Online retail sales growth slowed in May following a fairly strong April

Insight

Data releases over the past 24 hours have provided further evidence the global economy is slowing. China’s Caixin Manufacturing PMI confirmed that China’s reopening rebound is over.

https://soundcloud.com/user-291029717/recession-signs-rba-to-hike-grains-from-odessa?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

NZ: Dwelling consents (m/m%), Jun: -2.3 vs. -0.5 prev.

CH: Caixin manufacturing PMI, Jul: 50.4 vs. 51.5 exp.

GE: Retail sales (y/y%), Jun: -1.6 vs 0.3 exp.

EA: Unemployment rate (%), Jun: 6.6 vs. 6.6 exp.

US: ISM manufacturing, Jul: 52.8 vs. 52.0 exp.

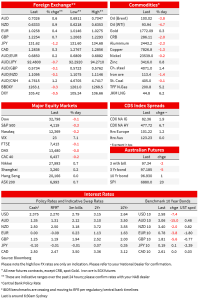

US and EU equities tread water notwithstanding another round of softer activity readings and heightened geopolitical tensions. China Caixin manufacturing PMI reaffirmed the message from the official reading indicating China’s reopening activity burst is over. The US ISM manufacturing printed better than expected, but signs of a slowdown are building. Meanwhile, House Speaker Nancy Pelosi is expected to arrive in Taipei today with China again warning of potential military or economic retaliation. Against this backdrop core yields have traded lower with the 30y Bond leading a flattening of the UST curve. The USD has extended its decline for a fourth consecutive day with JPY the outperformer again. AUD and NZD also appreciate while CNY loses ground

The S&P 500 ( -0.28%) and NASDAQ (-0.18%) have closed marginally lower, but a look at the intraday chart shows the overnight session was a volatile one (the VIX closed 1.5 point higher at 22.84) . Both benchmark indices opened sharply lower with geopolitical concerns not helping sentiment while details from the ISM released shortly afterwards contributed to the undecidedness in the air. Still, relative to the moves in core yields (more below), equity investors remain relatively relax with the US earnings reporting session showing a bit more resilience than expected while (misplaced?) expectations the Fed will pivot amid a slowdown in economic activity may also be a consideration.

Heightened geological tensions are seemingly not having a major impact on equity sentiment either. Pelosi’s office has yet to confirm her Taiwan visit, but speculation of her visit is rife with the local media confirming her arrival tonight and meeting with Taiwan’s President on Wednesday . China has previously warned against the visit from such a high-profile US government official and has threatened military action. China’s Foreign Ministry spokesman said that the army “won’t sit idly by”, while Chinese media suggest that the army would respond aggressively. Meanwhile the White House has urged Beijing for calm, National Security Council spokesman John Kirby said “there is no reason for Beijing to turn a potential visit consistent with long-standing US policy into some sort of crisis or conflict or use it as a pretext to increase aggressive military activity,”. But then he suggested several action China may consider, including firing missiles into the Taiwan Strait, launching new military operations, crossing an unofficial no-fly zone between Taiwan and the mainland and making “spurious” legal claims about the strait.

Data releases over the past 24 hours have provided further evidence the global economy is slowing. China’s Caixin Manufacturing PMI confirmed the message from the official reading, that is that China’s reopening rebound is over. Output fell to 52.0, from 56.4, and new orders fell more modestly, to 50.3, from 51.2. New Covid outbreaks have been more limited in the regions where the Caixin survey is run, suggesting the decline in activity has more to do with a genuine slowdown and fading of the reopening bounce. Price pressures were also lower in July, though input prices did not see the same collapse that the official measure reported.

Meanwhile in Europe, the final PMIs confirmed the euro area’s four largest members activity contracted in July. Then in the US, the ISM manufacturing index fell to its lowest level in more than two-years to 52.8, but by not as much as feared, with the consensus expecting a drop to 52.0. However, details in the report where not encouraging, the survey’s gauge of new orders remained in contraction territory for a second month while the inventories index rose to 57.3, the highest since 1984, suggesting stockpiles are mounting at more manufacturers. The new orders less inventories index is widely monitored, and this fell to a level consistent with economic recession. On the positive side, the employment index increased to 49.9 with the decline in prices paid also a positive surprise, falling 18.5 points to the lowest level in almost two years with recent weaker commodities prices a factor at play.

Linked to the above theme, worth noting too that Germany’s retail sales fell by 8.8% y/y in real terms in June, the weakest result since this index began in 1950 . This data can be volatile, but the sharp decline is notable and could result in a downgrade to Germany’s Q2 GDP flat preliminary reading and mark the start of Germany’s recession. This, well ahead of a winter that has the real risk of energy rationing, resulting in an additional decline in economic activity.

The softer activity readings around the globe have contributed to a decline in commodity prices with

Oil prices extending their July declines. Brent Crude is now toying with a new a break below $100 per barrel while WTI is at $94.07.

Core global yields have shown a greater degree of sensitivity to the data and geopolitical tensions, trading lower across the board. % The rally in bond markets continues with a bias for flatter curves, particularly in the treasury market where the 2y10y curve is currently 6.5bps flatter at -30bps. The US 10-year bond is at its intra-day low of 2.57%. While in Europe, 10y Bund closed 4bps lower to 0.78%.

In FX land, the USD has extended its decline to a fourth day in a row with DXY down 0.46% and BBDXY -0.33%. Within G10, JPY is the outperformer again, up 1.2% with USD/JPY down to £131.64 and with some technical room to test levels close to £130, if not lower. The decline in 10y UST yields of course helping too.

The AUD and NZD have gained ground against the USD, notwithstanding the risk aversion in the air. NZD rising to as high as 0.6350 overnight and currently at 0.6333. The AUD met some resistance just under the 0.7050 mark and has settled around 0.7027. Of note, both antipodean currencies have not shown any reaction to Yuan weakness, with USD/CNY up 0.4% to 6.7688, a theme to watch over coming days.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.