NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Todays podcast VIX tumbles as investors see the glass half full ahead of FOMC early tomorrow morning Banks lead gains in Equities with HG bond issuance also signalling improvement in risk appetite UST and Bund curves bear flatten as market increases Fed and ECB rate hikes expectations 2y UST jump 20bps, 10y UST gain […]

NZ: Trade balance (ann $b), Feb: 15.6 vs. 15.6 prev.

GE: ZEW survey expectations, Mar: 13 vs. 15 exp.

CA: CPI (y/y%), Feb: 5.2 vs. 5.4 exp.

CA: CPI core (avg of 3 series, y/y%), Feb: 5.4 vs. 5.6 prev.

US: Existing home sales (m), Feb: 4.58 vs. 4.20 exp.

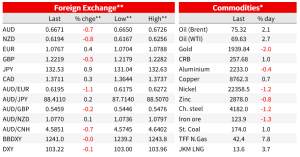

Ahead of the FOMC early tomorrow morning, there has been a notable improvement in risk appetite evident by a big decline in the VIX (fear) index, alongside gains in equities and a flurry of HG bond issuance. Markets are seemingly becoming more comfortable with the idea that authorities have probably done enough to prevent a systemic banking crisis. The improvement in risk appetite has also triggered a repricing of Fed and ECB rate hike expectations fuelling an aggressive bear flattening of the UST and Bund curves. The USD is little changed in index terms, softer against EU currencies, but stronger vs commodity linked pairs and JPY. AUD starts the new day at 0.6665, down close to 1% over the past 24 hours.

It might be early days, but the price action over the past 48 hours is certainly signalling a change in mood by investors. Concerns over banking sector stability have ease following quick initiatives and reassurances by authorities, in particular after assurances from the ECB and BoE investors are now less concern the wipe-out of AT1 bond holders in Credit Suisse represents a source of contagion risk for the broader market. Yesterday during our morning, we also had media reports noting US officials were exploring ways they might temporarily expand FDIC coverage for all deposits. The suggestion here was that official could use the Treasury Department’s authority via the existing Exchange Stabilisation Fund which would avoid the political stress of having to go cap in hand to Congress for help.

The theme of reassurance was then extended overnight with Treasury Secretary Yellen noting the US federal government “is resolutely committed” to mitigating financial-stability risks where necessary, adding that the government could repeat the drastic actions it took recently to protect bank depositors if smaller lenders are threatened.

The reassurances and stability measures provided by authorities in recent days appears to be having an enduring positive effect. Yesterday, the VIX index, which is often use as a gauge of fear, jumped to an intraday high of 28.91 with the market still trying to assess the implications from the Credit Swiss AT1 wipe out. But after jumping higher, the VIX index has now recorded its biggest two-day plunge of 2023 and currently trades at 21.44.

Of note too, after a few High Grade issues on Monday, activity in the US investment-grade bond market gathered momentum overnight with at least nine borrowers, mostly utilities, selling fresh debt. The improvement in market sentiment was also evident by the decline in expected pricing, for instance Bloomberg noted how Metlife is looking to sell a 10-year note at a yield 1.58% over Treasuries, after initial price talks of 1.85% while Republic services was looking at an 11y bond with a yield of 1.45% over Treasuries, after initially bracing for a yield of 1.85%.

US and European equities are stronger too. The Euro Stoxx 600 index closed +1.3%, with a 4% gain for Banks (UBS jumped as much as 10%,). Meanwhile in the US, the S&P500 has been enjoying a steady rise over the past couple of hours and now trades 1.20% higher on the day, Energy and Consumer Discretionary have led the gains up 3.5% and 2.76% respectively. The KBW Banking Index is up over 5% and notably the most troubled large bank – First Republic Bank – is up over 50% on the day, supported by JP Morgan CEO Dimon’s plan to back the bank, with talks of converting some, or all of the $30b in deposits from the 11 major banks last week, into capital.

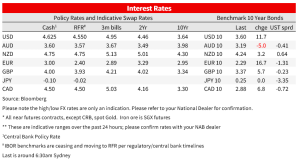

The improvement in risk appetite has also triggered a reassessment of Fed and ECB rate hike expectations. The decline in financial stability concerns means that Central Banks have more room to refocus on their quest to bring inflation to heel and as a result , the market has increased expectation for further tightening over coming months. Ahead of the FOMC tomorrow morning the market has nudged up expectations for a Fed hike to 21bps from 17.6bps yesterday. Similarly, a peak in the funds rate is now seen at 4.90% in June vs 4.73% yesterday. As for the ECB, traders are now betting on 17bps of rate hikes in May compared to as little as 3bps on Monday, while a 3.41% peak rate is priced by September.

The repricing of Fed and ECB rate hike expectations has triggered a decent bear flattening of the UST and Bund curves. The 2y UST yield is up 19bps on the day to 4.17%, while the 10-year rate is up 10bps to 3.59%, both rates near their highs for the session. European rates are up even more, with Germany’s 2-year rate up 26bps and 10-year rate up 17bps.

The USD is little changed in index terms with the DXY trading at 103.23 while BBDXY is at 1240. European currencies have outperformed with the move up in ECB rate hike expectations and gains in Bund yields lifting the euro to 1.077 (up 0.4% over the past 24 hours). NOK gains (+0.8%) can be attributed to decent gains in oil prices ( WTI +2.3%, Brent +1.82).

AUD and NZD have not been able to enjoy the improvement in risk appetite evident in equity and credit markets. The increase in UST yields has been the overwhelming force, boosting the USD vs commodity linked currencies. AUD has been on a steady decline over the past 24 hours with a small rebound in the past hour or so. The AUD starts the new day at 0.6671, after trading to an overnight low of 0.6648. Yesterday the RBA minutes revealed the Bank is looking for an opportunity to pause, though still judged more tightening is needed. The Minutes place a lot of emphasis on the data flow which of course pre-date global developments, the NAB survey and labour market update released last week suggest the RBA should be hiking in April, next week we will get the monthly inflation reading as well as retails sales (both for February), the last two important date prints before the RBA meets early in April.

In a similar fashion to the AUD, the NZD has fallen steadily, down over 1% to be back below the 0.62 mark, currently 0.6194 and USD/JPY is up nearly 1% on the day to 132.60.

Finally, as a cautionary observation vs the improvement in sentiment my BNZ colleague Jason Wong notes the Bank of America’s latest monthly survey of fund managers which shows the biggest fear is seen to be a systemic credit event, replacing inflation as the main worry. The poll showed the most likely source of a credit event is US shadow banking, followed by corporate debt and developed-market real estate. On a similar theme, the WSJ has two articles, one outlining the anxiety in the $8 trillion Mortgage-Backed Securities market, where banks are nursing large losses if they were marked-to-market. The second article noted the record commercial mortgages expiring in 2023 ($270b), and where smaller banks hold $2.3 trillion of such debt. Rising defaults could force mark-downs on these total debt holdings, reducing the capital adequacy of the smaller banks.

For the record, in economic releases, US existing home sales for February were much stronger than expected, rising 14.5% m/m, breaking a record string of 12 monthly declines. The monthly selling price fell 0.2% y/y, the first annual decline in pricing in 11 years. Canada CPI inflation fell by more than expected to 5.2% y/y, with the average of three core measures falling to 5.4% y/y. The data support the BoC’s recent decision to pause the rate hike cycle.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.