NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

US Core CPI just 0.160% m/m and 3m annualised rate now 3.1%

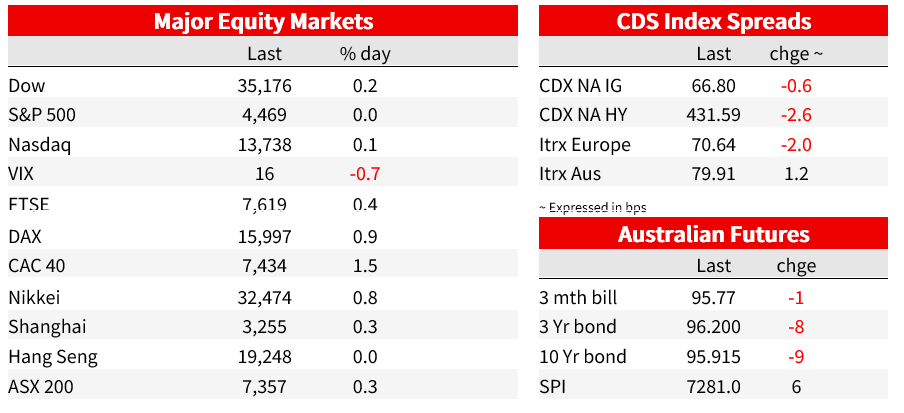

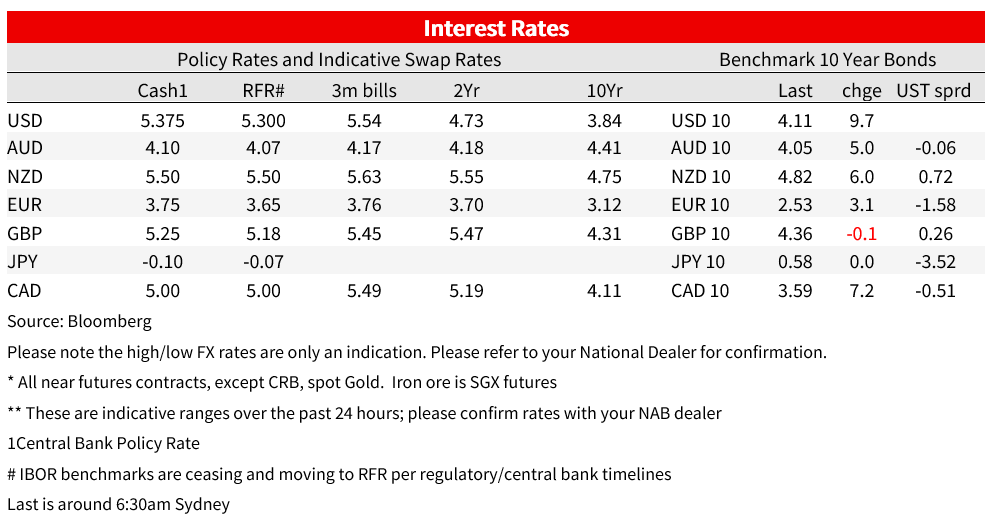

It was a night of two halves. A soft US CPI initially saw yields heading lower (Core CPI 0.160% m/m vs. 0.2% expected), before a tepid US 30yr treasury auction saw yields rise and the curves steepen (the 10yr yield is up 9.6bps to 4.10%); likely reflecting worries about absorbing the ramp up in long duration debt. Ditto the USD which initially weakened post-CPI, to more than reverse with DXY now up +0.1%. As for equities, the S&P500 was up 1.3% at one point, before paring back gains to close flat on the session.

