Robust growth for online retail sales observed in June

Insight

Very weak US retail and industrial production adds to the tumble in yields

“Where do you, where do you go?; You leave without a word, no message, no number; And now my head is pounding like rolling thunder”, Where Do you Go, No Mercy, 1996

‘Bad news is bad news’ once again for markets with weak retail sales and industrial production seeing risk assets sell-off and yields extending their declines seen after the BoJ yesterday (US retail excl. auto and agas -0.7% m/m vs. 0.0% exp and prior month revised down to -0.5% from -0.2%). The weak data has supported a US recession view in 2023, pushing back on the soft landing narrative that has pervaded markets since the beginning of the year. The NY Fed also released their 3m/10yr yield curve recession indicator for December, with this model ascribing a 47.3% chance of recession the highest since 1982 (note December 3m/10yr curve was inverted by -73bps, now it is -129bps).

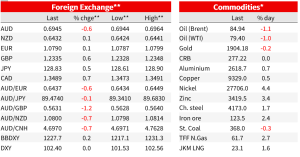

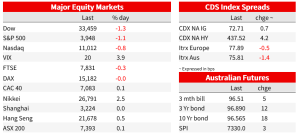

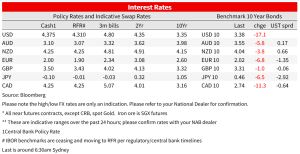

The S&P500 is down -1.1% as we head into the close, and once again has failed to convincingly break the 200 day moving average, though the S&P is still up 2.8% for the year. Despite the weak data, Fed speak remained hawkish, and ECB speakers pushed back on the earlier dovish Bloomberg-ECB sources story. US rate hike expectations have been pared further with a peak of 4.87% by June 2023, down from 4.915% yesterday, and thereafter 52bps of cuts in H2 2023. Combined with the BoJ standing pat yesterday (see below) yields have tumbled. The US 2yr yield is now down -11.4bps over the past 24 hours to 4.08%, along with the 10yr -15.5bps to 3.38%. Declines have been reflected in real yields with the 10yr TIP yield -12.1bps to 1.23%. The implied inflation breakeven in contrast is only down slightly by around -3bps to 2.13%.

Meanwhile in Japan the 10yr traded as low as 0.36% post the BoJ as short positions were culled, and rose back to 0.46% FX has been volatile, especially USD/JPY after the BoJ yesterday. USD/JPY jumped as much as 2.4% to 131.58, before paring the gain, with the pair back close to the pre-meeting level, trading this morning at 128.83 to be up just 0.5% over the past 24 hours. Weaker US data was the catalyst for a turn in the USD DXY (at one point it was up 0.5%, then down -1.3% as weaker US data hit before recovering) and on net is little changed over the past 24 hours at 102.42. Other pairs showed similar moves with a spike higher on USD weakness, before paring and in some cases finishing lower. The AUD hit a fresh 5-month high of 0.7063 but is now more than a cent lower at 0.6945 and is down -0.6% over the past 24 hours. GBP outperformed, +0.6% as strong core inflation means the BoE will need to remain aggressive.

As for details on the US data, it was much weaker than expected, though it is unclear to what extent the severe winter storms may have weighed towards the end of December. Headline retail was -1.1% m/m vs -0.9% exp, and the prior month was revised lower to -1.0% m/m from -0.6% m/m. The important core control measure was also weak at -0.7% m/m against -0.3% expected. Similarly industrial production was -0.7% m/m vs. -0.1% expected, and the prior month was revised lower to -0.6% m/m from -0.2%. On the prices side the PPI was -0.5% m/m vs. -0.1% expected, while core PPI was as expected at 0.1% m/m. The decline in retail spending and industrial production adds to the theme of the economy slowing and heading into recession in 2023, and pushes back on the soft landing narrative dominating markets since January.

Adding to the gloom were more job layoffs in the tech sector with Microsoft planning 10,000 job cuts or close to 5% of its workforce “in response to macroeconomic conditions and changing customer priorities” (see WSJ: Microsoft to Lay Off 10,000 Workers as Slowdown Hits Software Business ). Bank of America has also paused new hiring except for the most vital positions. Some retailers in the past few weeks had also said the holiday shopping season turned out to be weaker than expected. Reflecting these anecdotes, the Fed’s Beige Book painted a flat to declining picture of activity with five districts at slight/modest increases in activity, six reporting no change, and one reporting a significant decline (see Fed Beige Book). Fed speak also remained hawkish.The Fed’s Bullard said “we’re almost into a zone that we could call restrictive – we’re not quite there yet”. Similarly the Fed’s Mester “ We’re not at 5% yet, we’re not above 5%, which I think is going to be needed given where my projections are for the economy,” and “I just think we need to keep going, and we’ll discuss at the meeting how much to do”. Heavy hitters Williams and Brainard speak tomorrow, ahead of the blackout period for the 1 February FOMC meeting.

As for the BoJ yesterday, the BoJ kept the yield target unchanged and also kept their core inflation forecast excluding food and energy at 1.6% for 2024. This was in line with the consensus view, but the market was positioned for another possible surprise move. The BoJ has been buying JGBs in record amounts at an unsustainable pace and the unchanged policy stance won’t budge market expectations that YCC will end sometime in H1 2023. Governor Kuroda has one last meeting before passing the baton to a new Governor, yet to be announced, which will be the next key BoJ event – the market then trying to second-guess how hawkish the new Governor will be and how he handles the “hospital pass” if Kuroda leaves policy unchanged in March.

Finally on the inflation front, in the UK Core CPI was one-tenth hotter than expected at 6.3% y/y vs. 6.2 expected, and bolstering expectations the BoE will hike by another 50bps. Meanwhile for oil the IEA reported that demand is expected to reach a record daily average this year, with about half of the growth coming from a rebounding China. A further lift in oil prices – with some suggesting that a return to USD100 per barrel could happen – would spoil the lower headline inflation narrative that has been emerging.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.