On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

USD softer despite ‘risk-off’ market tone.

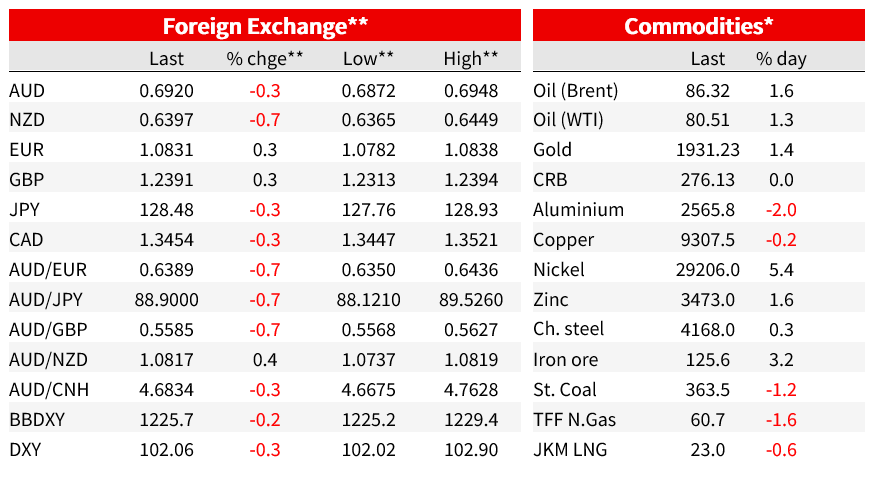

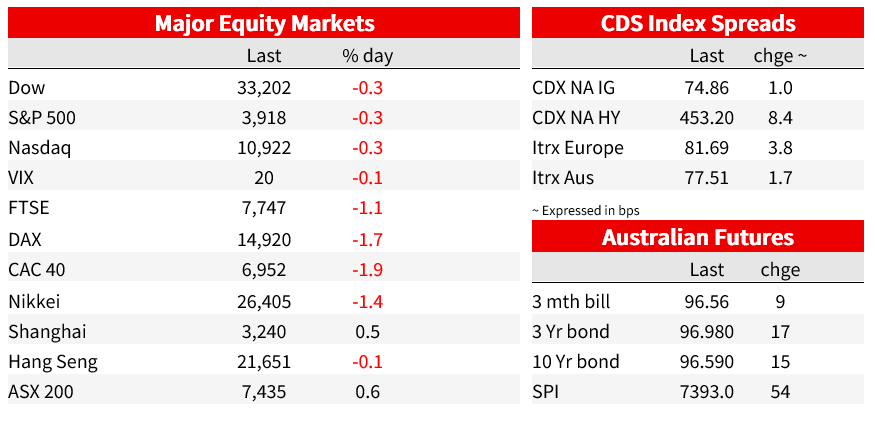

US markets are coming into the last hour of NYSE trade showing minor losses averaging 0.3% for the main board indices, after falls of more than 1% and as much as 2% for European stock markets. Netflix will report its earnings after the close. The generally risk-off tone is not evident in currencies though where the DXY index is about 0.3% lower thanks to gains for the EUR, GBP, and JPY, while AUD is back comfortably onto a 0.69 handle (0.6920) having been as low as 0.6872 following yesterday’s softer than expected Employment report. US bond yields have maintained the 3-4bps back-up witnessed during out time zone yesterday.

Fed Vice chair Lael Brainard , a key voice on the FOMC, has just been speaking, and while the headlines are very much on message (the FOMC will ‘stay the course’ and ‘policy will need to be sufficiently restrictive for some time in bringing inflation down’) there is an acknowledgement that as well as inflation having declined in recent months, data on retail sales and industrial production showed a slowdown in economic growth and that forward looking indicators suggest growth will slow further in 2023 due to the lags with which monetary policy operates. And, she says, policy is now in restrictive territory. She has said nothing explicit about the market being wrong to think rates might come down before 2023 is out.

‘Stay the course’ was also the mantra from ECB President Christine Lagarde speaking on a panel in Davos, who said “On inflation we have way-too high numbers….We shall stay the course until such a time when we have moved into restrictive territory for long enough so that we can return inflation to 2% in a timely manner.” In an apparent push-back to the Bloomberg story earlier this week suggesting the ECB might limit future rate increases (i.e. to less than 50bps, at least after the February decision). Ms. Lagarde said she would advise investors to “revise their position.”. Dutch central-bank governor, Klaas Knot – one of the known ECB hawks – was even more explicit, arguing that “most of the ground we have to cover will have to take place at a constant pace of multiple 0.5-point rate hikes”.

