Total spending grew 1.2% m/m in May

Insight

An all-round stronger than expected US employment report Friday dominated the end-of-week market price action; whether they extend or at least partially reverse this week hinges in large part on Wednesday’s US July CPI data.

https://soundcloud.com/user-291029717/us-jobs-market-too-hot-for-the-fed?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

US July non-farm payrolls 528k vs 250k expected

US non-farm payrolls two-month revisions +28k

US July Unemployment Rate 3.5% from 3.6% and 3.6% expected

US July Average Hourly Earnings 0.5% m/m vs 0.3% expected (June revised to 0.4% from 0.3%)

US July Average Hourly earnings 5.2% y/y from upward revised 5.2% (was 5.1%)

US July Labor Force Participation Rate 62.1% from 62.2% vs 62.2% expected

US June Consumer Credit $40.15bn vs. $27bn expected

Canada July Unemployment Rate 4.9% unchanged vs 5.0% expected

Canada July Net Change in Employment -30.6k vs 15.0k expected

Canada July Participation Rate 64.7% from 64.9% and 64.9% expected

China July trade balance $101.26bn vs $97.94bn expected

China July exports 18.0% y/y vs 14.1% expected

China July Imports 7.4% y/y/ vs 5.7% expected

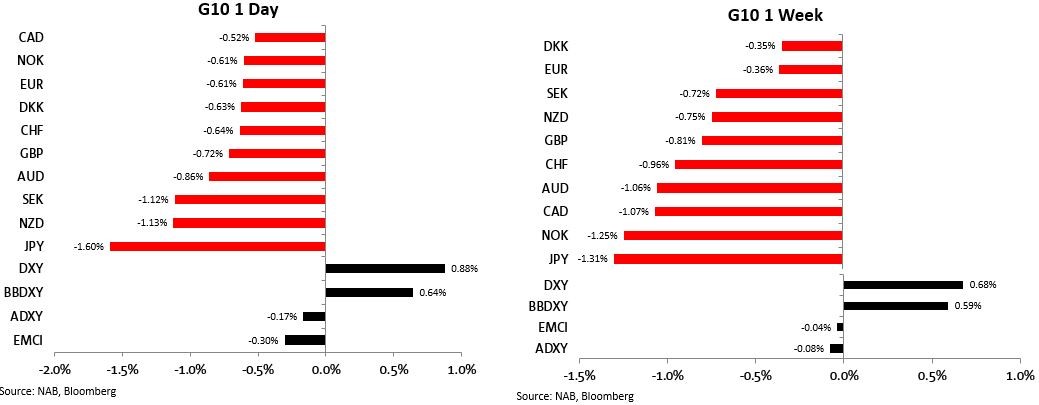

An all-round stronger than expected US employment report Friday dominated the end-of-week market price action. A quite vicious bond market sell off led by the front end of the Treasury curve pushed the 2/10s curve to -40bps (its most inverted since 30 August 2000). Sharply higher yields propelled the USD higher across the board (DXY 0.9%) led predictably by USD/JPY, up a cool 1.6% on the day and with AUD and NZD both down +/- 1%. Somewhat stronger than expected import and export growth figures from China on Sunday might provide a modicum of support for the antipodean currencies at the start of the new week, though the reality is that geopolitical developments aside, whether Friday’s market moves extend or at least partially reverse this week hinges in large part on Wednesday’s US July CPI data.

The 528k headline rise in July US payrolls, more than double the 250k expected, was compounded by a net 28k upward revision to the combined May/June numbers. The Unemployment Rate drop from 3.6% to 3.5%, so matching its pre-pandemic low, owed something to a 0.1% drop in the Participation Rate to 62.1%. This can’t be of any comfort to policy makers though, not seeing the ease of finding a job or switching to a better paid one drawing more folk into the labour force, in turn aggravating fears that wages growth won’t quickly subside. Indeed, Average Hourly Earnings were revised up to 5.2% in the year to June and stayed there in July thanks to a 0.5% monthly rise, which followed a couple of months of 0.4% gains and thoughts earnings growth could soon be back below 5%. If anything, wags growth looks to be accelerating.

