Long-term signal vs. Short-term noise

Insight

US economic data on Friday underscored the inflation challenge facing the Fed

https://soundcloud.com/user-291029717/no-inflation-slowdown-just-wishful-thinking?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

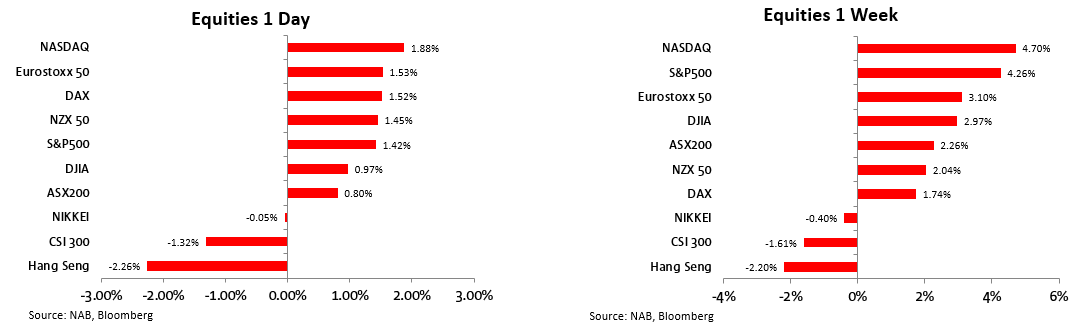

Equities extended gains on Friday, this time helped by reports from tech and oil companies, seeing the S&P500 higher on the day to close out their best month since November 2020. Since the FOMC on Wednesday, markets look to be betting the Fed has done the lion’s share of its task on inflation and will be receptive to slowing activity data, helped by softer Q2 GDP on Thursday.

Initial noises out of the Fed on Friday provided some departure from the market’s interpretation of last week’s FOMC meeting, but like Powell stopped short of providing more explicit guidance. The Atlanta Fed’s Bostic said he doesn’t think the economy is in a recession, citing jobs growth. He emphasised “we really need to address the high levels of inflation and get this economy back into a more stable and sustainable situation, ” and said he was ‘convinced’ the Fed would need to more, but how much will be informed by the data flow. There are two payrolls prints and two CPI’s ahead of the Fed’s September meeting. Minneapolis Fed President Neel Kashkari, in an interview with the New York Times, said “I’m surprised by markets’ interpretation.” “The committee is united in our determination to get inflation back down to 2%, and I think we’re going to continue to do what we need to do until we are convinced that inflation is well on its way back down to 2% — and we are a long way away from that.”

US economic data on Friday underscored the inflation challenge facing the Fed . The PCE deflator rose 0.9% m/m against 1.0% expected and 6.8% y/y. The core deflator accelerated to 0.6% m/m and 4.8% y/y. That worrisome result was largely flagged by the earlier CPI number. The spending indicators in the release were broadly consistent with the earlier Q2 advanced GDP release, showing a 0.1% m/m rise in real spending (consensus 0.0% m/m). The final University of Michigan Consumer Sentiment was revised higher to 51.5 from 51.1. The closely watched 5-10yr inflation expectations series was revised only slightly to 2.9% from 2.8, nothing to see there. Elsewhere, the Chicago PMI was disappointing, falling to its lowest level since mid-2020, at 52, and pointing to downside risks to tonight’s national ISM manufacturing survey.

Of more interest for the inflation outlook was the Employment Cost Index, which did nothing to ease concerns that tight labour markets risk sustaining too-high inflation. Average hourly earnings data had been suggesting a deceleration in wages growth, but alternate measures such as the Atlanta Fed wage tracker were not. The ECI rose 1.3% q/q against 1.2% expected, while the private wages and salaries accelerated to 1.6% q/q and 5.7% y/y. Those are rates faster than last quarter, faster than 2021, and much too high for at-target inflation. Harvard Economist Jason Furman points out there’s a glimmer of hope in a favourite series of the Fed, the private series excluding incentive paid occupations, which slowed to a still high seasonally adjusted 1.3% q/q. But the Fed would not want to be looking quite so hard to be confident inflation will slow.

Also of some interest, Fed Governor Waller put out a research note with colleague Figura assessing that “a soft landing is a plausible outcome for the labor market” pushing back against the well-publicised view of Larry Summers, from a paper with Olivier Blanchard and Alex Domash, that a much higher unemployment rate was needed to cool inflation. Waller and Figura conclude “the increase should be significantly smaller” because of unprecedentedly elevated vacancies.

