Total spending grew 0.9% in June.

Composite PMI sub-50 everywhere in the world bar UK; US worst of all.

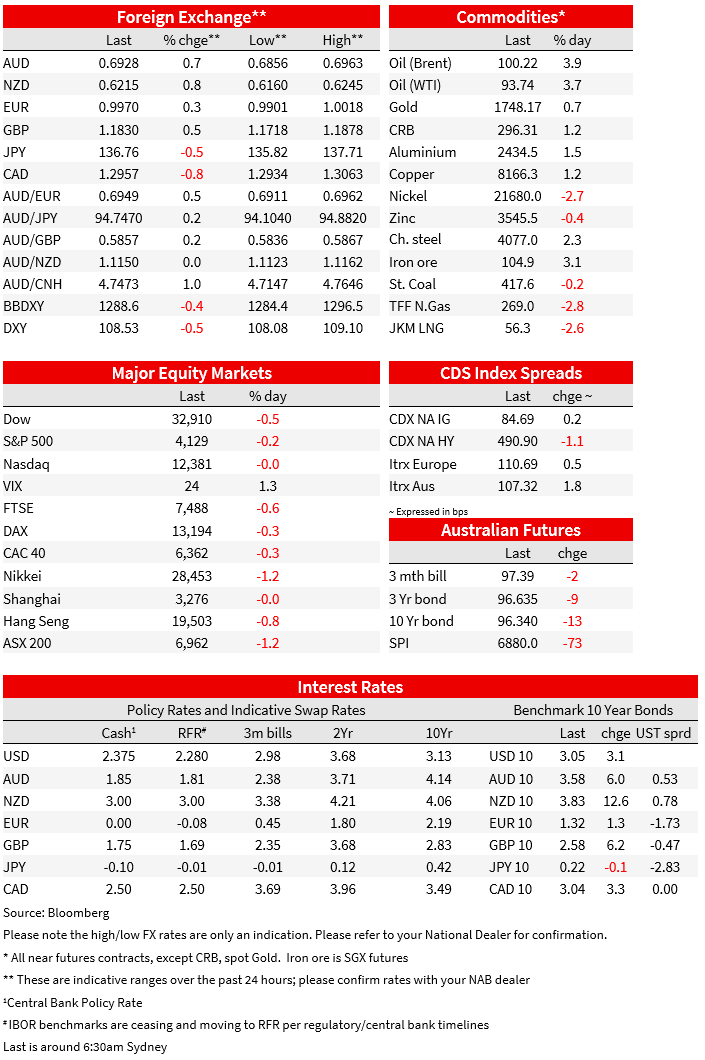

In the FX world that this scribe inhabits, relativities are what matters when it comes to currencies. In the case of all the data released in the last 24 hours, that for the United States happens to be worse than just about everything everywhere (not something we are used to saying). The US dollar has accordingly given back a little of the strong gains posted since the middle of last week, helping AUD trade back more comfortably onto a 0.69 handle, the US yield curve has shown some further re-steepening tendencies with 2s down and 10s up, while US equities have just closed with small losses for the S&P500 and no change in the NASDAQ. Brent crude is back above $100 for the first time in over a week.

The last 24 hours has seen ‘flash’ PMIs released for Australia, Japan, France, Germany, pan- Eurozone and the United States – 21 numbers in all of you count Manufacturing, Services and Composite readings. While there are some ‘overs and under in individual releases relative to expectations, the standout feature is that Composite readings for every country bar the UK have come in below 50, on a literal read implying outright economic contraction.

Before we rush to conclude that the UK – the one economy where recession is supposedly nailed on and its central bank willing to admit as such – is now holding up the global economy, the latest Confederation of British Industry (CBI) survey published overnight (the equivalent of the NAB Business Survey) shows Orders slumping to -7 from +8 and its Selling Prices gauge leap from 48 to 57. It really is just a matter of time before the hard data reflects the reality of the brutal energy price rises confronting UK households, unless the new British prime minister to be announced next weekend can somehow wave a magic wand (spoiler alert – she (for it will be she) can’t).

While the Eurozone PMIs numbers were somewhat mixed relative to expectations, albeit down on July in all respects, the most market-moving ones of the night were for the United States, where the Serives reading slumped to 44.1 from 47.3 against an expected rise to 49.8 (the latter because of the bum steer the weak reading in July provided vis-à-vis the subsequent much more highly regarded ISM survey). The US manufacturing reading also fell, but only to 51.3 from 52.2, just a little weaker than expected.

Compounding the ‘relatively worse’ US data night, New Home Sales in July slumped by 12.6%, well below the -2.1% and following a 7.1% (revised) June read, and the Richmond Fed manufacturing index fell to -8 from zero against an expected fall to -2. This makes it ‘2 from 3’ for the regional PMIs released so far (Empire and Richmond down, Philly Fed up).

In markets, we can date the fall-back in the USD to the Services PMI print, DXY falling from around 109.0 pre-release to below 108.20 before pulling up to around 108.50 later in the day and where it ends in New York. The USD sell off saw AUD/USD rise from around 0.6880 to be briefly above 0.6960, before easing to around 0.6930 as of NY close. All other G10 currencies were lifted against the greenback, NOK faring best on the oil price jump, CAD and NZD showing a similar sized rise as AUD (all up 0.8%) and higher) and GBP (+0.6%) doing somewhat better than the EUR (0.3%). The oil price rise in turn, that saw WTI and Brent crudes lift by $3.25-$3.50 and Brent back above $100 for the fist time since 12 August, is attributed to further reflection on the comments from Saudi Arabia earlier this week that prices don’t reflect fundamentals and that OPEC+ output curbs might become a consideration.

In the rates market we’ve seen a big range in 10-year Treasuries, from 2.98% (seen soon after the PMI data) to 3.07% (beforehand) before settling in late New York trade back at 3.05%. 2s are -1bps, meaning that the 2/10s curve has steepened by 4bps on the day to -25bps.

Finally, the one piece of central bank speak that caught the eye was from ECB GC member Panetta, who said not just that the probability off a recession ids increasing, but that recession would mitigate inflationary pressures. There speaks some truth.

NAB Markets Research Disclaimer

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.