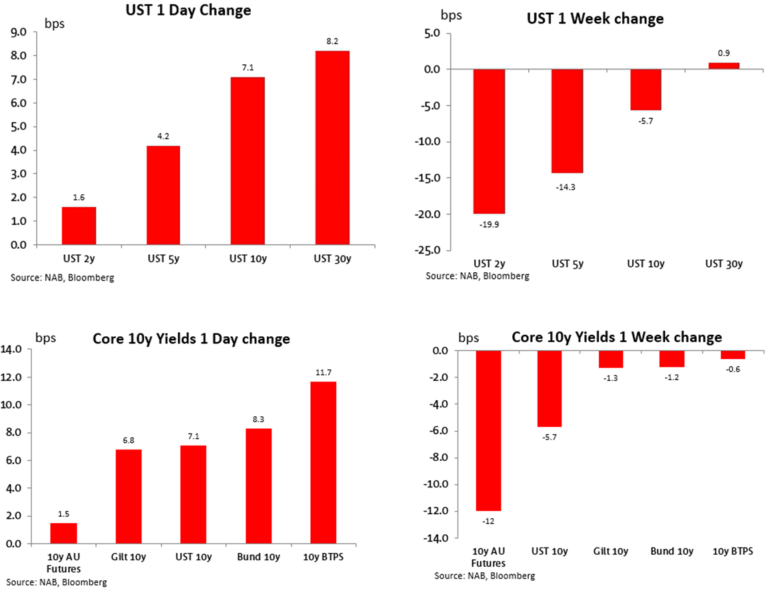

Bonds Friday and Weekly

o markets , and while longer dated Treasury yields quickly reversed – and then some – the knee-jerk falls that followed the headline jump in the US unemployment rate and weaker than expected AHE rise, 10-year Treasuries still ended the week some 6bps lower. Perhaps, therefore, the trading market had gotten itself a bit too stretched on the long side in the days leading up to, and into, payrolls, hence the lack of follow-though gains and then position squaring in front of what is a long holiday weekend, played a part. Anticipation of heavy corporate bond supply, to be compressed into a four-day week, might also have been a factor.

The 7bps net rise in UST 10s Friday was roughly matched by equivalent European benchmarks, which look to have been driven more by Treasuries than local events (the latter limited to small downward revisions to EZ manufacturing PMI and an upward one for the UK). As for Aussie bond futures, 10s were just 1.5bps higher Friday and on the week significantly outperformed both US and European markets, with a 12bps fall – thanks in part to the downside monthly CPI surprise earlier in the week.

Equities Friday & Weekly

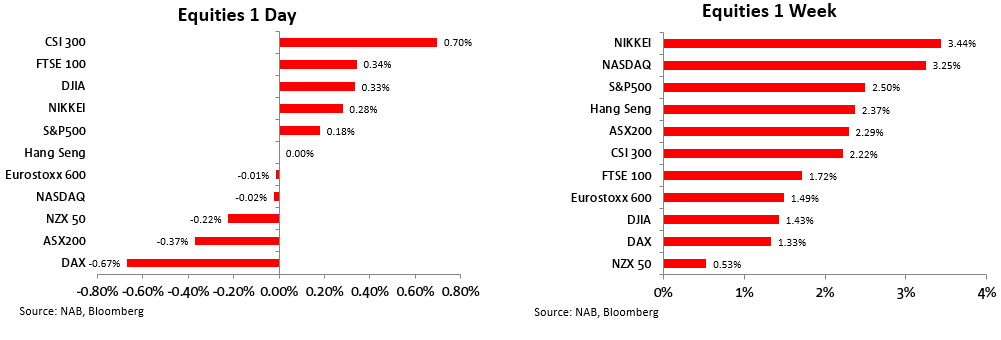

A very mixed day for equities Friday , the S&P500 and NASDAQ ending little changed, straddled by a 0.7% gain for China’s CSI 300 and a 0.7% loss for the German Dax. The former followed the news of cuts to mortgage rates for existing not just new borrowers and a reduction in first home buyer deposit requirements to 20%. All major bourses were up on the week though, led by gains of over 3% for both the Nikkei (3.4%) and NASDAQ (3.3%). The ASX 200 finished mid-pack, but still with a healthy 2.3% weekly gain.

