NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The UK has a new PM in Rishi Sunak, and gilts have rallied in response. UK 10yr gilt yields were 31bp lower at 3.75%. That’s 90bp off their peak of 4.64%, but still about 60bp above their level before the Truss Premiership.

The UK has a new PM in Rishi Sunak, and gilts have rallied in response. In the US, equity markets extended Friday’s gain, the S&P500 up another 1.2% as markets look ahead to a busy week for earnings. Chinese equities are lower, led by tech, in reaction to the outcomes of the Party Congress and what it means for COVID-zero and broader policy as the onshore yuan hit a 14-year high.

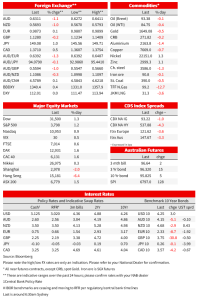

First to the UK, where exits from Boris Johnson and Penny Mordaunt have cleared the way for Rishi Sunak to become PM. UK 10yr gilt yields were 31bp lower at 3.75%. That’s 90bp off their peak of 4.64%, but still about 60bp above their level before the Truss Premiership. 2yr yields were off an even sharper 37bp at 3.43%, more than 100bp off their recent highs and around 28bp higher than pre-Truss as further firming of a changed fiscal backdrop has pared expectations OF the task at hand for the BoE. Reports suggest Treasury is still working under the assumption the medium-term debt-cutting plan will be presented to parliament on October 31. Moves elsewhere in rates markets were relatively muted. The US 2yr and 10yr were each 3bps higher to 4.51% and 4.24%. German 10yr bund yields were 9bp lower at 2.33%.

European flash PMIs slid deeper into contraction territory. The Eurozone composite slowed to 47.1 from 48.1 and 47.6 expected, dragged down by manufacturing, which fell sharply to 46.6 from 48.4. But services fared little better, slipping to 48.2 from 48.8. There is little in the way of country breakdown in the flash numbers, but German numbers made especially grim reading. The composite falling to 44.1 and S&P Global citing energy costs and weaker demand as drivers of a quickening manufacturing downturn. In contrast, France’s composite PMI pointed to mere stagnation, slowing from 51.2 to 50. Forward looking components of the survey pointed to more slowing to come. One positive note was companies reporting fewer component shortages and improved shipping, though S&P notes much of this was due to slowing demand as much as increase capacity. The UK numbers also fell deeper into contraction. The composite falling to 47.2 from 49.1 and 48 expected. The US PMI also surprised lower at 47.3 from 49.2 with a sharp drop in the Services PMI from 49.3 to 46.6. The more closely watched US ISM data is next week.

In China, the conclusion of the National People’s Congress over the weekend brought no sign of movement on the COVID-zero policy and not only confirmed a widely expected third term for president Xi but installed loyalists throughout the Party’s top ranks. The reaction in markets has been less than positive. The Hang Seng was 6.4% lower in its worst day since the GFC. The Hang Seng China Enterprises Index, a gauge of Chinese stocks listed in Hong Kong, was down more than 7% and the CSI 300 was off nearly 3%. Bloomberg reports foreign investors sold a record amount of equities via trading links in Hong Kong in data going back to 2016. Tech giants were under additional pressure amid fears of less market-friendly policy. Alibaba, Tencent and Meituan were each down more than 11%. The onshore yuan hit a fresh 14 year low against the USD at 0.7263, while the dollar gained 1.3% against the CNH to 7.3202 after hitting a high of 7.3322

All of this despite GDP data defying fears a weak number might have contributed to the delayed release. GDP came in at 3.9% y/y vs 3.3% y/y expected. The full gamut of data released, however, showed the ongoing drag from covid controls on the consumer economy. Industrial production for September rose 6.3% y/y (4.8% expected). Retail Sales, though slowed to 2.5% y/y from 5.4% and 3.0% expected. Reports yesterday evening that China suspended in-person schooling and dining-in at restaurants in a district at the centre of Guangzhou will do nothing to allay fears of an ongoing gloomy consumer outlook. The Party Congress outcomes suggest little chance of a near term change in policy. As one example, Shanghai Party Secretary Li Qiang was promoted to Politburo Standing Committee and looks poised to become the next premier despite the hit to Q2 economic growth.

In currency markets, the DXY was little changed after Friday’s broad-based pull back, down 0.1%. The AUD and NZD were the worst performing of the G10 currencies, the weaker renminbi and China-centric sell-off one contributor. The AUD was 1.1% lower to 0.6311. The dollar gained 1.0% against the yen to be back up around 149, paring much of the 1.4% fall on Friday on the back of reported intervention. A sharp but short-lived intraday rally in the yen on Monday bred speculation the MoF was in the market again. Bloomberg estimates the size of Friday’s suspected intervention was as much as 5.5 trillion yen ($36.8 billion).

Across equity markets China was very much the exception to what is elsewhere a sea of green. The Euro Stoxx 50 was 1.5% higher, helped by the tailwind of strong gains in US equities on Friday despite soft PMI readings. The S&P500 extended Friday’s gains, up 1.2% and led by health and consumer staples. The NASDAQ was 0.9% higher. There is a slew of earnings reports ahead later this week, Apple, Amazon, Alphabet and Microsoft among them.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.