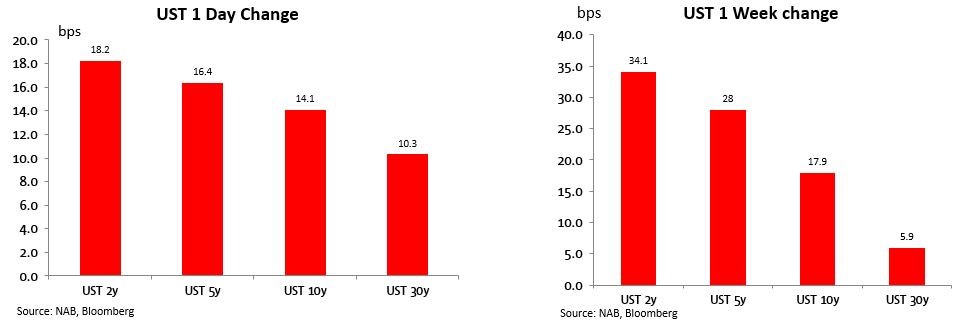

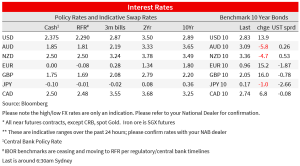

US Treasuries sold off hard immediately upon the employment release and never really looked back over the remainder of Friday’s new York session, jumping quickly from 3.065% to 3.20% and ending the day at 3.225%. 10s didn’t fare much better, yields leaping from 2.70% to 2.80% and ending the week up 18bps at 2.83%.

In the Fed Funds futures market, pricing for the September FOMC meeting shifted from about a 35% probability of the Fed lifting by another 75% on 21 September to a little more than 75%. Terminal Funds Rate pricing lifted from 3.43% (in February 2023) to 3.64% (now March 2023).

Speaking on Saturday, Fed Governor Michelle Bowman said, “My view is that similarly-sized increases should be on the table until we see inflation declining in a consistent, meaningful, and lasting way.” Bowman added that she supported last month’s rate increase and backed the move away from offering specific forward guidance at the press conferences following policy meetings.

Also speaking post Friday’s payrolls report, San Francisco Fed President Mary Daly was not quite so hawkish, saying, “As I think about what’s up next for interest rates, I still think that we need to move them up — of course we don’t need all the support we’ve been giving the economy but we don’t need to be too aggressive. We do already see signs of slowing,” she says in interview on Fox News, adding it takes a while for interest-rate increases to move through the economy. “The good news is people can get jobs. The bad news is that inflation remains too high. And our number one priority is to get that down.”

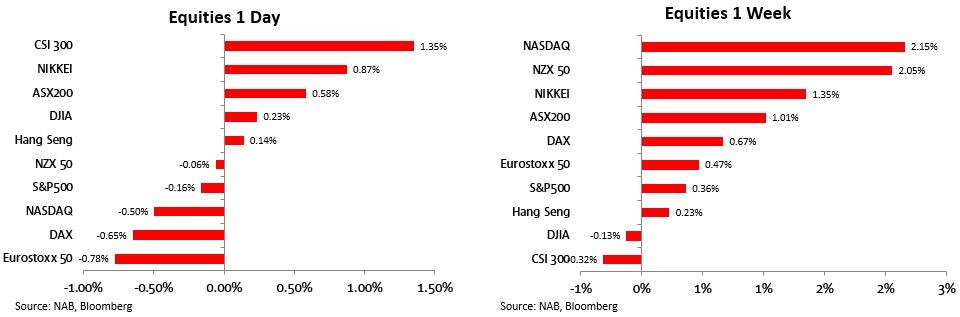

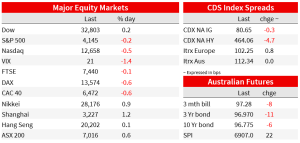

While the signal from the 2/10s yield curve is that a recession in 2023 is looking even more nailed on, equity markets ended up over the whole of Friday apparently taking the bond signal in its stride. Yes, stocks sold off at the open (S&P500 by more than 1%) in line with the jump in discount rates, but losses were almost fully recovered, only for the market to sell off again but almost fully recovering losses in afternoon trade to end the day down just 0.16% (the more interest rate sensitive NASDAQ – -0.5%).