FX Friday & Weekly

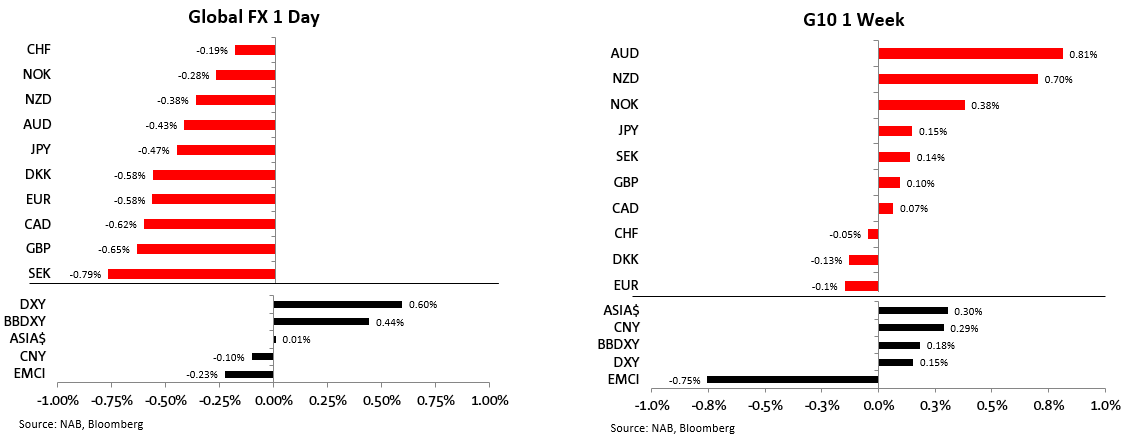

To FX, a knee-jerk fall for the USD on the US employment report headlines went the same way as the Treasury market, the DXY ending Friday with a 0.6% gain. G10 currency losses ranged from -0.2% for the CHF to -0.8% for the SEK, with AUD and NZD both mid-pack with falls of 0.4% – a little less than for the GBP and EUR (-0.6%). AUD/USD had earlier made another, albeit very brief, excursion above 0.6500, as it also had on Tuesday and Wednesday, seemingly confirming its current dubious status as a currency best sold on rallies than bought on dips.

Over the week, the DXY gain was limited to 0.15%. AUD (0.8%) and NZD (0.7%) were the best two performing majors, and where we’d place some of the credit on the pull-back in USD/CNY from above 7.29 at the start of the week to nearer 7.26 at the end.

