Long-term signal vs. Short-term noise

Insight

Risk assets have enjoyed a positive start to the new week with European and US equities extending Friday’s rebound. After a positive lead from Asia, European and US equities closed the Monday session with gains across the board, extending Friday’s rebound.

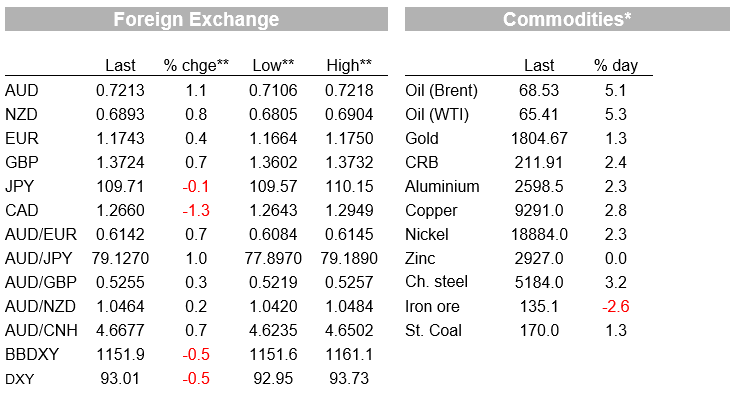

Risk assets have enjoyed a positive start to the new week with European and US equities extending Friday’s rebound. Encouraging covid news seemingly the catalyst for a solid improvement in sentiment. A 5% gain in oil has led the gains within commodities while pro- growth G10 currencies are up over 1%. AUD is back above 72c while the Kiwi is toying with a break above 69c. Mixed PMI news came and went with little market impact.

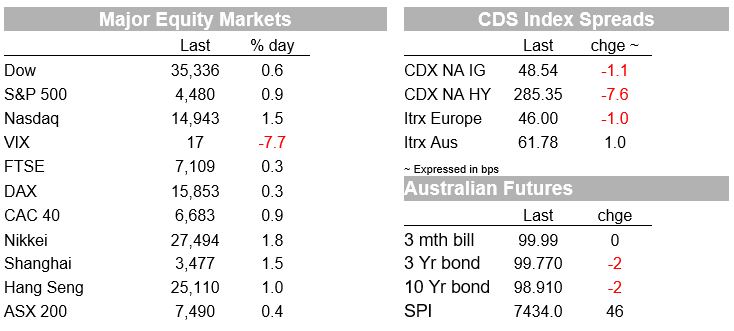

After a positive lead from Asia, European and US equities closed the Monday session with gains across the board, extending Friday’s rebound. The S&P 500 gained 0.85% with the energy sector jumping 3.77%, mimicking the big jump in oil prices ( WTI and Brent gained over 5%), consumer discretionary and IT also had a good day, both up over 1% while defensive sectors such as real estate and utilities were sold, down 0.40% and -1.32% respectively. All major European equity indices closed with gains between 0.28% and 0.86%, the Stoxx 600 index gained 0.7% with pro cyclical sectors leading the way.

Encouragingly covid news around the glove has seemingly been the catalyst for the big improvement in sentiment while mixed PMI news didn’t elicit much of a market reaction. Yesterday, China reported zero new community cases of COVID19 for the first time since its current outbreak began just over a month ago, showing some success with its stringent lockdowns and restrictions. Late last night, following a meeting analysing money and credit aggregates, the PBoC released a statement calling for efforts to push down real lending rates and pledging to support the economy with appropriate money growth . The PBoC Governor Yi said that the central bank would boost credit support for the real economy, especially small companies.

US Covid news have also been a little bit more promising; numbers remain elevated but there some positive signs pointing to the potential that a peak in infection rates has been or is very close to been reached. Numbers are falling in the original delta-variant hotspots such as Missouri and Arkansas, where new cases are down 12% from their peak. There is also a slowing in new case numbers for Florida and Louisiana, two states that followed the initial delta wave. The rest of the US is seeing rising daily case numbers, but at a slower pace.

Overnight the FDA granted full approval to the Covid-19 vaccine made by Pfizer Inc. and BioNTech. The approval is the first for a Covid vaccine in the US and it is expected it will boost the immunisation, as the approval should increase confidence on the vaccine safety and effectiveness. Bloomberg also notes that many large US employers, colleges and universities as well as state and local governments are expected to put vaccine requirements in place in the wake of the approval.

The positive covid news appears to have been a key catalyst for the rebound in commodity prices over the past 24 hours. Oil prices have led the rebound with Brent and WTI up over 5%, going a long way to recovering last week’s loss. Copper has also extended Friday’s rebound, up over 2% with other metals recording similar gains. Iron ore was the exception, down 0.71% overnight.

The positive risk backdrop along side gains in most commodities provided a boost to pro growth currencies while the USD was broadly weaker. The greenback is down just over 0.5% in index terms with all G10 pairs including safe havens such as JPY and CHF outperforming the USD. CAD, NOK and AUD are at the top of the leader board, up over 1% with NZD a little bit behind, up 0.85%. After threatening to break into the 70c handle late last week, overnight the AUD climbed above 72c and now trades at 0.7210. Meanwhile NZD is at 0.6892, after spending a brief time above 69c a couple of hours ago.

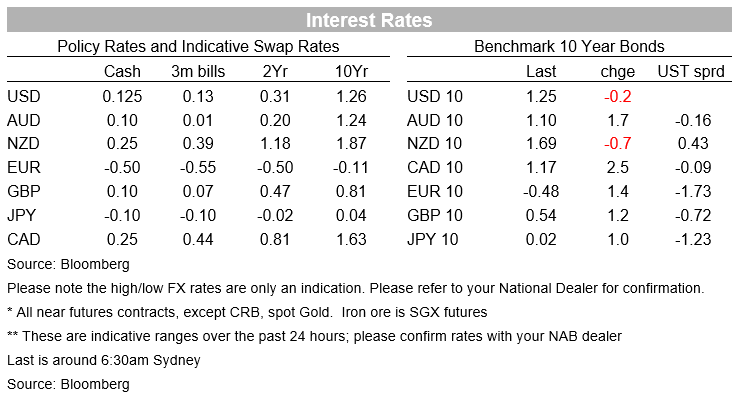

In quite a stark contrast to price action seen in equities, FX and commodities, core global yields have essentially been bystanders 10y rates showing about 1 bps change over the past 24 hour . The 10y UST rates is now at 1.25% after trading in a tight range overnight. The Fed’s Jackson hole symposium later in the week looms large and its likely keeping traders on the sidelines.

Overnight economic data releases haven’t had any noticeable impact on the market. PMI data released were a mixed bag. In the euro area, services PMIs held up at very strong levels, while Germany’s manufacturing PMI was notably weaker than expected, albeit apparently more a reflection of supply shortages. Separately, German’s Bundesbank flagged that Germany’s economic rebound could be weaker than expected as the delta variant and slowing vaccination rates could lead to stricter protection measures.

In the UK, the more important services PMI fell by much more than expected, but this likely reflected the “pingdemic” (since largely ended), resulting in significant staff shortages as they self-isolated at home following potential exposure to COVID19.

In the US, the services PMI also came in much weaker than expected, falling to an eight-month low, but again reflecting supply side issues, with the survey compiler Markit reporting increasing frustrations in relation to hiring staff. US existing home sales unexpectedly rose, up 2% to 5.99m, with a seasonal lift in inventory helping meet increased demand.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.