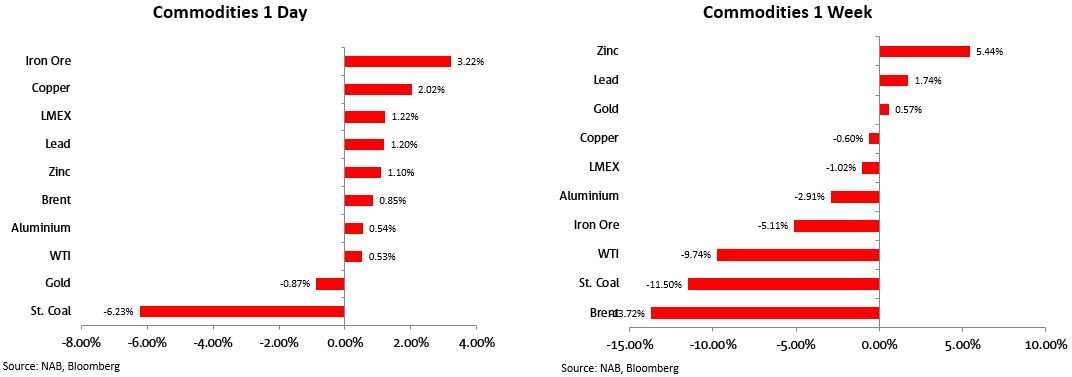

Maybe the recession will never really arrive with the labour market this strong? (plus, according to FactSet, 75% of incoming US Q2 corporate earnings have so beaten their consensus estimate, by on average 3.4%). Consumer Discretionary (-1.7%) was the worst performing sector in the S&P500 Friday, more consistent with the recession signal than the broader market moves, but some offset came from Energy (+2%), in which respect WTI crude rose by 47 cents and Brent by 80 cents. This within what was a very mixed night for commodities but which saw copper up 1.85% and iron ore futures 5% (see chart below).

In currencies, true to recent form USD/JPY showed the most sensitivity to the spike in Treasury yields, rising two big figures to Y135, meaning the pair has now retraced just over 50% of the 14 July through 2 August selloff. The next biggest losers were NZD and SEK, both -1.1% followed by AUD, the latter down 0.9% to a low of 0.6870 (0.6911 at the NY close). AUD has opened the week a touch higher, helped perhaps by Sunday’s China trade data which showed annual export growth of 18%, little changed on June but better than the 14.1% expected, plus a pick-up in import growth to 7.4% from 4.8%, also a little better than expected.

CAD fared less badly than other G10 pairs, USD/CAD only up 0.5%, aided by stronger oil but with mixed messages from Canada’s labour market down (unemployment rate unchanged at 4.9% against a rise to 5.0% expected but employment – a very noisy number in Canada – down 30.6k against +15.0k expected). Friday’s overall FX moves, which saw the DXY USD index +0.88%, rescued the USD from what would have otherwise been a down week (ended +0.68%).

Finally, in the last hour or so the US Senate has, using Vice President Harris’ casting vote, approved the Democrats tax and climate bill (known as the ‘Inflation Reduction Act’) by 50-51. It should be approved by the House of Representatives on Friday. The overall fiscal impact of the bill should be contractionary (i.e. more taxes than spending increases) though some observers will be quick to claim that the spending will likely come before the taxes designed to pay for it and pay down some of the deficit, such that it might add to rather than subtract from inflation in the coming year or more.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 1.2% m/m in May

Insight

Narrowing gap between conditions and confidence

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.