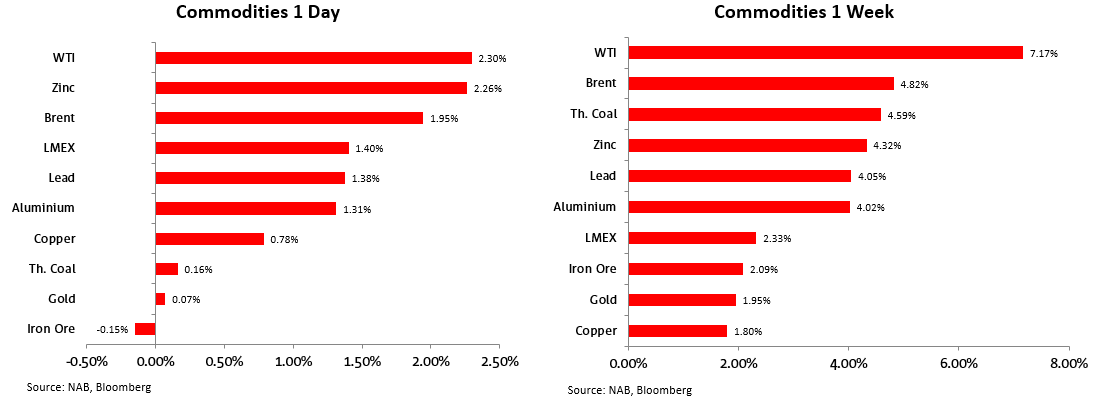

Commodities Friday & Weekly

Coming Up

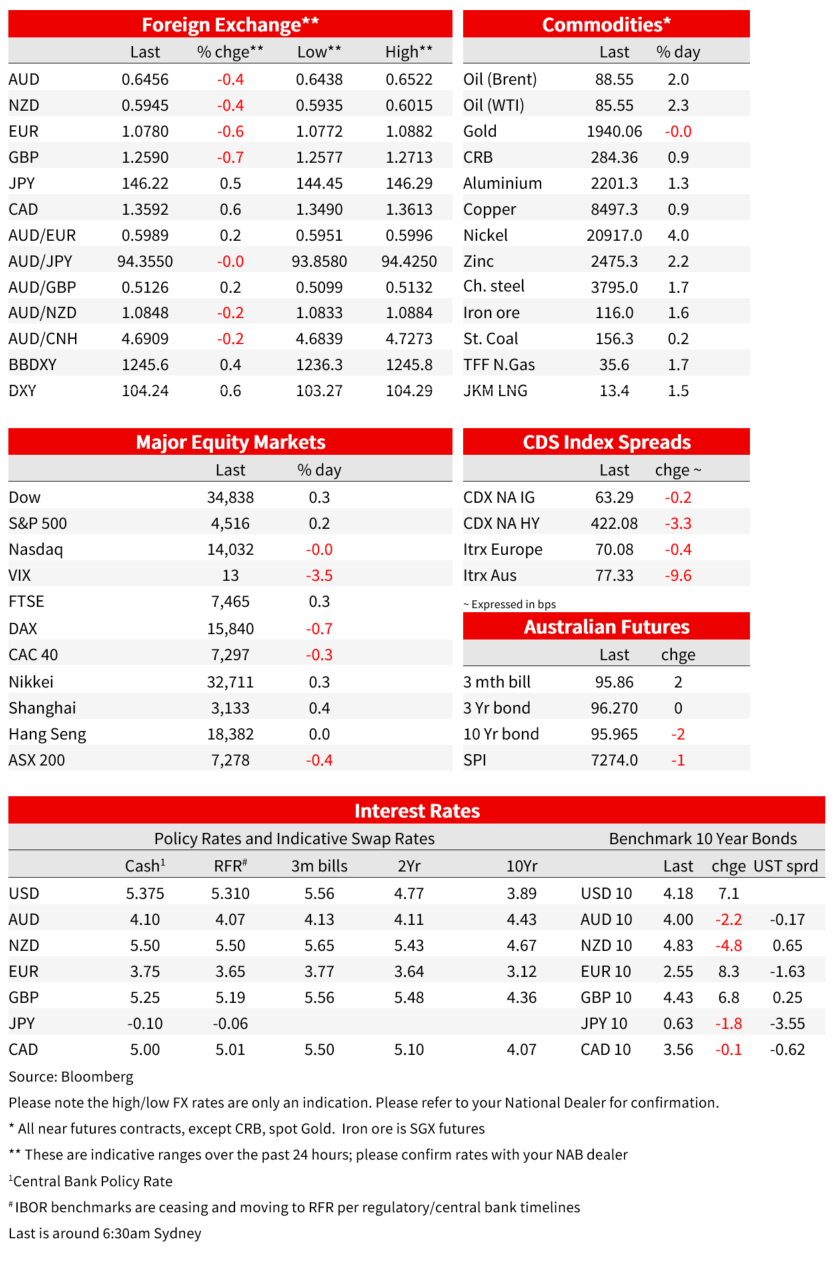

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.