Coming in for landing in a heavy cross wind

Insight

Deutsche Bank woes weighted on European equities and on US equities at the open, but the latter enjoyed a decent rebound before the close. Core global yields ended Friday lower across the board , the USD was broadly stronger , but still fell for a third consecutive week, AUD and NZD were the week’s underperformers.

JN: CPI (y/y%), Feb: 3.3 vs. 3.3 exp.

JN: CPI ex fr. Food, energy (y/y%), Feb: 3.5 vs. 3.4 exp.

UK: Retail sales ex auto fuel (m/m%), Feb: 1.5 vs. 0.2 exp.

GE: Manufacturing PMI, Mar: 44.4 vs. 47.0 exp.

GE: Services PMI, Mar: 53.9 vs. 51.0 exp.

EA: Manufacturing PMI, Mar: 47.1 vs. 49.0 exp.

EA: Services PMI, Mar: 55.6 vs. 52.5 exp.

UK: Manufacturing PMI, Mar: 48.0 vs. 49.7 exp.

UK: Services PMI, Mar: 52.8 vs. 53.0 exp.

US: Durable goods orders (m/m%), Feb: -1.0 vs. 0.2 exp.

US: Durables ex trans. (m/m%), Feb: 0.0 vs. 0.2 exp.

US: Manufacturing PMI, Mar: 49.3 vs. 47.0 exp.

US: Services PMI, Mar: 53.8 vs. 50.3 exp.

Concerns over banks stability continues to be a source of volatility triggering big intraday swings in equity and rates markets. Deutsche Bank came under selling pressure on Friday as investors continue to hunt for the next victim in the current turmoil. Authorities from both side of the Atlantic sought to reassure investors that the banking system remains sound and resilient. DB’s woes weighted on European equities and on US equities at the open, but the latter enjoyed a decent rebound before the close. Core global yields ended Friday lower across the board with UST yields also lower on the day, but well off their intraday lows. The USD was broadly stronger on Friday, but still fell for a third consecutive week, AUD and NZD were the underperformers on the week

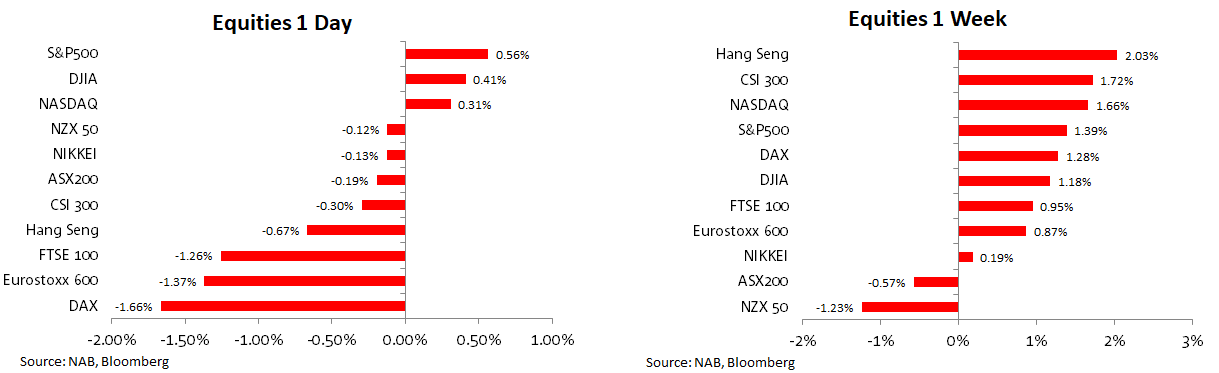

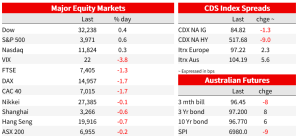

European equities had a torrid Friday with regional indices closing over 1% or 2% lower on the day. Bank shares drove the decline with DB shares at the epicentre of the market rout. Shares of the German bank fell close to 15% intraday with its credit default swaps widening to levels not seen since the start of the pandemic. The sharp decline in DB’s shares prompted German Chancellor Olaf Scholz to call for calm, saying there was no question about the bank’s future. “Deutsche Bank has thoroughly reorganised and modernised its business model and is a very profitable bank,” he told reporters in Brussels.By and large commentary from analysts quoted in the media corroborated the Chancellor’s observation, some analysts called the selling pressure on DB as irrational while others also indicated they were not concerned about DB going the way of Credit Suisse. DB ended the day down 8.5%. The Euro Stoxx 600 index fell 1.4%, led by a 3.7% fall in bank stocks.

