A private sector improvement to support growth

Insight

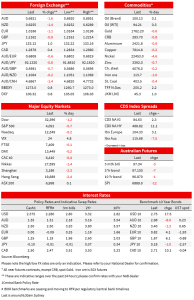

In Australia, the RBA met yesterday and raised the official cash rate by 50bps to 1.85% as expected, the third consecutive 50bps increase to be at its highest level since April 2016.

https://soundcloud.com/user-291029717/pelosi-in-taiwan-fed-nowhere-near-almost-done?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Global yields have surged led by the belly as Fed speakers make a co-ordinated effort to push back on the markets interpretation of Powell post FOMC. Some geopolitical risk premium has also come out of the markets with Pelso making a safe landing in Taiwan. Mary Daly led the charge by the Fed, stating the Fed is “nowhere near almost done”, followed by Evans who said for the September FOMC “50 is a reasonable assessment, but 75 could also be okay”. Importantly in Evan’s view rates needed to go to “a sufficiently high level ” of 3.75% to 4% by Q2 2023. The end result is yields are broadly where they were prior to the FOMC last week. The 2yr yield is up 17.5bps to 3.05%, the 10yr is up by a similar 17.7bps to 2.75% and the 2/10s curve remains well inverted at -30.5bps. Fed Funds pricing now has a peak of 3.40% in February 2023, up from 3.27% yesterday. Pricing of cuts in 2023 has also been pared with 49bps of cuts now priced, compared to 58bps on Monday. The USD rose on the yield backdrop with the DXY +0.8% and making broad-based gains. The AUD (-1.6%) was the weakest in the G10 following the RBA’s more ambiguous language yesterday. Equities fell with the S&P500 -0.7%.

As for US House Speaker’s Pelosi trip to Taiwan, that has seemed to proceed without too much geopolitical angst. Pelosi arrived safely in Taiwan at 10.44pm local time and is the first House Speaker to visit in 25 years. In the lead up to the event there was some geopolitical risk premium being priced with Monday seeing gold up, yen strength and yields lower. That has started to reverse out with China making a strong, but importantly not an “unhinged ” response. China sent fighter jets over the Taiwan Strait and the Xinhua News Agency has report China would conduct live fire exercises in the airspace and sea waters around Taiwan for four days starting Thursday noon. No surprises then to see USD/Yen +1.0% to 133.12, Gold -0.6% to 1,762. The unwinding of this premium also likely added to the rise in yields as noted above. As for the political theatre, Pelosi made an editorial supporting Taiwan, while it Biden is contemplating cutting tariffs against China to lower inflation – all ahead of the November mid-terms.

Fed speak dominated the session and was the catalyst for the surge in yields. First up was the Fed’s Mary Daly who said the Fed was “nowhere near almost done” on its fight against inflation. Daly noted “…we are still resolute and completely united on achieving price stability, which doesn’t mean 9.1% inflation. It means something closer to 2% inflation, so a long way to go,” and importantly for markets which are pricing in cuts in 2023, fighting high inflation requires “raising and leaving the interest rate for a while” on hold. Evans made similar hawkish comments and also noted that at the September FOMC meeting “50 is a reasonable assessment, but 75 could also be okay ”. As for the pace of hikes, Evans favours 50bps in September and then stepping down to 25bps increments to take the Fed Funds Rate to a “a sufficiently high level” of 3.75% to 4% by the end of Q2 2023. Mester rounded out Fed talk, noting that she needs to see compelling evidence of several months of inflation coming down, noting that so far “I haven’t seen anything suggesting inflation is levelling off”.

As for data, it was mostly second tier. The US had JOLTS which printed lower than expected at 10,698k against 11,000 expected. There are now 1.8 job openings per unemployed person from its March high of 1.99, but is still very much indicative of a tight labour market. There was little change in the quits rate of 2.8%. The Fed has been looking to job openings falling in trying to achieve a soft landing. There has been some debate whether this is possible, with Summers and Blanchard refuting work by Fed Governor Waller. Regarldess, what JOLTS does show is some labour demand is easing, but perhaps not rapidly enough to bring wages under control as illustrated in last Friday’s ECI.

Finally in Australia, the RBA met yesterday and raised the official cash rate by 50bps to 1.85% as expected, the third consecutive 50bps increase to be at its highest level since April 2016. The Statement repeated that “the Board expects to take further steps in the process of normalising monetary conditions over the months ahead”, but also added policy “is not on a pre-set path.” The later addition created some ambiguity around the pace and trajectory for hikes with markets giving a less hawkish interpretation. RBA whisperers in the press play to this ambiguity with the AFR’s Kehoe noting “ a 0.25 or 0.50 of a percentage point rise in September will be a close call, but beyond that point more conventional 0.25 of a percentage point increases are most likely” (see AFR: The size of RBA rate rises will soon ease ). Importantly the inflation profile still suggests the RBA needs to get into restrictive territory higher with inflation set to peak at 7.75% over 2022, remain high at 4% in 2023 and around 3% over 2024. NAB’s view is that seeking a return to 2-3% inflation will likely require at least a slightly restrictive monetary policy setting, which we suggest is in the 2.6-2.85% cash rate range. The RBA’s forecasts foresee only a very modest lift in the unemployment rate to 4% at the end of 2024, after some further decline in the months ahead. NAB expects a 4.5% unemployment rate in 2024.

The markets less hawkish interpretation of the RBA saw a strong rally in the rates market, seeing the 3-year bond yield fall as much as 10bps. However, global yield moves and perhaps a re-think of whether that initial market reaction was appropriate has seen an 18bps reversal, with that rate now some 8bps higher compared to the pre-RBA level. The AUD fell over ½ a cent in the hours after the statement and the USD rebound overnight has kept the AUD from reversing course. The currency is down around 1.6% over the past 24 hours. As for the rest of the G10 currencies it has been a story of USD strength with the DXY +0.8%. Some unwinding of geopolitical angst has seen USD/Yen +1.0% to 133. The EUR is -1.1% and GBP is -0.9%.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.