NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Equities continued their relentless rise, brushing off the inflation expectations data and hawkish Fed rhetoric

https://soundcloud.com/user-291029717/a-positive-outlook-apart-from-the-downturn?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

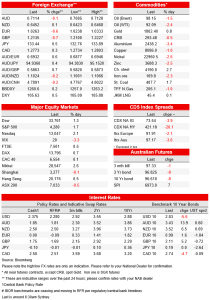

Another wild ride for equities on Friday with the S&P up 1.7% to 4,280 to be now 16.7% off its mid-June lows and only -10.8% from its all-time high of early January 2022. The stark rally in equities since mid-June has been driven by a squeeze of bearish positioning following the generally better than expected earnings for large tech stocks, some notion that the Fed was close to a pivot after Powell’s neutral comment, and more recently the softer CPI/PPI reports hinting that inflation may be peaking. The bond market in contrast is not as optimistic. Short end yields on Friday reversed their initial drift lower following a hotter than expected University of Michigan 5-10yr consumer inflation expectations print (3.0% vs. 2.8% expected and 2.9% previously), alongside the Fed’s Barkin who again pushed back on the notion of a Fed pivot and of the markets pricing of cuts in 2023. The US 2yr yield rose 1.8bps to 3.24% while the 10yr fell -5.6bps to 2.83%. Fed funds pricing moved incrementally higher with a peak now of 3.66% in March 2023 from 3.63% on Thursday, and markets continue to price around a 50% chance of a 75bp hike at the upcoming September FOMC. The USD (DXY+0.5%) was stronger, and the AUD and NZD outperformed.

Key for sentiment this week will be US Retail Sales on Wednesday, along with major earnings reports from retailers including Walmart, Home Depot (Tuesday) and Target (Wednesday). A growing narrative of a soft landing has taken hold, gaining traction after some easing in price indicators with some interpreting that as allowing the Fed to ease up on the pace of hikes. The FOMC Minutes on Wednesday may push back on the notion of a Fed pivot though as has recent hawkish Fed commentary. It is also a big week for Australia with Wages on Wednesday and Employment on Thursday, and before that the RBA Minutes on Tuesday. Across the ditch the RBNZ meets where expectations are for a 50bp hike to 3.0% (see Coming Up below for details). Weekend news has been quiet so it is likely to be a quiet start to the week until the major risk events from Wednesday. The only mild sliver of interest for an Australian audience was the SMH writing the government is looking to increase the migration cap from its current 160k to 180-200k in the upcoming October Budget amid the tight labour market (see SMH: Labor to bring in tens of thousands more migrants as it eyes bargain with union movement).

First to the data. The University of Michigan Consumer Sentiment was better than expected at 55.1 vs. 52.5 expected and 51.5 previously. A lot of focus was given to the headline beat, though it is worth noting that even with the rise consumer sentiment is still lower than what was seen in the GFC or at the height of the pandemic. What was also interesting within the report was that higher income consumers are now being hit with “large declines in both their current personal finances as well as buying conditions for durables”, while low and middle income consumers saw improvements in the month. Inflation expectations were mixed with the 5-10yr rising one-tenth to 3.0% against 2.8% expected, while the 1yr fell two tenths to 5.0% to 5.0% against 5.1% expected (see University of Michigan for details). Separately reported Import Prices fell more than expected with ex petroleum -0.7% against -0.2% expected . Overall it suggests while softer than expected CPI/PPI/Import Prices give grounds to think inflation the peak of inflation is behind us, elevated inflation expectations highlight the risk that too high inflation is sustained and thus the fight of the Fed against inflation is still far from over.

Short-term yields reacted more to the long-run inflation expectations component out of the survey. The US 2yr yield after having drifted lower through the European season rose 7.3bps to finish up 1.8bps to 3.24%. Hawkish comments by the Fed’s Barkin who pushed back on any notion of a Fed pivot also added. Barkin stated he wanted to “…see a period of sustained inflation under control [clarified to be multiple months]. And “until we do that, I think we are going to just have to continue to move rates into restrictive territory”. Interestingly Barkin likely viewed the neutral rate as being higher, noting “there’s still more to come to get into restrictive territory ”. Barkin also pushed back on the notion of rate cuts once inflation was under control, noting: “you’d like to see inflation running at our target, which is 2% at the PCE, and I’d like to see it running at our target for a period of time”. (see Barkin CNBC interview for details). And added the experience from the 1970s was the Fed shouldn’t cut rates until inflation has convincingly returned to target.