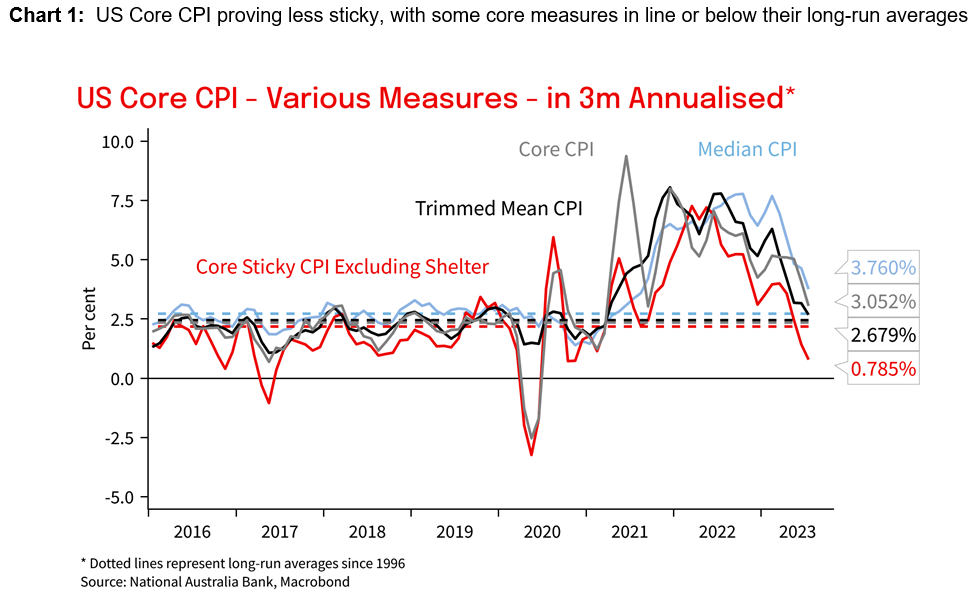

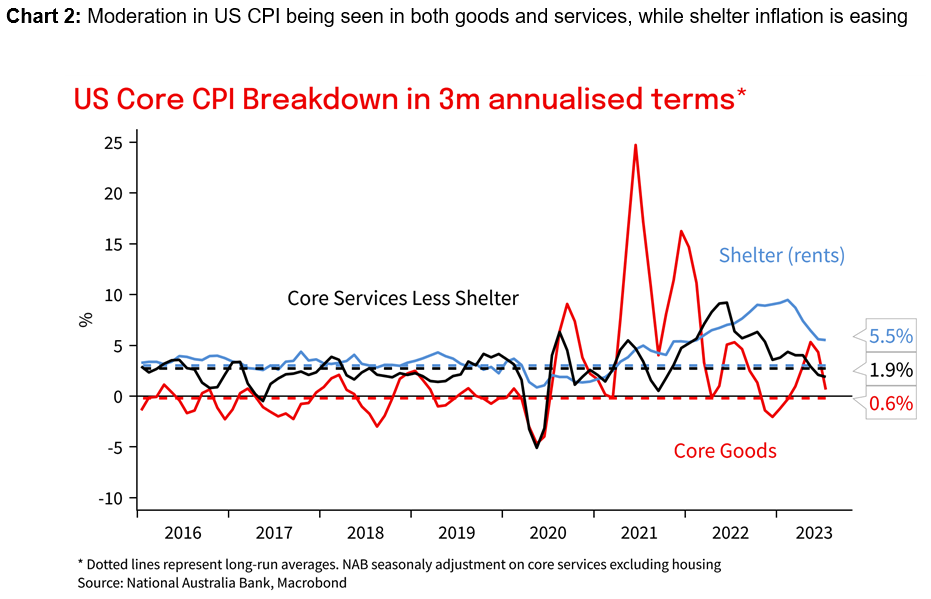

First to US CPI. Headline CPI was 0.2% m/m and 3.2% y/y (consensus 0.2/3.3). Core CPI was also 0.2% m/m and 4.7% y/y (consensus 0.2/4.7). While both measures were close to consensus, the details were more flattering. Core CPI in unrounded terms was just 0.160% m/m, following last month’s 0.158%. In 3-month annualised core CPI is now running at 3.1%. Alternative core measures have seen similar moderation in 3-month annualised with the Cleveland Fed’s Trimmed Mean at 2.7%, though the Weighted Median is a little higher at 3.8%. Highlighting that inflation may not be as sticky as feared the Atlanta Fed’s Core Sticky Excluding Shelter is now running at just 0.8% in 3-month annualised. Our measure of core services excluding shelter is running at 1.9% 3-month annualised, core goods at 0.6%, with only shelter running higher at 5.5%. Core goods is interesting and suggests signs of healing supply chains and weak global manufacturing at last being reflected in end prices. Meanwhile in other economic news, US initial jobless claims rose a chunky 21k last week to 248k (230k consensus), but still consistent with a flat trend over the past five months.