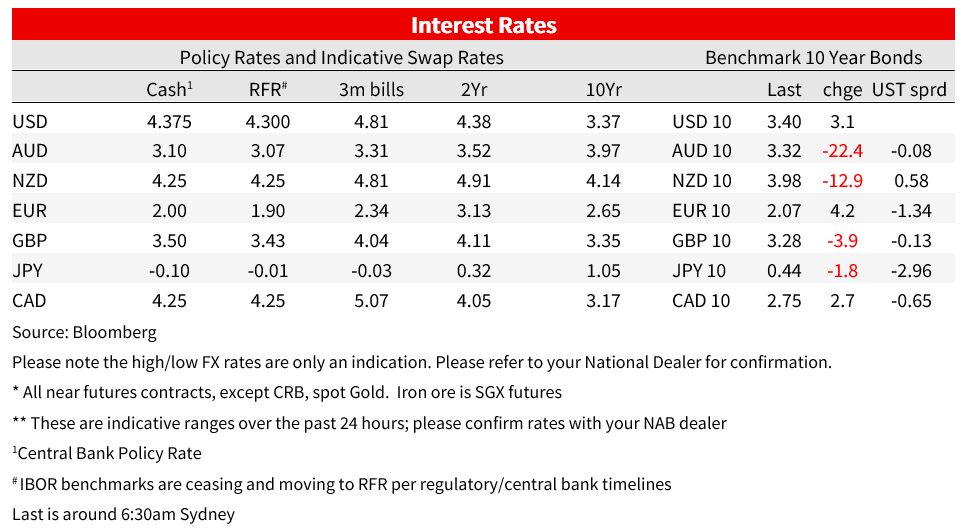

Evidently less hawkish than these latest ECB speakers, BoE Governor Andrew Bailey gave an interview in which he said that the last two months’ of decline in headline inflation meant that the UK may be turning the corner on its cost-of-living squeeze, and that ‘the most likely outcome is that (inflation) will fall quite rapidly, probably starting in the late Spring, and that has a lot to do with energy prices’. While still expressing concerns about labour market tightness and its impact on pay and acknowledging signs that ‘if anything it is still rising a bit’, he says some of the forward-looking surveys of earnings and pay ‘are not as strong as that actually’. On monetary policy, Bailey said that market interest rate expectations are now more closely aligned with the BoE’s thinking on where rates peak (currently seen around 4.5%, versus 3.5% now).

US economic data overnight was mostly second tier and not obviously market moving. Housing Starts and Building Permits both declined on the month, by 1.4% and 1.6% respectively, the former less than expected and the latter by more than expected. The Philly Fed survey failed to replicate the extreme weakness seen in the earlier Empire survey, instead lifting to a (still weak) -8.9 from -13.7 and against an expected improvement to -11. Weekly jobless claims meanwhile fell to below 200k (190k) though Continuing Claims rose from 1,630k to 1,647k, albeit a bit less than expected. The latter level remains consistent with US recession this year.

There was nothing to frighten the US bond market vigilantes in these remarks, the 3-4bps back-up in Treasury yields since Wednesday’s NY close having occurred mostly in the Tokyo market yesterday. Similarly, no real reaction to the headline grabbling news that the US government has now bumped up against the debt ceiling and so begun taking special measures to keep paying its bills. These can likely continue through mid-year at least but will likely be an all-consuming issue inside the Washington beltway in the weeks and months ahead. The now Republican controlled House sees the debt ceiling as just about the only leverage it has to try wind back some of the Biden administration’s fiscal policies enacted in the last year or so, such as increased funding for the Internal revenue Service, designed to improve tax collection.

The local rates market in contrast saw a significant reaction yesterday to the Australian labour market data which showed unemployment at 3.5%, unchanged but from an upward revised – from 3.4% – November print even with the participation rate dropping 2/10s to 66.6%, and employment falling by 14.6k against expectations for a 25.0k rise. The yield on 3-year bond futures fell by as much as 14bps post the data, and at one point in the afternoon money market futures were slightly better priced for no change than +25bps out of the 7 February RBA meeting (15bps priced at the close). Next Wednesday’s Q4 CPI will obviously be important here.

The softer than expected labour market data also kicked an Australian dollar than was already well down from its early week highs above 0.70, dropping from around 0.6950 to 0.6900 in short order. Losses extended to as low as 0.6872 overnight but AUD has perked up in the New York afternoon to now be quite comfortably back onto a 0.69 handle (0.6920 now).

Currency moves elsewhere show a somewhat bigger fall for the NZD than AUD in the last 24 hours, making the bird the weakest of the G10 pack, while the JPY is the strongest, maintaining most of the gains seen during our time zone yesterday and meaning USD/JPY now trades below its pre-BoJ no-change level. This plus gains of 0.4% for the EUR and GBP mean that the DXY index is a third of a percent lower, notwithstanding the generally risk-off equity market tone.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.