Coming in for landing in a heavy cross wind

Insight

US equities stage a late recovery, but remain edgy

AU: Private capital exp (q/q%), Q4: 2.2 vs 1.1 exp.

US: GDP (2nd est. ann’lsd q/q%), Q4: 2.7 vs 2.9 exp.

US: Core PCE (2nd est. QoQ), Q4: 4.3 vs 3.9 exp.

US: Initial jobless claims (k), 18-Feb: 192 vs 200 exp.

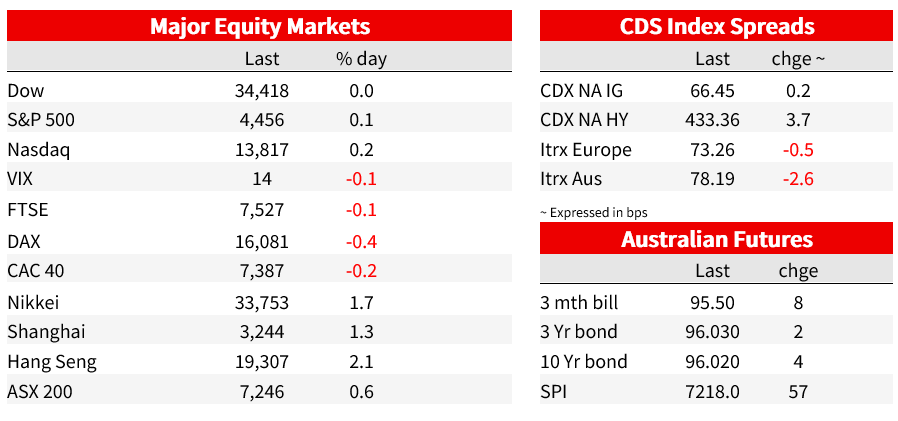

Equity markets remain edgy amid an uncertain economic and central bank outlook. After initially trading higher the S&P 500 fell close to 1.4% intraday, only to recover in the past hour. Q4 US GDP was revised lower with the consumer not as buoyant as initially thought, but at same time the core PCE deflator rose more quickly than previously believed. Meanwhile Jobless claims continue to suggest the US labour market remains in rude health. Conclusion from the US overnight data releases is that the Fed still has more work to do, rattling risk assets. 10y UST trade up to 3.97%, then down to 3.87%, the UST curve is flatter on the day while the USD is broadly stronger, extending recent gains. AUD starts the new day back above 68c.

US equities started the overnight session on a positive mood, the S&P 500 opened higher, extending gains during the first our trading to almost +1%, then it was all downhill falling over 1.4% intraday, followed by a decent recovery in the last hours. Overall, the price action reflects an edgy market that remains uncertain on the outlook, not knowing which way to go. The S&P 500 now trades up 0.60% on the day while the NASDAQ is 0.78%.A look at the S&P sector reveals a mixed picture, energy and IT are up on the day but consumer related sectors as well as Utilities and Communication Services have struggled.

US economic data releases have added an extra layer of edginess. Q4 US GDP was revised lower with the consumer not as buoyant as initially thought, but at same time the core PCE deflator rose more quickly than previously believed. Q4 GDP growth was revised down to 2.7% from 2.9%, below the consensus for an unchanged outcome. The decline was largely due to a downward consumption revisions, cut to 1.4% from 2.1%, with stronger investment spending only a partial offset. Q4 PCE readings were revised higher, suggesting the US economy ended last year running hotter than previously thought, the core PCE was revised to 4.3% (qoq SAAR), up from the initial 3.9% estimate.

Meanwhile jobless claims surprised with a lower print. Claims fell to 192k during the week ended February 18 from an upwardly revised 195k level in the previous week, compared with expectations for an increase to 200k. Stronger weather and seasonals have yet again been sighted as the culprit for the economists miss, still the conclusion must be that the US labour market remains in rude health, notwithstanding known headwinds from tighter Fed policy. Inflation is also higher now than previously thought, so the Fed still has more work to do.

