A private sector improvement to support growth

Insight

After a positive start, US equities struggled for direction amid lingering banking stability concerns. Front end tenors have led a decline in UST yields with similar price action seen in European curves. BoE, SNB and Norges Bank deliver on expected rate hikes. AUD gives back earlier gains as equities struggle.

UK: Bank of England Bank Rate (%), Mar: 4.25 vs 4.25 exp.

US: Initial jobless claims (k), 18-Mar: 191 vs 197 exp.

US: New home sales (k), Feb: 640 vs 650 exp.

EC: Consumer confidence, Jan: -19.2 vs -18.2 exp.

After a positive start, US equities are struggling for direction amid lingering banking stability concerns. US Treasury Secretary clarifies the US government position, saying the US is prepared to provide additional deposit actions if needed. Front end tenors have led a decline in UST yields with similar price action seen in European curves. BoE, SNB and Norges Bank deliver on expected rate hikes. The USD is staging a bit of a come back to be unchanged over the past 24 hours, AUD gives back earlier gains as equities struggle.

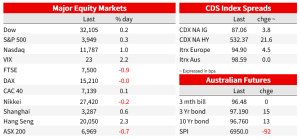

After a positive start that saw the S&P 500 climb 1.8%, US equities turn south with bank and energy stocks leading the decline. Investors remain concern over the outlook for US banks, yesterday US Treasury Secretary Janet Yellen spooked the market when she said that US Treasury Secretary regulators weren’t unilaterally prepared to offer a blanket guarantee. Speaking before lawmakers again overnight, Yellen clarified the government’s position noting US deposits are safe, and a drastic extension of deposit insurance isn’t needed and then added that “Certainly, we would be prepared to take additional actions if warranted.”.

US equities are attempting a late recovery after Yellen’s comments with the S&P 500 now up 0.30% while the NASAQ is +1.01%. Earlier in the session, European equity indices closed mixed with the Euro Stoxx 50 ending the day +0.27% while the UK FTSE 100 was -0.89%.

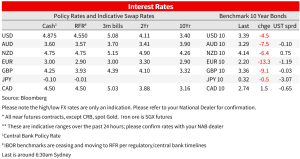

As expected by the rates markets, the BoE lifted the UK cash rate by 25bps to 4.25% and in line with previous guidance left the door open for further hikes of inflationary pressures prove persistent. There were no dissenters with policy makers voting 7-2 for the hike. In the usual letter to the Treasury published alongside the decision Governor Bailey noted that “The committee will continue to act as necessary to ensure that CPI inflation returns to the 2% target.”. As for financial stability concerns, given recent turmoil in US regional Banks and Credit Swiss, the BoE noted that ‘the UK banking system maintains robust capital and strong liquidity positions’ going on to say that the UK ‘banking system remains resilient’.

On inflation the BoE noted that ‘CPI inflation increased unexpectedly in the latest release, but it remains likely to fall sharply over the rest of the year’ . BoE Governor Bailey suggested that there were some signs February’s inflation reading was a ‘one off’. On another day, these observations would have justified a no change outcome, but with headline inflation at 10.4% and core at 6.2%, the Bank was seemingly left with no choice but to hike.

Market pricing continues to see a better than even chance that the BoE hikes another 25bp in May but has trimmed peak pricing closer to 4.5% from the closer to 4.75% seen yesterday. Short end gilt yields initially edged higher after the BoE, before continuing their downtrend to be around 20bps lower on the day, similar to the declines seen in core European yields. 10-year Gilt yields closed 9bps lower to 3.35%, while core European equivalent yields down between 11-14bps. GBP saw some volatility around BoE release and is little changed over the past 24 hours at 1.2285.

The SNB lifted it cash rate by 50bps to 1.5% notwithstanding the issues with Credit Swiss and noted that it could not rule out additional rises in the policy rate to ensure price stability over the medium term. Chairman Jordan in a statement also said that “To provide appropriate monetary conditions, the SNB also remains willing to be active in the foreign exchange market,” adding that currency sales have been the focus.

And then the most hawkish outcome came from the Norges Bank, which not only hiked by 25bp, but also flagged a similar hike in May. Revised guidance in the accompanying Monetary Policy Report showed the Bank now expects a 3.6% peak later in the year.

Moving onto the US rates markets, front end tenors have led a decline in yields across the curve. The 2y rate is down 16bps to 3.781% while the 10y Note now trades at 3.38% after climbing to 3.52% just before midnight. The late recovery in equities after soothing words from Jane Yellen appears to have helped stop the decline in yields with the 10y Note lifting a couple of bps after her new comments.

Earlier in the session, US jobless claims eased down to 191k from 197k previously, so a strong headline level, but the details revealed the number of states whose unemployment claims have risen more than 25% over the past year has climbed to its highest level since mid-2019 suggesting some cracks are appearing in the US labour market.

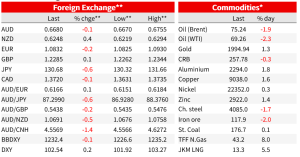

In currencies the USD is still around 0.8% lower than pre-Fed levels, but after trading lower earlier in the overnight session, the greenback has staged a recovery with the DXY index now up 0.20% over the past 24 hours (@ 102.55). Looking at G10 pairs, JPY is the top performer, up 0.6% (USDJPY @ ¥130.60) with the Kiwi not too far behind up 0.42% and now trading at 0.6260.

The AUD is a tad lower relative to levels this time yesterday (-0.8%) and after trading to an overnight high of 0.6755, the aussie start the new day at 0.6685. The euro has also traded in a similar fashion, briefly climbing above 1.09, but now trades at 1.0836, little changed over the past 24 hours.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.