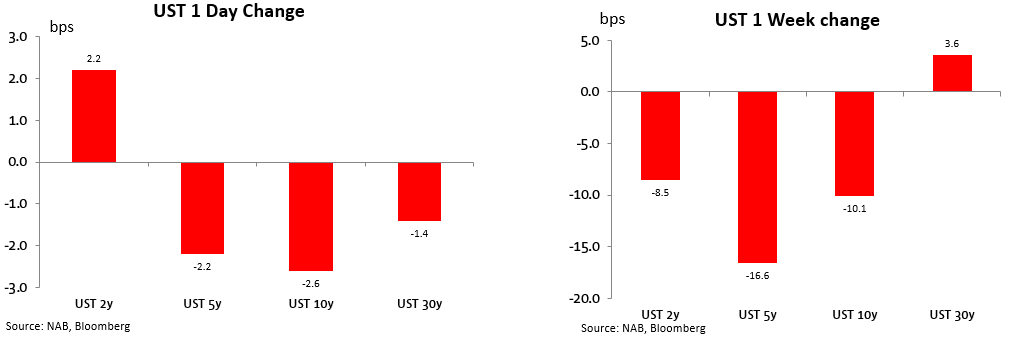

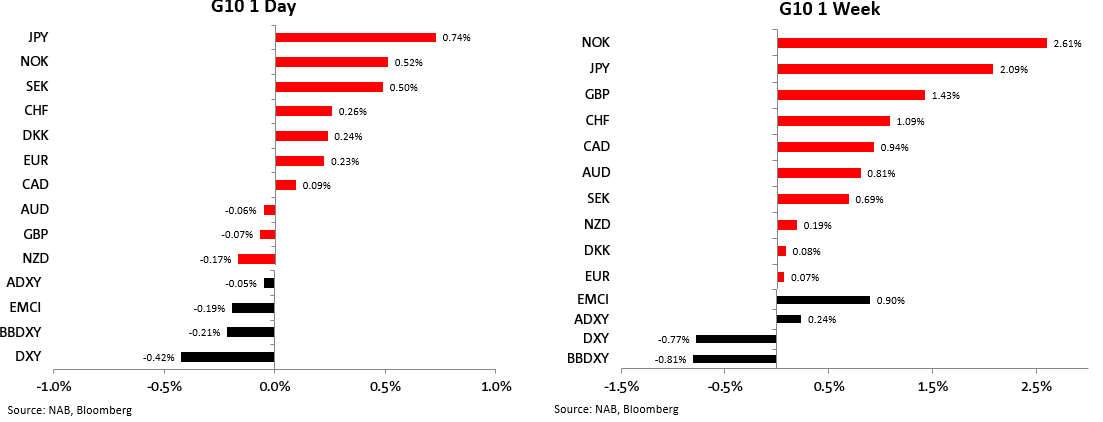

Bostic’s comments and the US data initially helped 2yr yields and the US dollar higher, but they didn’t hold on as the day progressed. The 2yr yield up just 2bp after being as much as 8bp higher, and the DXY down 0.4% at 105.90.

In rates markets, US yields moved deeper into inversion on Friday , the 2yr gaining 2bp and the 10yr losing 3bp. Over the week, the combination of an interpretation of a growth-sensitive Fed with not much more to do on rates and soft Q2 GDP data saw yields lower. 2yr yields were 3.06% heading into the FOMC meeting on Wednesday and have since fallen 17bp to 2.88. Near term Fed pricing is not too dissimilar to the June dot plot, which Powell noted was still a reasonable guide, with 3.31% priced by year end, up 6bp on Friday and in line with the median dot. But where the dots had 50bp of further hikes through 2023, markets price 60bp of cuts.

In Europe, Bloomberg reported the leader of the right-wing Brothers of Italy party, which is currently leading in the polls, plans to abide by EU fiscal rules and stick with previously agreed economic reforms if it comes to power after the upcoming election. The Italy-Germany 10-year bond spread fell 14bps on Friday, to 220bps, but remains significantly wider than earlier this year. Over the week, yields were lower, with German 10yr yields down 21bp to 0.82%, while Italian 10yr yields were down 29bp.

As for the European data flow, Euro Area GDP beat expectations, rising 0.7% q/q vs 0.2% q/q expected. The rebound alongside re-opening winning the day over energy crisis for now, with much of the strength coming from the more tourism-exposed south, though little detail is available in the advance read. CPI data also came in a little higher than expected at 8.9% y/y, up from 8.6% and 8.7% expected . Energy and food prices remain significant contributors to Eurozone inflation (+39.7% y/y and +9.8% y/y respectively) but they are far from the only story, with core (ex food and energy) inflation hitting 4%, a fresh high for this series. The core read pushed higher to 4.0% from 3.9. The market is still pricing a high chance of a 50bps hike from the ECB at the upcoming meeting in September but only around 50bps of additional rate hikes beyond that point.

