We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Following a negative lead from Asia, US and EU equities have begun the new week on the back foot.

AU: Retail sales (m/m%), Jul: 1.3 vs. 0.3 exp.

Following a negative lead from Asia, US and EU equities have begun the new week on the back foot. Meanwhile, after moving higher during our time zone yesterday, UST yields have range traded overnight with the 10y Note now trading around 3.11%. The USD is little changed with euro gains offset by JPY and GBP weakness. EU gas prices fall 20% after EU Commission says is considering regulating its energy market.

Friday’s post-Powell market trends in equities have extended at the start of the new week with Asian (Nikkei down 2.66%, CSI 300 -0.44%) as well as European (Euro Stoxx 600 -0.81%) and US equity markets starting the new week with negative returns . Overnight the S&P 500 traded mostly in negative territory, falling as much as 1% early in the session, showing a modest recovery before the close and ending the day down by 0.67%. The NASDAQ closed 1.02% lower.

It seems investors are still digesting the consequences from Fed Chair Powell hawkish speech where he not only refuted the notion of a dovish pivot but emphasised the need for rates to head higher and remain restrictive in order to bring inflation to heel. Yesterday during our APAC session, UST yields rose across the curve and then settled into a range trading environment during the overnight session. 10y UST yields are 7bps higher relative to Friday’s close and are currently trading at 3.108% while th2 2y rate is 2.5bps higher at 3.42%. The 2y10y curve steepened 4bps to -32bps.

Last week expectations Fed Chair Powell will be delivering a hawkish message, lifted US rate hike expectations with the moves extending after his speech on Friday and now extending further at the start of the new week . A September hike is now priced at 69.3bps, up almost 3bps from Friday while next year the peak in the Fed Funds rate is seen at 3.84, up 5bps. A lower funds rate is still seen by December next year, at 3.499%, 4bps higher relative to Friday’s levels.

The other important theme from Jackson Hole was the hawkish rhetoric coming from ECB speakers. Speaking overnight ECB Chief Economist Lane, considered one of the most dovish on the committee, also called for higher rates, but arguably at a less aggressive pace than the likes of ECB Schnabel, who over the weekend urged “strong determination to bring inflation back to target quickly.”. Instead, Lane called for “A steady pace, that is neither too slow nor too fast, in closing the gap to the terminal rate”. The speech outlined the importance of determining the expected terminal rate, the current gap and then assessing the speed at which to approach the terminal rate based on new information. This argued for a “meeting-by-meeting approach.” The speech seemed to infer he was on board for a 50bps hike next month, but unlikely 75bps.

Higher European yields versus US rates have lent some support to the euro overnight but a big decline in the gas TTF benchmark, which fell almost 20% on Monday was also helpful, although at EUR272/Mwh, gas prices are still unbearably high. The move lower in gas prices was triggered after EU Commission President Ursula von der Leyen said the EU was looking at urgent action to try to dampen soaring power prices and is putting together proposals to reform the electricity market. Price cap are seemingly part of the discussion and the Czech Republic, which holds the rotating presidency of the EU, announced an extraordinary meeting of energy ministers to be convened on September 9. On the topic, Shell’s Chief Executive warned that Europe may need to ration access to energy for several years as the crisis is expected to last more than one winter.

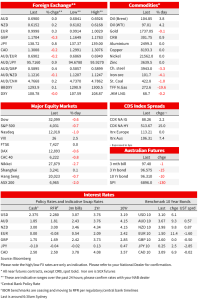

The USD is little changed in index terms. After almost trading below 0.99, the euro is now playing with a move above parity currently trading at 0.9997. The NOK and CAD are also a tad stronger, up between 0.10 and 20% with the move up in oil prices helping their cause. WTI and Brent oil are up close to 4% following comment from Iran suggesting a imminent Nuclear deal (allowing Iran to increase oil sales) looks unlikely with talks with the US likely to extend into September. After underperforming on Friday, NZD has recovered a little bit, up 0.3% to 0.6153 while the AUD is little changed at 0.6903, although yesterday the big decline in US equity futures dragged the AUD down to an intraday low of 0.6841. In contrast GBP (-0.52% to 1.1709) and JPY (- 0.9% to 138.72) are the notable underperformers, the former saddle by political uncertainty in addition to higher energy prices while the latter has been weakened by higher UST yields.

NAB Markets Research Disclaimer

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.