NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

A deal was struck over the weekend that sees UBS buying Credit Suisse for CHF3.0bn, a fraction of its value at Friday’s close. Iitial market response, in FX at least, has been (cautiously) favourable.

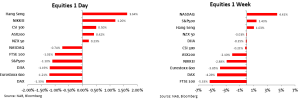

The travails of the US regional banking system and in Europe, Credit Suisse, continued to barrel though global markets on Friday. Thursday’s bounce in European and US equities has proved to be very much of the ‘dead cat’ variety, albeit Friday’s loss for the S&P500 was limited to 1.1% (financials -2.7%) and the Eurostoxx 50 to 1.3%. The KBW bank index lost another 5%, to now bring its March-to-date loss to 28%. First Republic Bank’s shares lost 33% Friday (so much for that $30bn mid-week deposit injection from other banks) while Credit Suisse was down 8% to CHF1.86, having jumped from 1.697 to 2.022 on Thursday following news of the CHF50bn loan from the SNB.

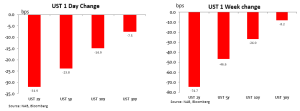

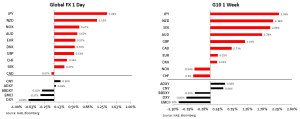

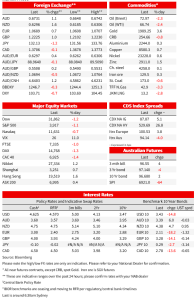

Elsewhere another precipitous fall in front-end US Treasury yields (2s down 32bps) is, for now at least, overriding ‘risk-off’ considerations to see the USD weaker, such that it was an up day (and week) for AUD/USD, closing very close to 0.6700 (0.6738 now on the UBS/CS news). JPY though was the week’s standout winner, benefitting unambiguously from both falling US yields and risk-aversion.

In what the FT describes as a shotgun wedding, UBS has agreed to buy Credit Suisse after increasing its offer to more than $2bn , with Swiss authorities poised to change the country’s laws to bypass a shareholder vote as they rush to announce a deal before Monday. The all-share deal will be priced at a fraction of Credit Suisse’s closing share price on Friday. Having been reported earlier in the night that UBS would buy CS for CHF0.50 a share of UBS’ own stock (up from a bid of CHF0.25 earlier in the day), so a little over 25% of CS’s closing share price of CHF1.86 on Friday, incoming reports are that the purchase price will be CHF0.76 per share.

The SNB has reportedly agreed to offer UBS a $100bn liquidity line as part of the deal, FT sources say, while the newswires are also no saying the Swiss government is to grant UBS a CHF9bn guarantee on CS losses. Shareholders are already expressing anger, as you would no doubt expect, but at least one source of contagion in the global banking sector has just been cauterised.

In other banking sector news since Friday’s market close, Bloomberg on Saturday night reported that Biden administration officials have been in touch with Warren Buffett in recent days in regard to the US regional banking crisis. There was no indication as to what if any role Buffett might play, though of course he has has form in leveraging his legendary investor status to the US financial system, providing capital injections into both Goldman Sachs (2008) and Bank of America (2011) during the GFC.

And also late Saturday night US time, Bloomberg reported that First Citizens Bancshares Inc. is evaluating an offer for SVB, said by Bloomberg to be among the handful of potential buyers in the data room for the auction for the failed bank. Offers were due Sunday morning, with the FDIC to valuate whether a full sales or break-up is the best option depending on whether any bids come in.

On Friday, the Fed released data showing banks borrowed $165b, around $150b from the traditional discount window and $12b from the new emergency loan programme. Almost all of the borrowing came from the New York and San Francisco Fed districts. In addition, there were new loans of $143b to the new FDIC-owned banks that the FDIC set up to cover depositors of the failed Signature Bank and Silicon Valley Bank. In total, assets on the Fed’s balance sheet rose by about $300m, this expansion over the week unwinding about half of the Fed’s quantitative tightening programme so far.

Economic news Friday saw the University of Michigan’s preliminary March Consumer Sentiment Index fall to 63.4 from 67.0 (67.0 expected) seemingly driven in large part by the regional US banking crisis. Of comforts to Fed officials, 5-10-year inflation expectations slipped to 2.8% from 2.9% – so near the bottom of the 2.7-3.1% range since mid-2021, albeit the Fed would doubtless rather see this closer to the 2.5% pre-pandemic average – something which will require more significant falls in (current) food and energy inflation than witnessed of late.