In other data flow, over the weekend, China’s official PMIs came in weaker than expected. The Manufacturing PMI fall back into contraction territory at 49.0 from 51.2, sharply softer than the 51.4 expected. The more export focussed Caixin version is coming up today. The Services PMI fell to 53.8 from 54.7. That comes after news late last week that Chinese leaders all but acknowledged that the country would miss its annual growth target for this year as it stayed the course on strict covid policy, dropping reference to the 5.5% target in favour of seeking an economy within “ a reasonable range.”

Equities on Friday were supported by strong earnings. Amazon shares were 10% higher after the company said its quarterly revenue grew faster than expected and Apple shares were 3.3% higher on continued growth in iPhone sales. Chevron (+8.9%) and Exxon Mobil (+4.6%) each reported strong profit numbers. But gains were reasonably broad based, with 9 of 11 sectors advancing. Shares in Europe were also higher, the Eurostoxx 50 up 1.5%. Chinese shares were lower after the Politburo on Thursday stopped short of announcing any new bond quotas or pull forward bond quotas allotted for next year even as it said that it would introduce policies to expand domestic demand to keep growth in a ‘reasonable range.’

Over the week, equities were buoyed by a pullback in Fed rate hike bets, as well as some positive signals during earnings season. 75% of firms reporting so far have beaten estimates. That helped the S&P500 up 4.3% over the week to end July 9.1% higher, its best month since November 2020. Can that tone persist against a Fed still laser focussed on inflation?

Currencies had a volatile Friday. The AUD ended up little changed at 0.6986, down 0.1% against the USD, but only after trading as high as 0.7032 before reversing sharply lower to 0.6911 , the move starting after Bostic’s comments and extending on the release of the PCE and ECI. Should the market continue to hear what it wants from the Fed, the aussie can readily spend more time above 0.70, but 0.65-0.70 is still seen containing most of the price action in coming months. The yen gained 0.7% against the dollar, to be 2.1% higher over the week as lower yields across other advanced economies supported. The USD has lost 4.4% against the yen since its recent high of 139.41 on 14 July. The dollar was 0.8% lower over the week on the DXY

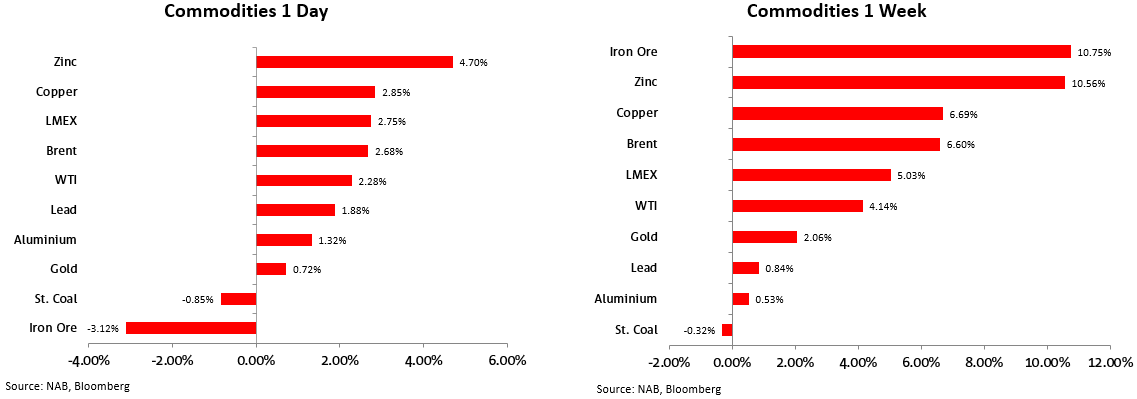

Looking at commodities, iron ore was the outperformer over the week . Iron ore was up 10.8% higher even after a 3.1% decline on Friday, supported earlier in the week amid optimism around stabilisation in market conditions after support for Chinese property developers from lenders. Copper is 6.7% higher over the week to be 11% higher than its recent 14 July trough. Oil rose over the week, with Brent 6.6% higher to US$103.97/bbl.

In other news, Europe’s energy crisis shows no sign of resolution, with news over the weekend that Russia has cut of gas to Latvia after accusing it of violating supply conditions. Russia has already cut gas to Poland, Bulgaria, Finland, Netherlands and Denmark due to its requirement to pay using a rouble account. Latvia said the move would have little effect on the country, which had already banned exports from 2023.

Looking at the rest of the week:

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.