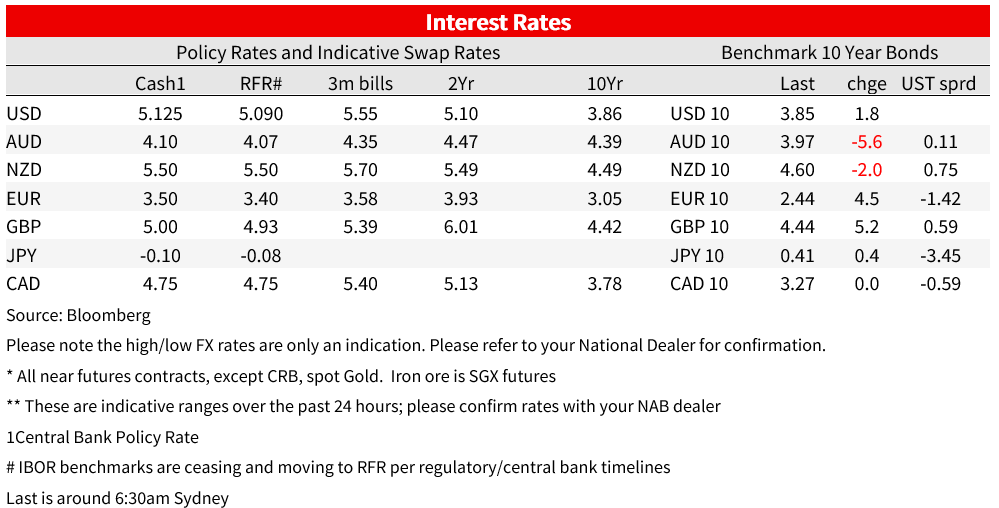

This uncertainty is not only keeping equity investors nervous, the rates market is also edgy with the MOVE index (a UST rates volatility index) continuing to rise, now at 118, up 20 points from its recent low at the start of the month . Indeed, overnight price action on the 10y UST note is a good illustration of this edginess, the benchmark yield initially traded to a high of 3.97%, but now trades 10bps lower at 3.87% and 2bps lower relative to yesterday’s closing levels. The UST curve is mildly flatter with the 2y yield unchanged at 4.697%.

Earlier in the session 10y Bunds ended the day 4.4bps lower at 2.47% while 10y UK gilts close 1bps lower at 3.583%. The UK Gilt curve continues to invert with front end yields edging a little bit higher again after BoE Man (known hawk) said that more hikes are needed while cautioning that a pivot is not imminent. The OIS market lifted the expected peak on the BOE rate to as high as 4.75% before easing to 4.69%, still 4bps higher than Wednesday.

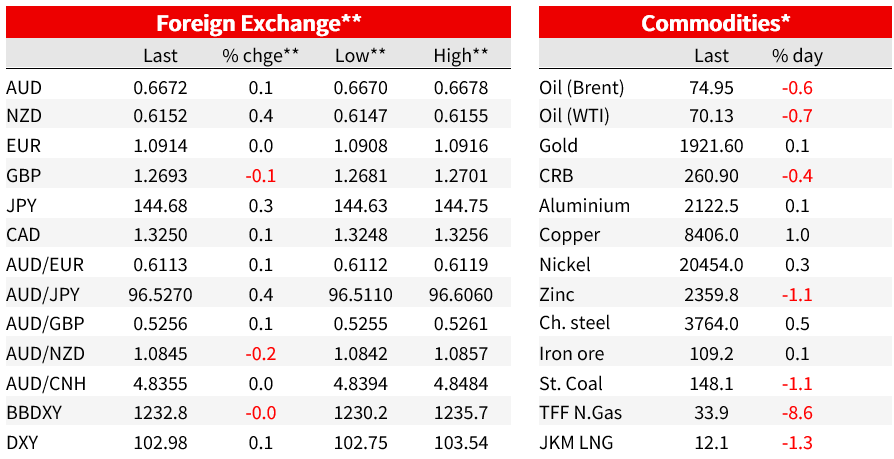

Moving onto FX land, the USD continues to benefit from the risk aversion in the air and the prospect of more Fed rate hikes ahead. Both BBDXY and DXY are up around 0.12% with the greenback stronger across all G10 pair barring NOK which is up 0.17% on the back of a decent rebound in oil prices. Both Brent and WTI oil are up close to 1.8% following a forecast for record Indian demand and the prospect of Russia curbing exports.

The hawkish talk from BoE Mann didn’t help sterling with the pair at the bottom of the leader board, down 0.25% to 1.2018. The prospect of a potential UK EU deal on N.Ireland is a theme to watch over the coming days.

The euro edged lower not helped by the decline in Bund yields and now trades at 1.0597 while the AUD and NZD have staged a small recovery in the past hour as US equities rebound . The AUD now trades at 0.6813, after trading down to an overnight low of 0.6782. The AUD continues to show a high degree of sensitivity to risk appetite, trading in a similar pattern to the S&P 500. NZD mostly traded its post-MPS 0.6210-0.6250 range through the night but tested through the bottom of that this morning as the USD strengthen. The kiwi starts the new day at 0.6231.

USD/JPY found resistance yet again above the ¥135 mark and now trades ta ¥134.67. Ueda-san, BoJ Governor nominee will be speaking before the Diet today and the market will be watching him very closely. Ueda remains an unknown quantity, so any hints as to whether he remains supportive of the current BoJ ultra-easy policy or not will be important for JPY’s outlook as well as rates markets.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.