Long-term signal vs. Short-term noise

Insight

Ahead of the July US CPI release tonight US equities closed on the back foot. Oil prices extend recent gains while LNG prices surge following news Australian workers vote to strike. Quiet night in FX land.

NZ: Card spending total (m/m%), Jul: -0.9 vs. 1.3 prev.

NZ: RBNZ 2yr inflation expectations, Q3: 2.83 vs. 2.79 prev.

CH: CPI (y/y%), Jul: -0.3 vs. -0.4 exp.

CH: PPI (y/y%), Jul: -4.4 vs. -4.0 exp.

Ahead of the July US CPI release tonight US equities closed Wednesday’s session on the back foot. Big tech were the underperformers while Energy stocks outperform. Oil prices extend recent gains while LNG prices surge following news Australian workers vote to strike. The UST curve flattening theme continues aided by a solid 10y Auction. Quiet night for FX, strong CNY fix helps AUD and NZD after soft China inflation numbers.

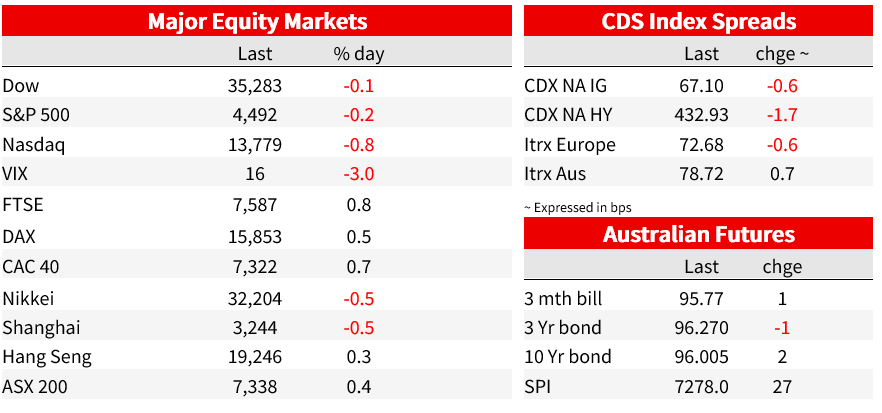

After a down and up opening session, US equities turned south again before the close with all three main equity indices closing in the red. The Dow fell -0.54%, the S&P 500 was -0.70% and the NASDAQ -1.17%. Big tech were the notable underperformers (IT sector -1.51%) with Nvidia falling ~5% while Tesla, Apple and Amazon fell close to 4%. Energy stocks (sector +1.22%) on the other hand were the outperformers supported by further gains in oil prices. Earlier in the session the Eurostoxx 600 closed 0.43% higher with energy share leading the gains while financial also recovered after Italy issued a clarification of its new tax on banks’ windfall profits, saying the impact may be limited for some banks and the levy won’t exceed 0.1% of a firm’s assets.

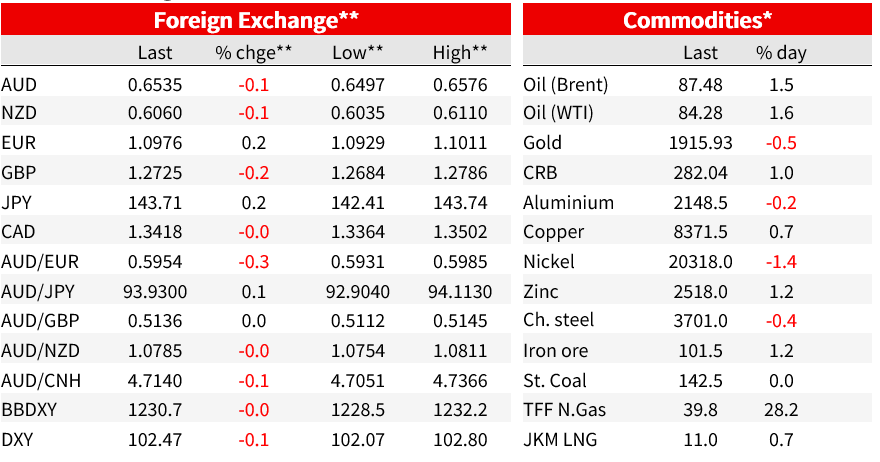

Oil prices gained for a second day with WTI (1.62%) closing the session above $84, breaking above previous high while Brent (1.41%) closed at $87.40. Bloomberg notes prices have been supported by the risk to Russian flows from the Black Sea after Ukrainian President Volodymyr Zelenskiy said his country would retaliate to prevent the OPEC+ producer from “blocking our waters.”

