Total spending grew 0.9% in June.

The San Francisco Fed’s Mary Daly warned it is too early to ‘declare victory’ over inflation.

https://soundcloud.com/user-291029717/not-convinced-by-the-fed?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

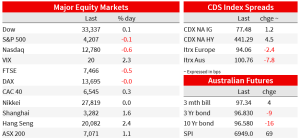

It was a relatively quiet night in markets following yesterday’s reaction to softer-than-expected CPI data. US equities largely held onto yesterday’s gains while the USD dollar held onto its declines. The S&P500 was little changed at 0.1% and the dollar was 0.1% lower on the DXY. In contrast, there was more movement in rates markets with US 10yr yields 10bp higher alongside similar moves in other markets.

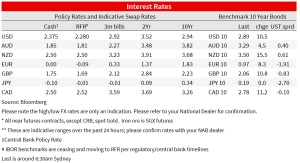

The San Francisco Fed’s Mary Daly warned it is too early to ‘declare victory’ over inflation. Her sentiments mirrored those of Evans and Kashkari the day before. Daly described the month-to-month data as ‘good news’ but added “inflation remains far too high and not near our price stability goal. ” While not ruling out another 75bp hike, Daly did say a step down to 50bp in September was her baseline. Market pricing has been pared to around 62bp for the September meeting from 68bp prior to the CPI report and implies a peak of around 3.6% in February 2023.

Bond yields were generally higher globally and curves steeper. The US 10yr yield was 11bp higher to 2.89%, its highest levels since 22 July while 2yr yields were 2 bp higher at 2.34%. Those moves take the 2s10s inversion to less extreme levels at -35bp compared to -48bp prior to CPI. Higher longer-term yields also seen elsewhere. The German 10yr was 8bp higher to 0.97%.

US equities initially extended yesterday’s gains, up as much as 1% intraday before paring gains to finish 0.1% lower. Energy stocks led gains on Thursday, while tech and consumer discretionary, which have outperformed in recent weeks, saw declines. The Nasdaq was 0.7% lower after yesterday’s 2.9% gain. At face value, equity markets seem to be interpreting the positive inflation news as bolstering prospects for a soft landing and a shallower tightening cycle. European markets were mixed with the Euro Stoxx 50 0.2% higher.

With little new news flow to speak of, currency markets generally showed small moves. The US dollar is down 0.1% on the DXY at 105.1 following yesterday’s 1.1% decline. Moves were mixed against G10 currencies but generally small. The AUD held onto its appreciation yesterday, up 0.2% and sitting at 0.7106. That’s after hitting a high of 0.7137 overnight, the highest level since 10 June.

The data flow overnight saw US PPI come in below expectations , but there was little market interest following Wednesday’s more closely watched consumer prices. For the record, producer prices declined 0.5% m/m, below the 0.2% expected, while producer prices excluding food and energy was also softer at 0.2%m/m vs 0.4%. That difference accounted for by a 9%m/m fall in energy prices. US retail fuel prices also continued their decline, dropping below $4 a gallon on Thursday and 20% below their mid-June peak. Weekly initial jobless claims were 262k against 265k expected and from a downwardly revised 248k . Seasonal adjustment at this time of year makes interpretation difficult, and the downward revision a useful reminder of the health warnings attached to higher frequency data. Overall, though, initial jobless claims remain consistent with a gradual trend higher from very low April levels.

Brent oil was 2.2% higher to US$99.53/bbl and WTI was 2.5% higher amid contrasting assessments of the outlook from the IEA and OPEC. The IEA says world oil consumption will increase by 2.1 million barrels a day this year, or about 2%, up 380,000 a day from their previous forecast as high natural gas prices and heatwaves spur generators to switch to oil. That contrasts with the assessment from OPEC, which expects global oil markets to tip into surplus this quarter as it downgraded the outlook for demand and increased estimates for non-OPEC+ production. The IEA also said OPEC+ is unlikely to increase output in the coming months because of limited spare capacity

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.