On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Epicentre of current market turmoil shifts across the Atlantic to UK on Friday

Data round up:

S&P Global EZ Manufacturing PMI 48.5 from 49.6 and 48.8 expected

S&P Global EZ Services PMI 48.9 from 49.8 and 49.1 expected

S&P Global EZ Composite PMI 48.2 from 48.9 and 48.2 expected

S&P Global UK Manufacturing PMI 48.5 from 47.3 and 47.5 expected

S&P Global UK Services PMI 49.2 from 50.9 and 50.0 expected

S&P Global UK Composite PMI 48.4 from 49.6 and 49.0 expected

S&P Global US Manufacturing PMI 51.8 from 51.5 and 51.0 expected

S&P Global US Services PMI 49.2 from 43.7 and 45.5 expected

S&P Global US Composite PMI 49.3 from 44.6 and 46.1 expected

Canada July Retail Sales -2.5%m/m versus -2.0% expected

Canada July Retail sales ex Auto -3.1% versus -1.0% expected

After the market volatility in the first four days of last week generated by multiple central bank policy decisions, plus foreign exchange intervention by the Bank of Japan for the first time 1998, it was the turn of the UK to crank up the volatility dial on Friday. Whether or not the UK government announcement of the biggest tax reduction since 1972 – including removal of the top 45% rate of income tax down to 40%, large-scale fiscal support for households and business to protect them from sky-high energy prices and various reduction in ‘red tape’ – will in time yield a significant growth dividend is not something markets are yet willing to contemplate. Instead, they were consumed by worries over the scale of near-term UK government financing needs, at a time when the current account deficit is running at more than 8% of GDP.

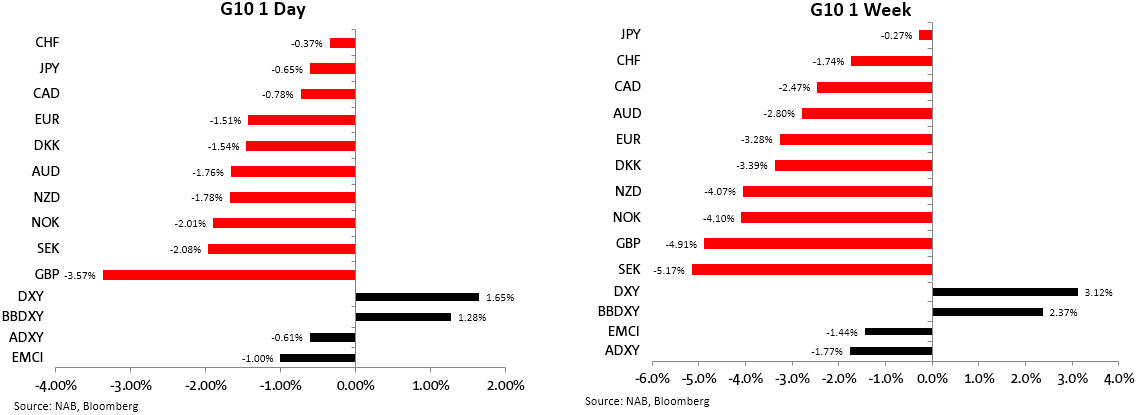

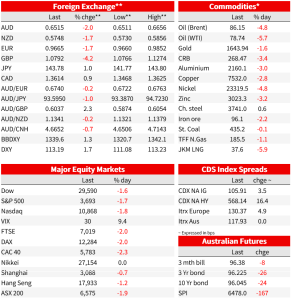

GBP/USD lost a cool 3.6% on Friday for a 4.9% weekly loss and to new post-1985 low of $1.0840. It’s already being quoted sub-1.08 in early Sydney trade. The record low is $1.0520 recorded in March 1985, a level some traders will no doubt now have their sights set on. AUD/GBP punched above 0.60 or the first time since October 2017. And following the announcement that the estimated additional £62bn of funding needed in the coming year (to a total of £193.9bn) would be concentrated at the shorter end of the gilts market, 2-year gilt yields jumped by 63bps to 3.8%. Contributing to the rise was the money market pricing in the need for an even more aggressive BoE tightening cycle, pushing mid-2023 pricing for Bank Rate up, from 4.9% following Thursday’s 50-point BoE rate hike to 5.5%.

