We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Yields lower on Friday, but still close to recent cycle highs

Happy seven year anniversary to our Morning Call Podcast. A Sonny & Cher song to start the week and which incidentally was also used repeatedly as Phil Connors’ wake-up music in the 1993 movie Groundhog Day. If you are having déjà vu with weekend headlines of China attempting to boost lending and activity without providing detail, you’re not alone. Markets will likely want more details though. The other piece of weekend news worth contemplating ahead of Jackson Hole later in the week is a WSJ article by Fed Whisperer Timiraos – Why the Era of Historically Low Interest Rates Could Be Over – more on that below.

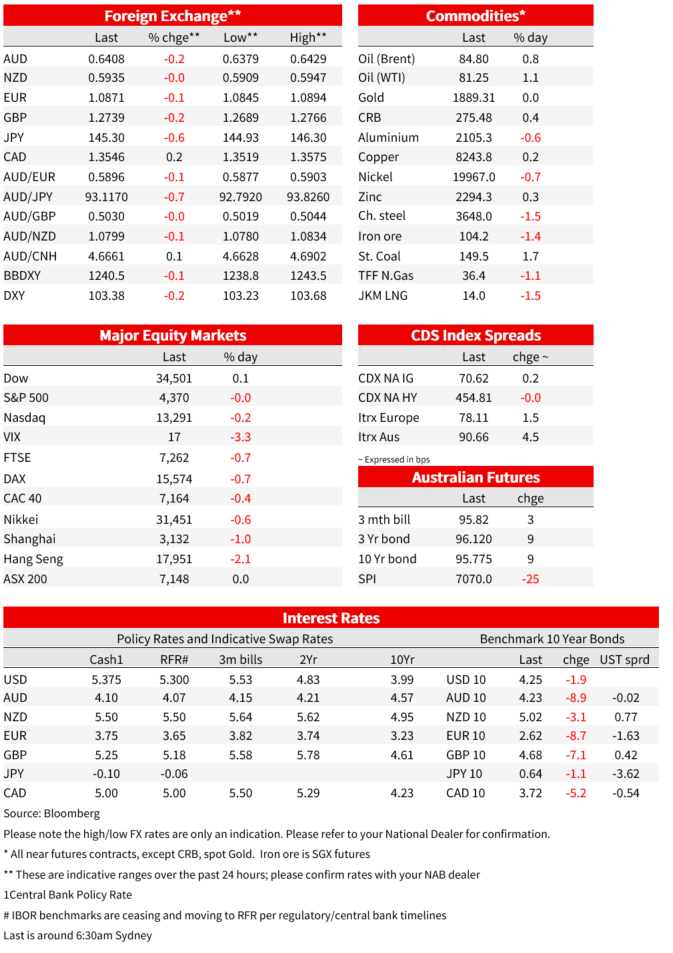

As for Friday’s moves, it was relatively subdued with the US 10yr -1.9bps to 4.25%. Note the 10yr did reach a peak of 4.34% during the past week which equalled the multi-years highs reached in October 2022. Over the week the US 10yr yield has risen by 10.2bps, which has been more than fully reflected in real yields with the 10yr TIP yield up some 16bps to 1.94% (the implied inflation breakeven fell by around 6bps to 2.31%). Near-term Fed Funds pricing is little changed with around 9bps of tightening expected by November, but cuts thereafter, though there has been a reduction in the degree of cuts priced for 2024 – there is currently 114bps worth of cuts priced by the end of 2024, down from 129bps last week.

Equities were broadly flat with the S&P500 -0.0% on Friday, though over the week the S&P500 is down some 2.1% on the week. Even with the recent declines the S&P500 is still up 22.2% since its low of 2022, and is 8.8% away from its record high. Nvidia’s earnings on Wednesday will be a key marker for equities, as will Fed Chair Powell’s Jackson Hole speech. FX markets were relatively quiet on Friday, the USD (DXY) was -0.2%, consolidating after the nearly 4% gains from the recent lows in July. Major pairs were little changed with EUR -0.1%, GBP -0.2%, though the Yen did outperform with USD/JPY -0.6% to 145.30. The AUD was -0.2% on Friday to 0.6408, though is -1.3% on the week.

First to the China news on the weekend. It was reported by Bloomberg that the PBoC and financial regulators met with bank executives and told lenders again to boost loans to support a recovery, adding to signs of heightened concern from policymakers about the deteriorating economic outlook. Authorities also urged for adjustments and an optimization of policies for home mortgages at the meeting on Friday, according to a statement from the PBoC on Sunday. Executives from China Life Insurance Co. and stock exchanges were at the same meeting, where officials also discussed measures with the financial sector to prevent and reduce local government debt risks (see Bloomberg: China Urges More Loans, Debt Risk Reduction as Woes Compound). Despite pledges to expand consumption and reform the property sector, officials have so far resisted major stimulus.

Ahead of Jackson Hole, which this year’s theme is “Structural Shifts in the Global Economy”, there was an interesting piece by the WSJ’s Fed Whisperer Timiraos on Why the Era of Historically Low Interest Rates Could Be Over – WSJ . It is hypothesised that large government deficits and investment needed for the clean energy transition may have lifted the neutral rate, with one estimate pegging the real neutral rate at 1.5%. With the Atlanta Fed’s GDP Now estimate running at 5.8% annualised even as inflation appears to be slowing, productivity may also be starting to lift. The main implication here is that a higher neutral rate if realised, would mean rates settling higher than they were prior to the pandemic.

As for data on Friday, UK Core Retail Sales fell by more than expected at -1.4% m/m vs. -0.7% consensus and coming after the prior month’s +0.7%. It is unclear what to make of the extent of the weakness, though at face value it may suggest households are being impacted by higher prices and from higher rates with the level of volumes now 1.8% lower than pre-pandemic February 2020 levels. The wet weather could also have been a factor with July being the wettest July since 2009 and the sixth wettest July on record since 1836. One interesting snippet for shopping centre landlords was that the wet weather saw online retail making up 27.4% of total sales, up from 26% in June and the highest share since February 2022. People are not returning to pre-pandemic bricks and mortar shopping in the UK at least. UK yields fell in the wake of the data with 10yr GILTs -7bps to 4.67%. BoE pricing though remains elevated with still 31.5bps priced for September and a a cumulative 76bps by February, albeit down from 89bps by March the prior week.

Finally in Japan, Core CPI was as expected at 4.3% from 4.2%. The interest part though was service inflation which rose to 2% from 1.6% in June, and barring the impact of a 1997 sales tax hike, service inflation had remained below 2% since 1993. The BoJ though is likely to be measured in public and is really wanting to see wages growth lift, though the inflation data suggests it is just a matter of time before the BoJ will have to tweak policy again. JGBs yields were marginally lower across the curve with benchmark 10-year bonds down 2bp to 0.62%. It is also worth noting some analysis about whether bond valuation losses from higher rates would impact Japanese regional banks. The central bank said in its Financial System Report issued in April that if yields rose by 1 percentage point across the board, regional banks in aggregate would suffer ¥3.4 trillion, equivalent to about $23 billion, in unrealized losses on their domestic bondholdings (see WSJ: As Rates Rise, Japan Is Wary About Silicon Valley Bank Sequel).

Coming this week:

Coming up today:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.