Investing and risk management in a world of shifting and unstable cross-asset correlations

Insight

UK markets remain at the epicentre of global market volatility

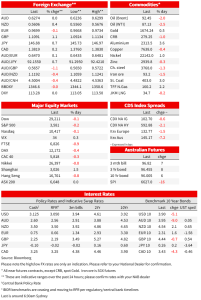

Ahad of the all-important US CPI release tonight, UK markets remain at the epicentre of global market volatility, in bonds and currencies if not necessarily stocks, US equities ending the NY day little changed at the start of the US Q3 earnings season, after a mostly down day for European stocks (UK FTSE -0.9%, Eurostoxx 0 -0.25%). AUD/USD is virtually unchanged on 24 hours ago, but AUD/NZD has lost another 0.4% to be, at one point in the night, some 4% down from its recent high near 1.15.

Volatility in UK markets – gilts and Sterling, remains exceptional. Following BoE Governor Bailey’s strong words on Tuesday evening that the UK pension industry had three days to get its house in order ahead of an (unchanged) Friday deadline for the ending of the Old Lady’s gilt buying spree, the FT reported late in our day Wednesday that the Bank had privately told some institutions that if necessary, buying would continue into next week if market dysfunction demanded – which the BoE denied on Thursday morning as being the case. The reality is inevitably that the (any) central bank’s financial stability responsibility’s will ultimately override their broader (anti-inflation) macro-economic mandate, such that the Bank will necessarily be there if market conditions demand (not that, in this case, it means the Bank would stand ready to keep a cap on gilt yields, far from it in fact in so far as this directly conflicts with its anti-inflation objectives).

Into the market volatility mix, our UK colleagues note various seemingly well sourced media reports leaning into the likely coming further U-turns on fiscal policy by the Truss govt – commensurate with the events on financial markets and the deterioration in the UK’s standing given the barely fathomable policy decisions of the last few weeks. This includes speculation on pushing back the 1p cut in the basic rate tax (to 19p) back to its original 2024 date – but retaining the (now aspirational) narrative of wanting to cut taxes. There is talk also of pushing back on the plans to not raise corporation tax – with suggestions some tax rises will take place, but they will be staggered. Collectively the UK media is saying the sheer turmoil in markets, the rises in interest rates and the need to show fiscal prudence are finally being heeded. Further, Treasury staffers are reportedly going through the entire mini (maxi?) Budget to see what can be unpicked, that everything is being looked at and that “the PM is panicking” according to one quoted Whitehall official.

The upshot (for now) of all this is that 30-year gilt yields rose from Tuesday’s closing level of 4.80% to as high s 5.10% (versus their 28 Sep peak of 5.14%) before retracing all the way down to 4.78%. Helping the latter move was news that BoE had bought £4.4bn of gilts from investors, its biggest intervention since it entered the market last month to prevent “fire sales” by UK pension funds in the wake of government announced plans for tax cuts to be funded by government debt issuance.

Elsewhere in bond land, Treasury yields are 2-4bps lower on the day (see FOMC Minutes comment below) in line with falls seen in most European markets and which followed the retracement lower in gilt yields.

For currencies, GBP has remained extremely volatile , GBP/USD has fallen sharply in late NY/early Wellington trade Wednesday on BoE’s Bailey ‘three days left’ remarks and extended those losses to $1.092 during the APAC day before rallying to a high as 1.1145 in the last few hours – a 2% intra-day range. Currency moves elsewhere have been much more modest, though of note USD/JPY has shown no signs of pulling back after yesterday’s run-up to within a whisker of ¥145, so just above the highs it reached on 22 Sep in front of the BoJ intervention. Of note here have been comments from BoJ Governor Kuroda in Washington, re-iterating the BoJ’s ongoing support for its ultra-easy monetary policy and, while saying government FX intervention was quite appropriate, noted that yen depreciation to date may have had a ‘good macro impact’.

Just released FOMC Minutes from the Fed’s September meeting (when rates were raised by 75bps) look to be responsible for a small pull back in US treasury yields and the USD. While the Minutes indicates united and resolute commitment by policy makers in their pledge to fight inflation, and a view that the cost of doing too little (on policy rates) outweigh that of doing too much, there was (at this stage only a minority) view stressing the importance of calibrating tightening to mitigate risks both to the economy and financial stability. Nothing here to detract from the view 75bp from the Fed next month is nailed on (74bps priced), but also nothing to suggest that current market pricing favouring a step down to 50bps in December is off-base.

Data wise, monthly UK GDP data showed a 0.3% m/m contraction in August, making the UK on track to record a negative Q3 outcome, likely the beginning of a well-anticipated economic recession. In other key economic news, US PPI inflation offered little respite from the strong inflation narrative, with the headline rate stronger than expected at 0.4% m/m and 8.5% yoy, boosted by higher food prices, while core inflation was broadly in line at 0.3% m/m and 7.2% y/y.

Finally, ahead of a slew of bank results today and tomorrow, the US earnings season kicked off with a strong result from PepsiCo and an upgraded outlook. The strong result reflected price increases put through that exceeded costs and this more than offsetting weaker volumes – not good for those worried about “stagflation” but good for PepsiCo if it has pricing power.

NAB Markets Research Disclaimer

Investing and risk management in a world of shifting and unstable cross-asset correlations

Insight

Robust growth for online retail sales observed in June

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.