Total spending grew 0.9% in June.

The US 10yr finally breached 4.00% for the first time since November, following five days of resistance. A hot German CPI and renewed price pressure in the Manufacturing ISM drove, while risk assets were mixed given the strong China PMIs yesterday

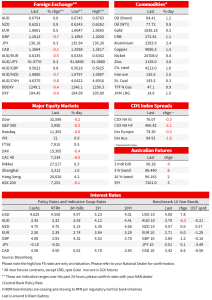

The US 10yr finally breached 4.00% for the first time since November, following five days of resistance. The 10yr yield rose +8.0bps to 4.0% overnight. A hot German CPI (9.3% y/y vs. 9.0 expected) and renewed price pressure in the Manufacturing ISM drove (ISM Prices Paid 51.3 vs. 46.5 expected), while risk assets were mixed given the strong China PMIs yesterday. ECB pricing has lifted further with 150bps worth of more tightening priced for the rest of 2023 compared to 139bps yesterday, and markets are ascribing a 97% chance of a 50bp hike in March and a 65% chance of a follow up 50bp in May. US Fed pricing has also lifted again with terminal now at 5.46% by September, up from 5.42% yesterday. Short-end yields are higher with the US 2yr up 7.0bps to 4.89%. Equities were whippy, but the S&P in the red at -0.6% into the close. The USD (DXY) was weaker -0.3%, with strength in EUR +0.5%, while the strong China PMIs yesterday saw the AUD rebound after initially falling after GDP/CPI data yesterday: AUD +0.0%.

First to the German CPI for February which again shows inflation becoming sticky. Headline German CPI was 1.0% m/m vs. 0.7% expected, taking the annual rate to 9.3% y/y against 9.0% expected. Within the details, it was the services side that showed inflation was becoming broad-based and sticky with services inflation at 4.7% y/y, up from 4.5% in January and 3.9% in December. In short there is more work for the ECB to do to rein in inflationary pressures. Bundesbank President Nagel warned core inflation pressures remain elevated and that inflation is only likely to retreat gradually: “One thing is clear: the interest-rate step announced for March will not be the last” and “Further significant interest-rate steps might even be necessary afterwards, too ”. ECB’s Visco made similar remarks, while Villeroy was less hawkish. Markets upped ECB pricing to 150bps worth of more hikes, up from 139bps yesterday, and are almost fully pricing a 50bp hike in March. The 10yr Bund yield rose 6.0bps to 2.71%.

As for the US ISM Manufacturing, it remained in contraction, but the most interest was in the prices component. The overall index was 47.7 vs. 48.0 expected and 47.4 previously. The Prices Paid Index though rose more sharply to 51.3 vs. 46.5 expected from 44.5 previously. And indeed over the past two months, the Prices Paid Index has risen 11.9 percentage points. The ISM noted that “Panellists comments support a return to more balanced supplier-buyer relationships, as sellers are more interested in filling order books and buyers now see the need to reorder. Also, future price increases are apparent for foundational purchased materials in several sectors ”. As for other important sub-indexes, Employment dipped back into contraction at 49.1 from 50.6, New Orders were 47.0 from 42.5, Production was 47.3 from 48.0. Anecdotes were very mixed within he survey (see Manufacturing ISM Report on Business for details).

Equities have been whippy, but are now in the red. The S&P500 is currently -0.6% into the close, while across the pond the Eurostoxx50 was -0.5%. Meanwhile, online job advertising continues to hint that the US labour market is not as strong as official numbers suggest with ZipRecruiter and Recruit Holdings showing their job postings are declining more than the official JOLTS data (see WSJ: Long-Robust U.S. Labor Market Shows Signs of Cooling). Helping support risk assets in Asia and into the overnight session were strong China PMIs yesterday with Manufacturing at 52.6 vs. 50.6 expected, and Non-manufacturing 56.3 vs. 54.9. Details showed much of the rebound is being driven by ‘old-fashioned’ infrastructure spending (the Construction-only PMI, which is actually a sub-set of the Non-manufacturing PMI, rose to 60.2 from 56.4 as local governments increased special bonds linked to infrastructure spending). China is also expected to unveil a growth target on Sunday at the National People’s Congress.

Needless to say, a China rebound led by infrastructure (again) is supportive for commodity prices and the AUD (and other commodity-linked currencies. No surprises then to see the AUD quickly reverse the initial -0.5% drop following yesterday’s softer GDP and Monthly CPI Indicator data, with the AUD broadly unchanged over the past 24 hours at 0.6753. The NZD has certainly benefited from the China data with the NZD +0.8% to 0.6251. Meanwhile the USD (DXY) was softer overnight -0.3%, with EUR +0.5% as hot inflation means higher rates. Commodities rose with Aluminium +2.4%, Copper +1.5%, Zinc +3.8%, and Brent Oil +1.0%

One exception was GBP which was -0.7% as BoE Governor Bailley was less hawkish (in contrast to his peers at the ECB and Fed), stating: “I would caution against suggesting either that we are done with increasing Bank Rate, or that we will inevitably need to do more’ going to say ‘some further increase in Bank Rate may turn out to be appropriate, but nothing is decided. ” The market trimmed expectations of the BoE rate peak by about 10bps, seeing closer to three 25bp hikes by year’s end effectively removing the decent chance of a fourth hike that had previously been built in. Gilts outperformed other European bonds, with 2-year yields down about 2bps while 10-year yields rose 2bps. Your scribe would caution though, look at the data, rather than what central banks are saying given how wrong footed they have been over the past few years.

Finally in Australia, yesterday saw softer than expected GDP and inflation from the Monthly CPI Indicator. GDP rose by 0.5% q/q vs. 0.8% expected, and the inflation indicator was 7.4% y/y vs. 8.1% expected. Neither really change the near-term story of inflation being too high and the RBA needing to hike rates further. What it does probably say is activity is likely to respond to higher rates, while some of the disinflation that we expected to see may start to emerge in coming months. In January: (1) goods deflation in excess of ordinary seasonality was seen with furniture prices -1.6% m/m, more than the 0.7-0.8 falls seen in Januarys prior to the pandemic. Clothing prices were -3.6% m/m, again outpacing the 2.1-2.3 falls seen prior to the pandemic; and (2) a turn in travel costs may also be occurring with prices -7.2% m/m, much more than the 1.5-2.5 falls seen in pre-pandemic Januarys. However, it still remains unclear how much demand needs to moderate to reduce inflationary pressures and it is worth noting that while real GDP increased by 0.5% q/q, nominal GDP rose 2.1% q/q and 12.0% y/y.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.