Equities continued their relentless rise, brushing off the inflation expectations data and hawkish Fed rhetoric. Helping to drive sentiment was a report that Apple has asked suppliers to build at least as many of its next-generation iPhones this year as in 2021, with the inference that Apple expects earnings to still be ok even with a global slowdown and the possibility of a US recession. The S&P500 rose 1.7% and is now 16.7% off its mid-June lows, to be only -10.8% from its all-time high of early January 2022. The S&P500 now stands at 4,280 and not far off its 200-day moving average of 4,380. There has also been a clear tilt to growth stocks with the NASDAQ up 2.1% on Friday and in a technical ‘bull market’ given the index is now 22.6% above its low (though still 20.4% away from its November 2021 high). Ditto the Russell 2000 which was also up 2.1% on Friday and is also in a technical bull market. The rally has accompanied falls in volatility, with the VIX index closing the week just below 20 and at its lowest level since early April. It is not only equities that are bullish, so is Bitcoin which briefly surpassed $25,000 for the first time since mid-June on Sunday and gold which rose 0.8% on Friday to clear $1,800.

Investors clearly were underweight equities going into June and were surprised by a trio of events, including ok big tech earnings, Powell stating the Fed is at neutral, and signs of inflation peaking. Positioning might still be light (adding to the potential for a further squeeze higher in thin summer holiday trade), but on a macro view there are still signs of softness in the US economy. In contrast to Apple, US semiconductor companies warned on revenue on Monday and Tuesday. Meanwhile truckload spot rates are falling, a potential signal for falling goods demand (though that may be just symptomatic of a shift away from goods and towards services as has been widely foreshadowed and would also play to the view of inflationary pressures easing) and Citi ‘s credit card transactions data fell -1.1% in July. The WSJ reports lockdown darling Pelton has announced job cuts while also lifting the price of its products by 30%, while electronic retailer Best Buyers has cut its revenue forecasts. Financial conditions have also eased which is not what the Fed wants to see to put downward pressure on inflation and according to the Bloomberg Financial Conditions Index they are back to where they were in April.

Across the pond UK Q2 GDP was negative at -0.1% q/q (-0.2% expected). The data was largely ignored given the energy crisis has the BoE forecasting the UK economy to shrink for five consecutive quarters starting in Q4. There doesn’t seem to be any end to the energy crisis plaguing Europe, with low water levels also adding to supply chain problems. Elsewhere on the softer side China reported much weaker than expected aggregate financing data (756.1bn against 1350.0bn and 5170.0bn), highlighting that the softness seen in the economy is likely to continue in the near term. Given China’s zero-COVID policy and sporadic lockdowns in major cities, any stimulus attempts are unlikely to gain much traction. The property sector is also slowing, another headache for policy makers. Meanwhile geopolitical risks remain high with a US Congressional delegation having landed in Taiwan yesterday for a two day visit. The five member delegation arrived to “reaffirm the US support for Taiwan”.

In FX the USD gained against most pairs with the DXY +0.5%. Weakness was most acute in EUR (-0.6%), GBP (-0.7%) and USD/JPY (+0.5%). Bucking the trend was the AUD (-0.1%) and NZD (+0.1%), taking their lead from equities and highlighting their role as global risk proxies. Over the past week the theme has been of general USD weakness (DXY -0.8%), with the AUD and NZD standout performers. The AUD is now up 5.9% since its mid-July lows, ditto the NZD at +5.8%. Meanwhile the USD (DXY) has fallen -2.7% since mid-July. Commodities were mixed with WTI oil down -2.4% to $92.09, while gold rose 0.8% to $1,802.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.