Total spending grew 0.9% in June.

US yields resumed their grind higher to start the new week, though there was little news to speak of, while US equities where higher.

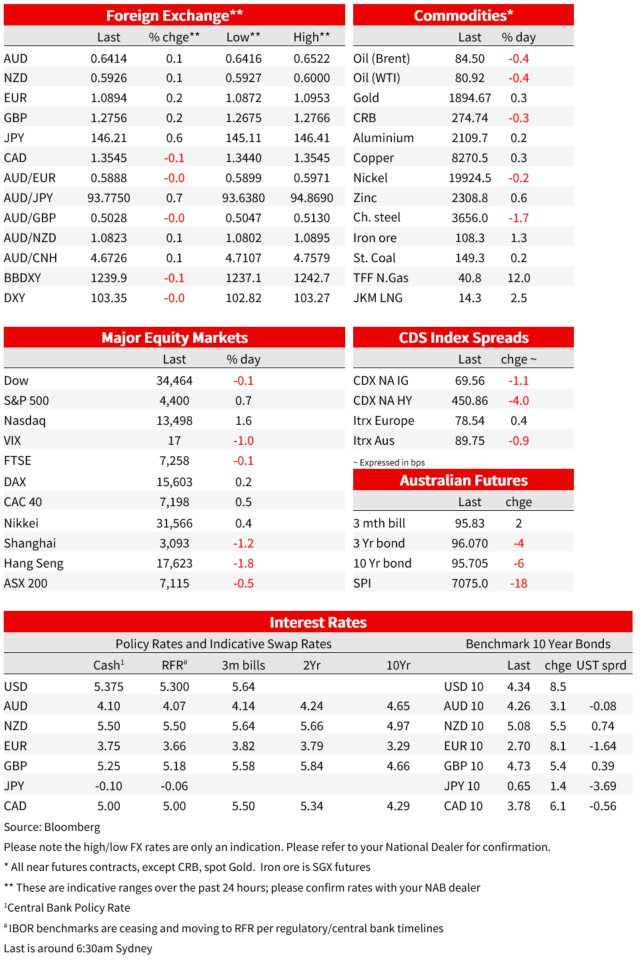

US yields resumed their grind higher to start the new week, though there was little news to speak of. Higher yields were again led by the longer end. The 10yr yield touching its highest since 2007 intraday, while real 10yr yields rose past 2% for the first time since 2009. Despite higher yields, US equities were stronger, up 0.7% on the S&P500 and led by tech.

The US dollar begins the new week down less than 0.1% on the DXY. That narrow daily decline coming after 5 straight weeks of appreciation. The dollar was lower against all G10 currencies except the yen, which was the notable underperformer on the day. USDJPY was 0.6% higher, touching 146.40 intraday to now sit around 146.22. CNHJPY was 0.8% higher and through 20, now sitting around 20.067. The AUD was up 0.1 on the day to 0.6414 after oscillating near 0.64 for most of the day.

In China yesterday, the 1-yr loan prime rate was cute by 10bp, less than the expected 15bp reduction and the 5-yr loan prime rate was left unchanged, where a 15bp cut was also expected, was left unchanged. Those following the PBoC decision last week to lower the MLF rate by 15bp. The 5yr rate is a key benchmark for mortgage lending, while the 1yr rate is a benchmark for most corporate and households loans. There are doubts about the effectiveness of further monetary policy stimulus ability to support sluggish credit demand, with the narrower follow through from the lending finance rate last week leaving hopes for broader stimulus with fiscal policy. The Hang Seng was 1.8% lower, while the CSI 300 lost 1.4%. The yuan was weaker through much of the Asian trading session, USD/CNH pushing up towards 7.34, but is back below 7.29 this morning.

US yields resumed their rise on Monday, with the rise in yields again led by the long end . 10yr Yields were 8bp higher to 4.34%, that after a selloff in the US morning say yields rise above 4.34% and to their highest since 2007. The yield on 10-year inflation-protected Treasuries pushed over 2% for the first time since 2009. The moves were without a fresh catalyst and amid light volumes. The 2yr yield was 6bp higher to 5.00%. In Europe, Germany’s 10-year yield was up 8bps to 2.70% and the UK 10-year rate up 5bps to 4.73%.

Despite higher yields, US equities rose, led by big tech names. The S&P 500 was 0.7% higher, while the Nasdaq was up some 1.6%. Tesla share showed their first increase in 6 days, while Nvidia was almost 7% higher. Nvidia is set to report results on Wednesday. Within the S&P500, IT led gains, up 2.3%, while Real Estate, Consumer Staples, Energy, and Utilities showed declines of more than 0.5%.

Elsewhere, European natural gas was up 12% to a 2-month high on strike concerns among Australian LNG workers. Bloomberg reports that potential strikes among workers at export facilities could disrupt 10% of the world’s LNG flows. Unions warned over the weekend that industrial action could start as soon as Sept. 2 at a facility of Woodside Energy Group if no deal is reached in pay talks on Wednesday.

The data calendar has been light but of some interest was much lower than expected German PPI inflation. PPI fell 6% y/y, driven by the sharp decline in wholesale energy prices, while prices declined in other areas as well, such as intermediate goods. Produces prices in the July month were 1.1% lower. The Bundesbank monthly report said that “the German economy continues to be in a weak phase,” and that “in the third quarter of 2023, economic output is likely to remain virtually unchanged again,” as a result of weak global demand weighing on exports and higher interest rates.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.