Chatter about a possible UK sovereign rating downgrade has already begun. The three main ratings agencies all have the UK on ‘stable’ ratings footings at present at AA (S&P), AA3 (Moodys) and AA- (Fitch) such that even if one or more does decide to put the UK on negative ratings watch, any decision to downgrade will likely not be before the evidence, or otherwise, of a growth dividend from Friday’s announcements, eventuates. A 2023, not 2022 story.

Elsewhere in the FX market on Friday, broad based USD strength was the order of the day, the DXY index rising by 1.7% (3.1% on the week to a new post-June 2022 high). This encompassed EUR/USD falling to a post-September 2002 low of 0.9668, AUD/USD making a low of 0.6511 (weakest since 20 May 2020) and NZD/USD 0.5730 (weakest since 24 March 2020).

Incoming economic data was very much a sideshow Friday, the main event here being the various ‘flash’ PMIs. In the Eurozone, it was again a case of French services holding the fort, its PMI rising to 53.0 from 51.2 against sub-50 (and mostly lower) readings for French and German manufacturing, German services and for both pan-Eurozone readings (EZ Composite down to 48.2 from 48.9, virtually the same as the UK, to 48.4 from 48.9). The US equivalent numbers, much less regarded than the longer established ISMs, fared much less badly, manufacturing up to 51.8 from 51.5 and services lifting to 49.2 from 43.7. Chances are the forthcoming US ISM’s will show the US economy continuing to fare significantly better than Europe (or China for that matter, where we’ll get new readings on Friday).

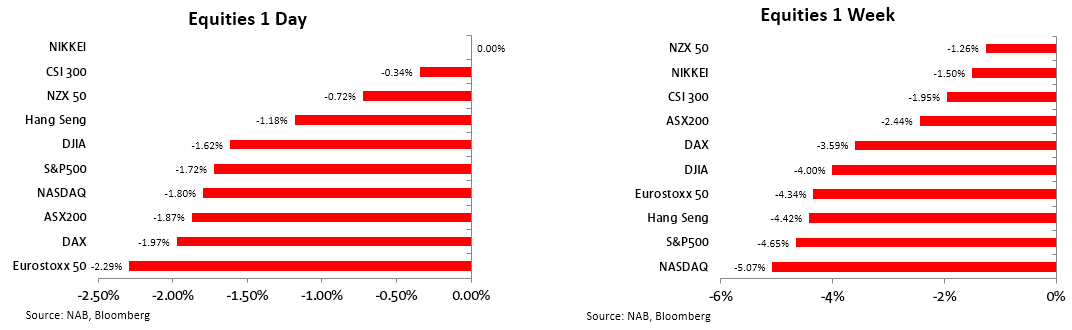

Equity markets everywhere in the word fell on Friday to round out an across-the-board down week. Not even the boost to UK exporter earnings from the crunch lower in Sterling could spare the FTSE 100 from a 2% loss, though this was a little less than the 2.3% fall in the Eurostoxx 50. On the week, it is the more rate-sensitive NASDAQ that fared the worse, down 5.1%, followed globally by the S&P500, down 4.7%. Incidentally, the Weekend Financial Times’ lead story is titled ‘Investors pile into insurance against further market sell-offs’ It notes the purchases of put options on stocks and exchange traded funds have surged, with money managers spending $34.3bn on the options in the four weeks to September 23, according to Options Clearing Corp data analysed by Sundial Capital Research. The total was the largest on record in data going back to 2009, and four times the average since the start of 2020. Institutional investors have spent $9.6bn in the past week alone.

