We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

In a low trading environment, equities have edged higher again with procyclical sectors leading the way. The bond market continues to catch up to the positive vibes evident in other markets with core yields higher across the board.

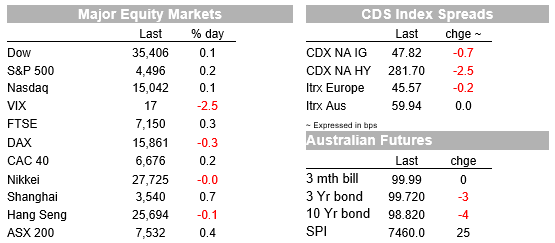

In a low trading environment, equities have edged higher again with procyclical sectors leading the way and in a sign of ongoing improvement in sentiment, the VIX index drifted down overnight and now trades with a16 handle. The bond market continues to catch up to the positive vibes evident in other markets with core yields higher across the board, 10y UST now trade at 1.34%. Pro-growth currencies have outperformed with AUD and NZD up another 0.3% relative to yesterday’s levels, but CAD has been unable to join the party with domestic politics dampening the mood.

The S&P 500 has closed the day up 0.29%, its fifth day of gains in a row, up 2.23% over this period and comfortably surpassing the 1.78% declined recorded in the prior two days last week . Buying the dip continues to be a rewarding strategy amid ongoing accommodative policies from central banks and positive covid news of late. The NASDAQ ended 0.15% higher not showing a great deal of sensitivity the move up in longer dated UST yields ( more on that below), although big tech didn’t have a good day with Apple down -0.84% and Microsoft -0.20%. Early in the session, European equities ended the day with modest gains with the German DAX the exception, down 0.28%.

One factor that might have played into the DAX’s underperformance was the unexpected decline in the headline IFO survey readings . The Business Climate/Confidence index ease to 99.4 from 100.7 and below expectations along with a corresponding dip in Expectations, despite the Current Assessment index rising. Speaking on BBG TV earlier, Clemens Feust, President of the Ifo Institute noted the current concerns facing businesses from supply chains/bottlenecks that are getting worse not better. This is a narrative that is consistent with the big increase in freight cost in recent weeks, with temporary closures of major ports in China (covid restrictions) not helping and supporting the notion that transitory cost pressures from bottlenecks are not yet going away. If producers are able to pass on these costs, more consumer inflationary pressures should be expected.

Meanwhile US data releases painted a more upbeat picture in the US. US durable goods orders for July came close to expectations, with the headline figure dragged down by lower Boeing aircraft orders (-0.1%, marginally better than the consensus, -0.3) but Orders ex-transportation continue to rise at a strong and steady pace, up 14.3% in the three months to July compared to the previous three months.

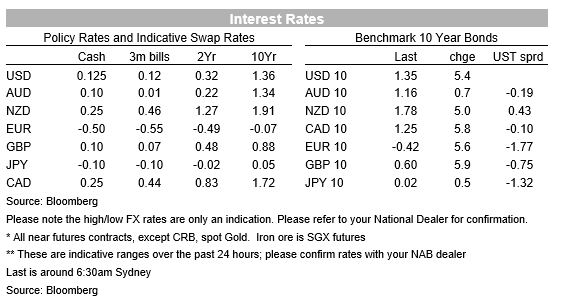

Ahead of Jackson Hole tomorrow and against a quiet backdrop with no major news to move markets, core yields have had a decent move up catching up to the positive vibes evident in other markets in recent days. The UST curve has bear steepened with the 10y and 30y tenors leading the way, up 5.2bps to 1.34% and + 4bps to 1.96% respectively. The sell-off hasn’t been confined to the Treasuries market, with rates higher across Europe as well, including a 6bps lift in Germany’s 10-year rate and a 9bps lift for Italy.

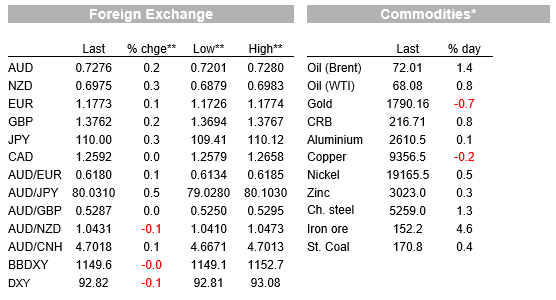

It has been another good night for commodities consistent with the view that investors are seemingly less concerned about the economic outlook this week. Oil prices gained over 1%, iron ore was up 4.6% and copper climbed 0.25% while gold was the notable underperformer, down 0.84%.

Against this backdrop is not surprising to see commodity linked currencies at the top of the G10 leader board. NOK, NZD and AUD are up over 0.30% in the past 24 hours with the AUD now trading close to its overnight high at 0.7276 while NZD is at 0.6974, after printing an overnight high of 0.6984. CAD is the notable underperformer, unable to enjoy the improvement in sentiment given domestic politics. On the election campaign trail, Prime Minister Trudeau has promised to hike taxes on big banks and insurance companies, this news follows yesterday’s promise to implement a two-year ban on foreign home buyers if re-elected.

The USD is little changed index terms (BBDXY @ 1149.6 and DXY @92.83) with the underperformance of safe haven currencies helping offset the gains in pro cyclical pairs. JPY and is down 0.32% and CHF is 0.12%. Meanwhile the euro is up 0.17% to 1.1772, showing little reaction to dovish remarks from ECB Chief Economist Philip Lane. Speaking to Reuters, Lane noted that the ECB is prepared to respond to any market disruptions that may arise when the Fed starts to unwind monetary stimulus. “The ECB is not a passive bystander,” Lane said, “If there are spillovers to euro-area financing conditions, we are willing and able to move as appropriate, as we have already demonstrated.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.