LNG prices have also stolen some of the headlines with European TFF prices jumping 28% following news Australian workers at Woodside and Chevron’s LNG facilities voted to strike on Wednesday, Reuters notes that collectively monthly exports from the facilities equate to around 11% of exports globally, highlighting the risk of a supply squeeze as we head towards winter in the northern hemisphere. The AFR noted about 99% of 180 production employees at Woodside’s facilities voted for action, including indefinite strikes, and they shall be soon joined by hundreds of other employees at Chevron’s facilities. Strikes could start as early as next week.

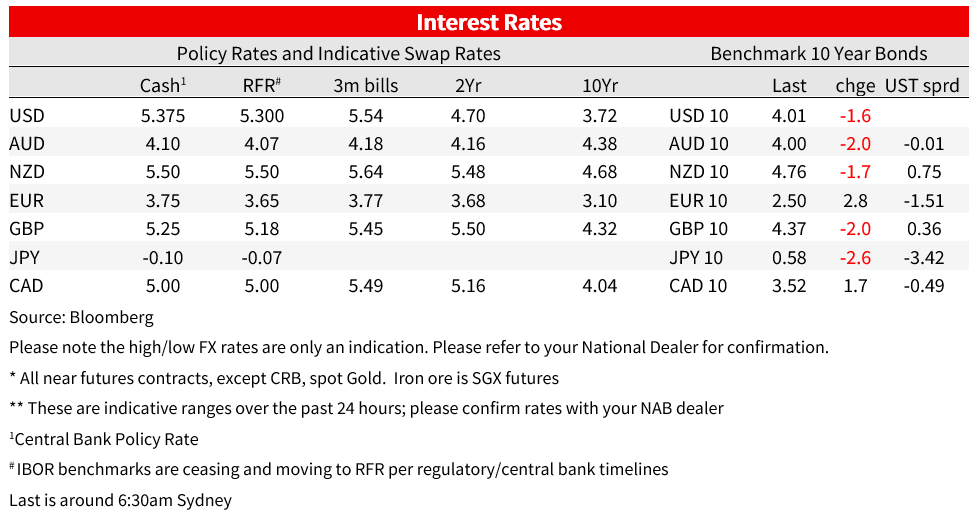

Amid a lack economic news, focus on the UST market remained on the supply side after issuance concerns last week contributed a rise in 10y UST yields up to 4.20%. Some of these concerns eased overnight with the $38 billion 10-year Notes auction showing signs of solid demand . The auction was well supported with bid cover ratio of 2.56. The treasury curve flattened on the day with the 2-year yields increasing 5bps to 4.80%. German 10-year bunds were up 3bps to 2.5% reversing some of the previous days large rally.

Moving onto FX, the USD is little changed in index terms, (DXY -0.04% and at 102.49 while BBDXY -0.03% at 1230.9). European FX edged a little bit higher with NOK leading the gains, up 0.63%, supported by the gain in oil and LNG prices. The euro climbed 0.18% but remained below the 1.10 mark (now trading at 1.0974).

A stronger than expected USD/CNY fix and reported selling by Chinese state banks yesterday provided support to the AUD and NZD in the Asian session. CNY managed to gain 0.11% over the past 24 hours (USD/CNY at 7.2103) with the strong fix offsetting underwhelming deflationary news. China’s CPI and PPI for July fell together for the first time since 2020. CPI fell 0.3% y/y which is the first decline since February 2021. Producer prices also fell for a 10th consecutive month contracting 4.4% y/y. Details were not as bad as the headlines with core inflation, which is a better guide to underlying price pressures, revealing a rise from 0.4% y/y to 0.8%, its highest since January and broadly in line with its 2022 average. Still subdued price pressures underscore how underwhelming the domestic recovery has been and highlight the need for more fiscal support, if Beijing wants to avoid the prospect of a deflationary trap.

The AUD was relatively steady during the overnight session, late during our session yesterday the pair traded to an intraday high of 0.6571, then overnight with US equities opening lower the pair eased down towards 0.6520 and now starts the day at 0.6528, 011% lower relative to levels this time yesterday. NZD/USD reached highs up towards 0.6100 in early Europe but has since retraced back to 0.6052.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.