We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

BoJ stuns markets with a 0% YCC tolerance band widening…

Shock and awe from the BoJ yesterday, not via any formal change to the (-0.1%) policy rate or (0%) 10-year JGB YCC policy, but the expansion of the tolerance band around the YCC target to +/-0.5% from +/-0.25%, something that Governor Kuroda has been telling anyone who would listen in recent months was not under consideration, since it would, he said, be tantamount to a rate rose. Last night he told us, ‘The move is not a rate hike’. The BoJ thus takes out our award for the most unpredictable central bank of 2022.

While justifying the move in terms of more effective market functioning and the distortion in the Japanese yield curve at the 10yr YCC target point, alongside claiming it is not a monetary policy change, the shock BoJ announcement has given succour to weekend local media reports suggesting that the government was contemplating a tweak to the BoJ’s remit that would allow for greater flexibility on its part in relation to achieving the 2% inflation target – ostensibly lowering the bar for a move off the negative policy rate and/or 0% YCC target at some stage next year.

Our view on the latter remains that any formal policy changes in this regard are contingent on next Spring’s Shunto (large firms) and Rengo (more SME-focussed) wage negotiations and the need to see outcomes deemed consistent with the 2% inflation target. Only then, and post the appointment of Governor Kuroda’s successor, might be see a policy change. That said yesterday’s tweak has, whatever the BoJ (and government) will have us want to believe, been interpreted as putting the writing on the wall for a policy shift next year almost regardless of the 2023 wage round. It is also seen as signifying a formal end to tolerance/desirability of Yen weakness.

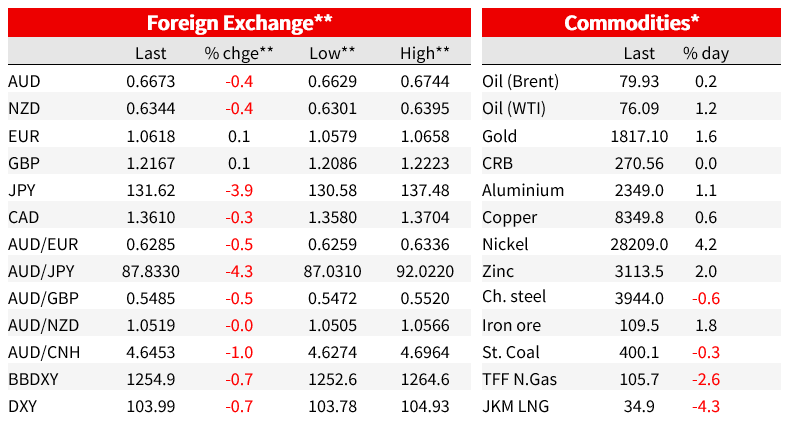

Certainly, the BoJ announcement was the catalyst for a dramatic unwinding of short JPY positions, with AUD/JPY and NZD/JPY the two biggest movers in the hours following the move (some 5.0% for both crosses versus a currently 4.25% move down in USD/JPY). Weight of positioning doubtless had something to do with the AUD and NZD moves. Elsewhere in FX, EUR/USD and GBP/USD were both little changed, meaning that the 0.6% fall in the DXY USD index was almost entirely the fault of the drop in USD/JPY given its 13.5% weight in the index, with marginal additional headwind from CAD (+0.26%) and CHF (+0.17%), the former getting some support from higher WTI crude prices (+1.2%).

10-year JGB yields jumped by 20.5bps to 0.455% (before closing at 39.3bps) and the 5-year JGB yield by some 123bps to 0.26% (all of which was later given back). And, with the 0% YCC target and 0.25% ceiling seen as something of a dragging anchor for bond yields globally, 10-year US Treasury yields are currently some 10bps up on pre-BoJ announcement levels, German Bunds 11.5bps up, 10-year gilts +9bps and, biggest of all, Australian 10-year bonds a whopping 20bps.

Earlier in the Australian session Tuesday, local bond futures were a touch weaker following the release of the Minutes of the RBA’s December Board meeting, at which a 25bps Cash Rate rise was agreed. They revealed the Board considered a wide range of options for policy at this meeting, including a 50bps rate rise and, for the first time since interest rates were first increased in May, a pause in the rate rise cycle. The Board concluded that the arguments for the three different courses of action (no change, +25bps or +50bps) were strongest for increasing the Cash Rate by a further 25bps. Justifying a 25bp hike, “members also noted the importance of acting consistently and that shifting to either larger increases or pausing at this point with no clear impetus from the incoming data would create uncertainty about the bank’s reaction function”.

The very fact that a pause in the rate rise cycle entered the RBA’s thinking in December suggest that one may not be too far off. Indeed, following what NAB expects will be two further 25-point rate rises in February and March, taking the Cash Rate to 3.60% – in line with market rates and which would by then imply the share of household income going to servicing mortgage payments being around their previous (2008) peaks – this still seems to us to be a reasonably best guess for at least a stopping off point. If so, this would by necessity not be a signal that the terminal cash rate has been reached, inevitably being totally data dependent as we go deeper into 2023.

Also, to note yesterday, the ANZ NZ business outlook survey was terrible, with the Business Activity outlook index down to -25.6 from -13.7 in November and confidence at net -70%. As our BNZ research colleagues noted, “It doesn’t get much worse than this”. Apart from the March 2020 lockdown, the own-activity indicator hasn’t been this low, now surpassing the GFC low. They say it all points to a larger recession than currently factored in by the consensus, engineered by the RBNZ.

Data out overnight has been mostly second tier. US Housing Starts were les bad than feared, -0.5% against -1.8% expected, with October revised up to -2.1% from -4.2%. That said, Building Permits slumped by 11.2% against a fall of just 2.1% expected Canadian retail sales meanwhile came in much as expected at 1.4% m/m (1.5% consensus) and even better than expected ex-autos (1.7% vs. 1.3% consensus). Eurozone consumer confidence, also out overnight, improved slightly to a still dire -22.2 from -23.9, in line with expectations.

In equities, coming into the last hour of NYSE trade, the S&P500 is clinging to just-positive change-on-the day territory (+0.2%) but the NASDAQ is essentially flat, so whether we will break a four-day losing streak for the former remains to be seen. It’s the energy sector (+1.6%) currently holding the index in the green thanks to the rise in WTI crude, with the (recession sensitive) Consumer Discretionary sector far and away the worst performer, currently -0.9%. Earleir Tuesday, the Nikkei finished the day down 2.5% thanks to the much stronger yen, while European bourses finished narrowly mixed.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.