Total spending grew 0.9% in June.

China is continuing its military drills around Taiwan, but that hasn’t impacted markets apart from gold (+0.7% to 1,787.61) retaining some slight geopolitical risk premium.

https://soundcloud.com/user-291029717/markets-in-limbo?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

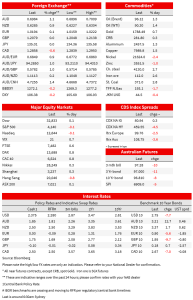

A very quiet start to the week with little news flow of significance. China is continuing its military drills around Taiwan, but that hasn’t impacted markets apart from gold (+0.7% to 1,787.61) retaining some slight geopolitical risk premium. Markets instead have been mulling over Friday’s strong payrolls report with a few more US banks calling a 75bp hike in September. Markets of course got their first on Friday with 69bps priced, now increased slightly to 70bps. As for how high US rates may go, markets price a peak of 3.62% in March 2023, followed by 57bps worth of cuts in 2023. Yields meanwhile consolidated last week’s large moves with 2yr yields down by -1bps to 3.21% compared to larger moves in the 10yr of -7.7bps to 2.75%. That dynamic of course means the 2/10s curve has inverted further to ‑46.0bps, the most inverted in 20 years and continues to drive talk of recession risk (note the largest in modern times was -56bps in April 2000). Meanwhile the USD edged lower with the DXY -0.2%, while equities gave up earlier gains with the S&P500 -0.1% after having been up some 1.0% at one stage. A weak earnings report by Nvidia (-6.3%) was one catalyst for the reversal.

There was little data of significance. One second-tier report that did get a few headlines was the NY Fed’s Survey of Consumer Expectations . That survey reported a fall in inflation expectations across all time horizons with the one year to 6.2% from 6.8%, three year to 3.2% from 3.6%, and the five year which is asked on an ad-hoc basis to 2.3% from 2.8%. The drivers appeared to be expectations of a sharp fall in price increases for gas and food – likely reflective of the decline seen in oil prices to date. The move in inflation expectations broadly supports the movements seen in implied inflation breakevens over the past few months with the 10yr breakeven at 2.48%, well down on its highs of 3.04% back in April. Note another measure of inflation expectations will be out on Friday in the University of Michigan Consumer Sentiment Survey with the Fed closely watching the 5-10yr expectation.

With payrolls strong on Friday, there is lots of focus on equities and whether the current rally can be sustained. In that light Nvidia’s (-6.3%) weaker than expected revenue numbers put pressure on semi-conductor stocks and combined with technicals (the Nasdaq had retraced 38.2% of its losses from its November high) was the catalyst that saw the S&P trade from being up 1.0% at one point, to closing ‑0.1%. Nvidia noted fiscal second-quarter revenue was about $6.7bn, down from its earlier projection of $8.1bn. High end graphic chip demand has weakened with major gaming and pc companies reporting weaker outlooks. Also interesting in terms of financial conditions is a return of meme-stock enthusiasm, with dogs like Bed Bath and Beyond (+39.8%), AMC (+8.4%) and Gamestop (+8.6%) enjoying gains today. Many analysts are taking the gains in meme-stock as a sign that financial conditions are still not tight enough (having loosened since the last FOMC meeting) and that the Fed still has a lot of work to do.

In FX, the USD has given up some of its Friday gain, with the DXY down about -0.2%. The AUD (1.1%) or the NZD (+0.9%) were boosted yesterday, helped by the better than expected Chinese trade numbers as were most commodities. Geopolitical tensions have had little impact even with China’s decision to extend its military exercises surrounding Taiwan, continuing training “under real war conditions”, as the People’s Liberation Army has described it. The EUR (+0.1%), GBP (+0.0%) and USD/Yen (-0.1%) are all been little changed. My BNZ colleague Jason Wong noted in his desperate search to write about something today, found an FT article that Norway is set to curb electricity exports in a blow to European energy supplies. Norway’s hydro lakes are low and there is political pressure to refill the reservoirs rather than pump out electricity to export to the UK, Germany, Netherlands and Denmark. An export curb here can only add to the evolving energy crisis in Europe, one that looks to intensify as winter approaches. The story hasn’t affected the market, with the euro flat on the day and European gas futures settling lower.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.