NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

The ECB delivered on its 50bps rate promise but scraps forward guidance. Meanwhile the US’ First Republic Bank gets a $30bn deposit injection from other banks

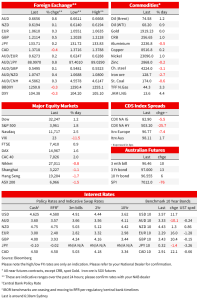

Offshore markets, be they currencies, rates, credit or equities, have traded in calmer fashion overnight than was the case on Wednesday when the Credit Suisse news barrelled through markets globally, the SNB’s announcement of a CHF540bn liquidity backstop for Credit Suisse going some way to restoring order. The ECB has delivered the much-heralded 50bps hike to its Refinancing Rate, but in doing so dropping any pretence at forward guidance, as a result of which money markets now see only one further rate hike in this cycle, of just 25bps and even then not before Q3. A positive session for European equities (Eurostoxx 50 +2%) has followed through to the US with the S&P500 closing up 1.8% Bond yields are smartly higher and the US dollar a touch softer, AUD a little firmer.

More orderly market conditions Thursday entailing a partial reversal of many of the mid-week, Credit-Suisse news related moves, actually began late in the New York late Wednesday/yesterday morning In APAC, following the announcement that Credit Suisse was set to borrow as much as CHF50bn from the SNB to shore up its liquidity position. In short, CS is not to be allowed to go under, unlike SVB and Signature bank before it. Then overnight, we’ve learned that First Republic Bank , the object of significant deposit outflows in recent days, is to receive a $30bn deposit injection (for at least 120 days) courtesy of a large consortium of US banks – including all the big/systematically important ones – by way of a (Fed/regulator orchestrated) show of support. Credit Suisse’s share price was up 19% Thursday, and First Republic is 12% up on Wednesday’s close following an earlier trading halt. The KBW Bank Index is up 2.5%. Credit Spreads are tighter (by between 4-20bps on various indices we track) and despite higher Treasury bond yields, overall US financial conditions are a touch easier on the day.

The ECB delivered on its well-flagged 50bps hike to all its main interest rates, undeterred by recent market ructions, though in doing so President Lagarde has scratched forward guidance. Though indicating that there is more work to do, this is caveated with the comments that ‘it is not possible to comment at this point on the rate path’ and noting that financial data as well as economic data are now policy determinants. Following the announcements, Eurozone money markets ended Thursday priced for only an additional 22bps worth of tightening in this cycle (with a high probability attached to a pause at the next (May 4) meeting Accompanying the announcements, The ECB’s new staff forecasts now show HICP at 4.6% in 2023, revised up from 4.2%, with headline down to 5.3% from 6.3%, and in 2024, HICP to 2.9% from 3.4%

US economic news has been largely ignored by market but showed a sharper than expected fall in weekly jobless claims, to 192k down from 212k, confirming the prior week’s spike to be largely weather related (California and Upper Mid-West snowstorms). Housing Starts were much stronger than expected , up 9.8% against a consensus for little change, and permits up 13.8%, though strength was dominated by the volatile multi-family (i.e. apartments) series – much as is often the case in Australia’s equivalent building approvals data. In contrast, the Philly Fed survey was little changed at -23.2 against expectations for a bounce to -15.0. As with the Empire survey earlier this week, no read though from China PMIs to the US, as has historically been the case.

Yesterday’s Australia February Labour Force Survey showed employment rose 65k, confirming our assessment that January was seasonally affected and says that despite the softer December and January prints, the labour market remains tight, though likely a little less so than 6 months ago. The unemployment rate fell to 3.54% (consensus and NAB 3.6%), back to its December level, while participation rebounded as expected to 66.6%. The RBA was looking for a rebound in employment to confirm their assessment of the labour market and they got it in today’s data. Together, we view this week’s NAB Survey and Thursday’s employment data as supportive of an April hike from the RBA.

In bond markets , there may have been a little less violence around Thursday than on Wednesday and other recent trading sessions, but big moves again nonetheless, US 10-year Treasuries currently 11.5bps up on the day to 3.57% and 2s a much bigger 27.4bps to 4.16%. US money markets now price a 25bps lift to the Fed funds target next week at about 80%, having been closer to 50:50 on Wednesday. European bonds also see double digit yields gains at both the short and longer ends (see table below). Implied yields on 3-year Aussie bond futures are about 15bps higher than where the local market left off Thursday.

Currency markets see the USD down about a quarter of a percent in index terms, improved risk sentiment dominating the back-up in US yields (but where the latter have been largely matched or exceeded elsewhere). All G10 currencies are firmer against the USD bar a little-changed USD/JPY, AUD and GBP both by about 0.5% and exceeding the 0.35% rise in EUR/USD, so in effect the ECB’s actions failing to offer direct support despite the 50bps rate rise, thanks to the revised/lack of forward guidance.

US equities have just closed with the S&P500 +1.8and the NASDAQ 2.5%. The VIX is off 3 points to 23. Oil is modestly higher (Brent crude up just over 1%) sand gold is very marginally (0.1%) up at $1,920.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.