The data should reinforce the widely held view that the Fed could skip a hike at the next meeting in September, but also keeps alive the possibility of a further possible hike later in the year given the tightness in the labour market. A view also reflected by the WSJ’s Fed Whisperer Timiraos (see WSJ: Cooler July Inflation Opens Door to Fed Pause on Rates). The Fed’s Daly (non-voter this year) said the result was “largely as expected and that is good news” and that “ It’s also consistent with what we believe will be happening, which is that inflation will gradually make its way down…But it is not a data point that says victory is ours. There’s still more work to do.” Given core services in the CPI, this comment though did seem dated “we do need to see [core services] come back to pre-pandemic levels if we’re going to be confident that we can get to 2% on a sustainable basis”. Safe to say if core CPI repeats the same performance as the past two months, Fed rhetoric will start to look dated (see Fed’s Daily: Yahoo Finance Interview for details). Markets price a cumulative 8bps of hikes through to the November meeting, a basis point lower from yesterday.

The knee jerk reaction to the CPI report was lower rates, but that quickly faded before focus turned to increased Treasury supply. The $23b auction of 30-year bonds was awarded at more than 1bp higher than the when-issued yield, the amount allotted to primary dealers was the largest since February, signs of tepid demand at this long duration auction. Rates jumped higher across the board after the announcement and even though the 30yr auction was sold at a yield of 4.189%, afterwards the 30yr yield jumped as high as 4.26% in late trade. Summer holiday trade may also be a factor. The curve steepened with the 2yr yield up 3.4bps to 4.84% and the 10yr yield up a sharper 9.6bps to 4.10%. The 2/10s curve is steeper on the day at -74.7bps. The moves were fully reflected in TIPs with the 10yr real yield up 8.8bps to 1.76%.

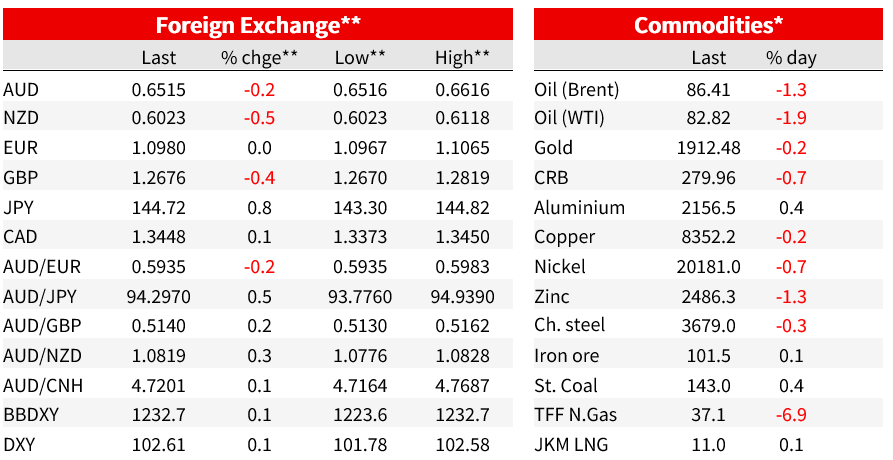

In FX, initial USD weakness of -0.7% post CPI has been fully reversed with DXY now +0.1%. The AUD currently trades at 0.6517, down 0.2% on the past 24 hours, after having spiked as high as 0.6616 on the initial USD weakness. Not helping the AUD is the mood around China. The China Securities Regulatory Commission plans to convene a meeting with some property developers and financial institutions later today. This follows one major developer, Country Garden Holdings, missing a coupon payment earlier this week and who isn’t invited to the meeting, suggesting some plan to prevent a default for the company and contain contagion risk across the sector. As for other major pairs, the yen has been the weakest, with USD/JPY +0.8% on the day to 144.76. Other pairs mostly reflecting mild USD strength: EUR +0.0% to 1.0979 and GBP -0.4% to 1.2674.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.