Online retail sales growth slowed in May following a fairly strong April

Insight

ECB’s Visco says “there is a risk of a recession” and that ECB policy can’t drive down gas prices.

https://soundcloud.com/user-291029717/when-is-a-recession-not-really-a-recession?utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

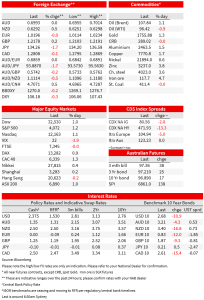

Another day when bad news is good for (risk) markets, the reported 0.9% contraction in US Q2 GDP and so meaning that on one, albeit flawed, definition the US was in recession in the first half of the year, seeing US bonds sharply extend their post-FOMC rally, 10 year Treasuries 11bps lower than Wednesday’s NY closing levels and 2s off 13bps. US (and most European) equities are keying off the rates signal not the economic headlines, the S&P 500 and NASDAQ both ending the day up more than 1%. Lower yields and positive risk sentiment is tried and trusted recipe for a softer USD, which is about a quarter of a percent lower, albeit a move that is flattered, as the day before, by smartly lower USD/JPY levels. Currencies aren’t much changed elsewhere, including AUD.

Definitely a night for the algo traders, whose machine reading of the -0.9% US Q2 GDP headline (against a +0.4% consensus estimate) saw the SPI futures swiftly losing 1% and US 10 year Treasuries fall from around 2.78% to as low as 2.65% and the USD – because of the initial equity signals – initially bought. The subsequent human intervention has seen the bond market rally preserved but equities investors liking the lower rates signal (adding to their – debatable – conclusion that the Fed has lost some of its hawkishness this week).

As for the detail of the GDP numbers, while the fall in inventories was a significant part of the story, subtracting an annualised 2.0% from growth in the quarter, consumption growth slowed to just 1%, after 2 1/4% in H2 2021 and 1.8% in Q1. Fixed investment was weak, with equipment spending down 2.7% and housing investment falling 14.0% – it’s not at all obvious they will bounce back in Q3. Government spending somewhat surprisingly fell by 1.9% (some suggestion it will be revised up) while net foreign trade contributed 1.4pp and should do so by even more in H2 as imports mean-revert lower and now that inventory levels have been rebuilt by many firms.

Also to note in the GDP data, the PCE deflator rose by 8.7% (annualised rate) from 8.2% in Q1 and 8.0% expect, though the core PCE deflator fell back, to 4.4% from 5.2% as expected.

In other US economic new overnight, weekly jobless claims printed another above trend result of 256k (from a revised 261k) but the numbers are being distorted by annual automakers’ retooling and associated seasonal adjustment issues. A (gently) rising trend looks to be the underling story, which should show up in weaker employment growth and, potentially, a rising unemployment rate in coming months.

The Kansas Fed manufacturing Activity index surprised to the upside (13 from 12 and 4 expected) so a rather mixed picture so far from regional July PMIs. The ISMs next week will be important to see if they corroborate the weak picture in last weeks’ S&P Global PMIs, in services especially.

The economic news out of Europe continues to make grim reading. Following last week’s poor PMIs and weaker German IFO survey, the various European Commission confidence indicators were all very soft. Economic Sentiment is down from 103.5 in June to 99.0 in July (the composite PMI, recall, was down from 52.0 to 49.4). Industrial confidence (3.5 from 7.0) and Services sentiment (10.7 from 14.1) both weaker than expected; and while consumer confidence was unchanged, it was still at the lowest level for over two decades.

On the inflation front, more unpleasant news with German CPI, on the EU harmonised (HICP) measures, printing a higher than expected 8.5%, up from 8.2% in June and 8.1% expected.

Fed official have so far remained silent post the FOMC, while latest ECB speak came from GC member Visco, ECB’s Visco who says, “There is a risk of a recession,” and that should this happen, the ECB would “need to discuss what to do.” He notes ECB policy can’t drive down gas prices and that the ECB must avoid ‘too strong’ messages.

Back to markets and the 1.2% overall gain for the S&P500 is broad based, led by Real Estate (and where we’d note 30-year bond yields are almost back to 3%), Utilities and Industrials. Post close, Intel, Amazon and Apple have all reported Q2 earnings. Amazon jumped 10% after estimating Q3 net sales to be $125-$130bn against a street consensus for $127bn, while Intel fell 9% after a big miss on its last quarter earnings and lowered guidance for the current quarter. Apple just beat its $82.76bn revenue estimate ($83bn) and its stock is currently up around 3%

US Treasuries are ending the New York day with 10s 11bps lower at 2.675%, the lowest close since 7 April, and 2s an even bigger -13.5bp at 2.86%. In FX this has unsurprisingly shown up in another big fall in USD/JPY , its lowest in about 5 weeks. Moves elsewhere have been slight save for a 0.5% rise for the Swiss Franc and 0,.4% gain for the NZD, AUD/USD ending the New York day unchanged just beanth 0.70 (0.6990).

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.