US industrial production was flat in February against a 0.2% expected rise, through January was revised from flat to 0.3%, so on net much as expected. In Europe final Eurozone core CPI was unchanged from the 5.6% preliminary read, headline revised down to 8.5% from 8.6% – both as expected.

In China, the PBoC on Friday evening announced a 0.25 percentage point reduction in the reserve requirement ratio (RRR) and which will apply to most banks from March 27. It last cut the RRR, by the same amount, last December. The move isn’t see likely to lead to a fall in bank lending rates but will improve banks’ profitability and at the margin make then better able to extend loans and so at least maintain the recent pick up in loan growth rates. The PBoC made clear in announcing the cut that it does not intent to flood the market with liquidity.

As for markets and following Thursday’s 50bps ECB rate hike but dropping of forward guidance on likely future actions, money market pricing for the upcoming Fed (Wednesday) and BoE (Thursday) meetings continues to bounce around . For the Fed, a 25-point rate rise is still the most expected outcome but priced at just 59%. This is in line with a large poll of traders and analysts in which this scribe participated and released on Saturday, which shows an average 60% probability of a 25-point move among those surveyed between March 13 and March 16, with a 27% average chance of no-change and 10% chance of +50bps. For those who completed the survey earlier, so prior to last week’s banking sector turmoil, the probability of no change was put at just 5% and of a 50-point move 36%. The consensus is for 25-point moves out of both this week’s then the May meeting, with rates than held at the assumed 5.0-5.25% terminal rate throughout 2023. The latter is sharply at odds with money market pricing which on Friday night had the Fed’s terminal rate at just 4.79% and 100bps of cuts by year-end.

For the Bank of England, the market has now got 12bps of tightening priced, such that the decision on whether or not to lift Bank Rate by 235bps is seen to be a line ball call. This is indeed NAB’s take, but we (just) lean towards no change this week. See our BoE preview from Friday (“BoE to take a pass this week and instead look ahead to early May meeting”). There remains near universal expectation the SNB will go ahead and lift its main rate by 50bps to 1.50%, also on Thursday.

Extreme bond market volatility was again present, globally, on Friday. The failure of the mid-week actions by the SNB and US regulators to shore up the likes of First Republic’s or Credit Suisse’s share prices more than monetarily, means that financial stability concerns and their potential implications for central bank policy contuse to drive strong demand for shorter dated government bonds. US 2-year notes lost 32bps Friday to 3.84%, down exactly 75bps on the week. 10s were down 15bps Friday to 3.43% for a weekly loss of 27bps. This curve re-steepening (reduced inversion) in the last week or so is consistent with US recession starting about now, albeit nowhere to be seen in latest economy data. German benchmark binds saw 10s down 18bp Friday for a 40bps weekly fall, and 2s down 22bps for a 71bps loss on the week. In Australia, including Friday night’s 7.5bps drop in futures-implied yields, 10s are down 27bps on the week.

In currencies, outright falls in US Treasury yields continue to be more influential on the USD than what is happening with yields spreads, which in the case of the Eurozone are moving against not in favour of EUR/USD. Renewed – and rising – confidence in the Fed cutting rates this year and well ahead of any other central bank is evidently in the driving seat, for now at least overriding the otherwise USD-positive impact of deteriorating risk sentiment. Doubtless if risk aversion develops a much bigger head of steam, this would then come to dominate USD price action. This is turn would snuff out the AUD’s fledgling rally off the 0.6565 10 March low, though we would note that USD/CNY back blow 6.90 is an independent source of AUD support at the moment. AUD/USD briefly got back onto a 0.67 handle Friday (high of 0.6725) before ending the week at 0.6697. Elsewhere in G10, JPY is ruling the roost, USD/JPY subject to downward pressure from both the sharp fall in US bond yields and risk aversion, down 1.4% Friday and 2.4% on the week.

Being the first market to open in the APAC region post the UBS-CS takeover news, initial response has been a ‘risk positive’ one, seeing gains of more than 0.5% for both AUD and NZD in Wellington, and USD/JPY gaining about half a percent.

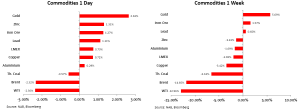

Finally, in commodities heightened far of recession induced demand destruction seen oil extend its weekly loss into double digits Friday (Brent -2.3% Friday, -11.9% on the week) while haven considerations together with a fall back in real bond yields in the past 10 days or so is further lifting gold, up 2.6% Friday to $1,989 (highest close since March 10, 2022) and 5.7% up on the week.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.