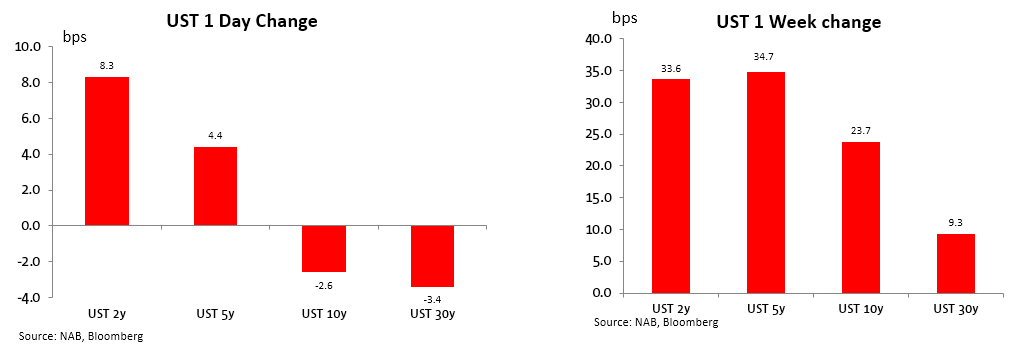

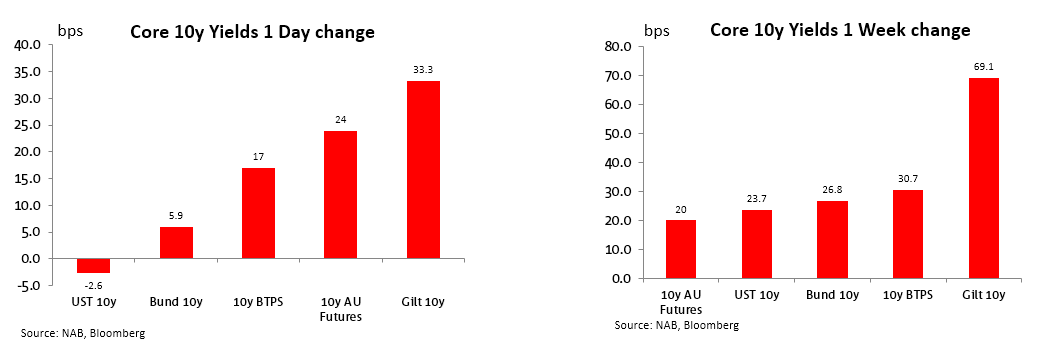

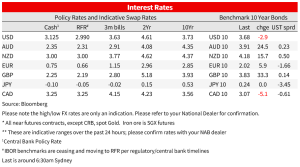

For bond markets, it was the belly of the US yield curve that suffered the most last week, the 5-year note adding 35bps and where one contributory factor – and to the 24bps rise in the 10-year yield – was the Bank of Japan’s intervention on Thursday. This is on the view that if not yet, they will need to be sellers of some of their stock of FX reserves Treasury holdings to furnish the USDs needed to sustain an intervention effort. Gilt yields meanwhile comfortably surpassed the back up in Treasury and all other global developed market bond market yields, the 10-year yield up 69bps on the week. Aussie 10s, in futures terms, added 20bps on the week, so meaning 4bps of spread compression versus equivalent US Treasuries.

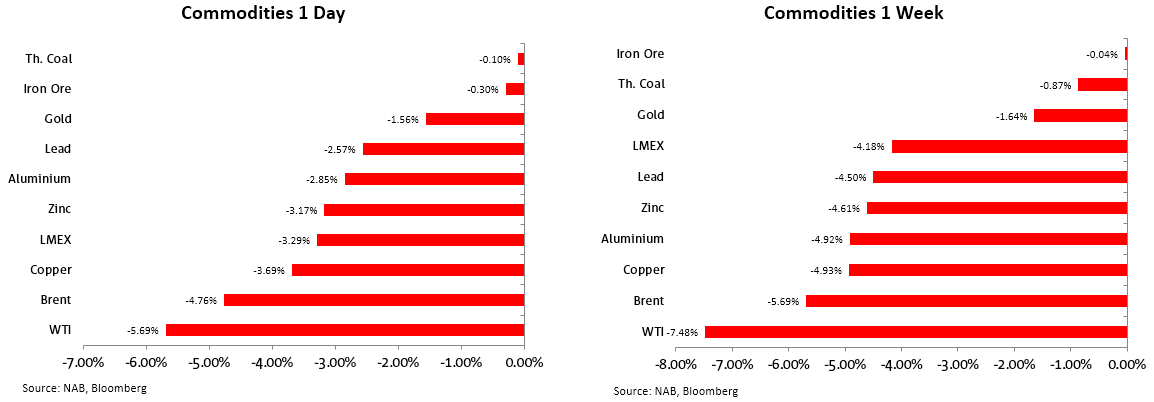

Finally, in commodities, with global growth concerns to the fore as central banks crank up the policy tightening dials and with the US dollar rampant, no single commodity we track managed an ‘up’ week, though of note for Australia, iron ore and coal were only very slightly down. Oil was pummelled as perhaps the best barometer of anticipated demand destruction alongside USD strength, WTI crude losing 5.7% on Friday alone for a loss of 7.5% on the week.

NAB Markets Research Disclaimer

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.