The negative vibes from Europe weighed on US equities at the open with the S&P 500 down 1% within the first hour of trading. But then we saw sharp turn around in fortunes with the KWB Banking index leading a rebound . Early in the day Treasury Secretary Yellen convened a meeting of the Financial Stability Oversight Council (FSOC) a panel that includes Fed Chair Powell and the head of the FDIC. After the market close, the Treasury released a post-meeting statement, noting that while some institutions have come under stress, the US banking system remains sound and resilient

Is hard to tell whether the FSOC meeting helped sentiment, but certainly the current volatility in markets suggest investors are looking for more reassurances from authorities. Over the weekend Bloomberg noted that US authorities are considering expanding an emergency lending facility for banks in ways that would give First Republic Bank more time to shore up its balance sheet, according to people with knowledge of the situation. So, after a sharp drop at the start the S&P 500 ended day 0.56% higher with gains led by pharma, health and utilities sectors. The NASDAQ gained 0.31% on the day and gained 1.66% on the week. Of note the Australian and New Zealand equity markets were the week’s underperformers, down 0.57% and 1.23% respectively.

Equities Performance

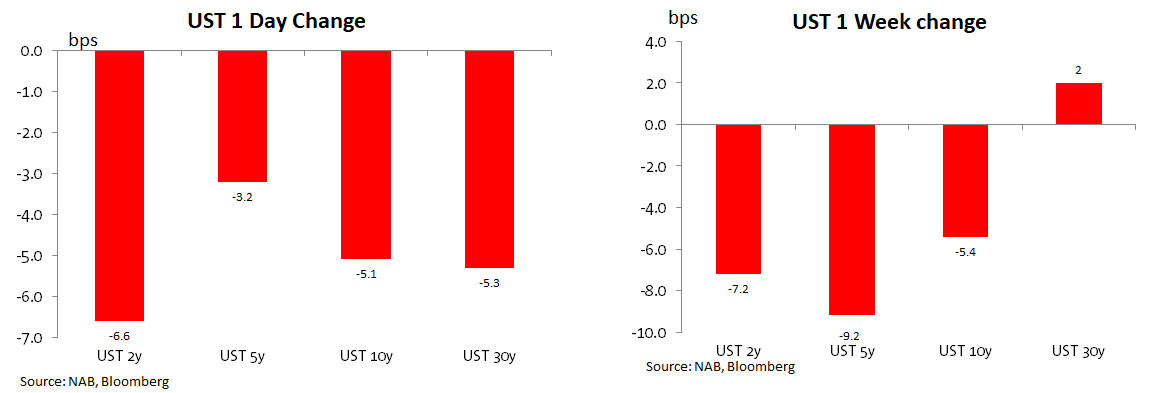

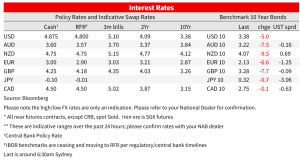

Uncertainty over the banking sector driven by DB’s shares wild swings also triggered some volatility in the rates markets with core global yields lower across the board on Friday. In Europe the 10y Bund yield closed 6.6bps lower on the day to 2.12% while 10y UK Gilts closed 7.7bps down to 3.27%. Meanwhile, the 10y UST yield traded in a 13bps range on Friday, opening the Tokyo session at 3.41%, then trading to an overnight low of 3.28% before closing the day at 3.37%, down 5bps relative to levels on Thursday’s close. The 2-year rate fell to a fresh 6-month low of 3.55% before ending the day at 3.77%, down 7bps. Pricing for future Fed hikes continued to be pared back, with the next with the next May meeting priced at just +6bps, before the chance of easier policy begins to be priced from the June meeting.

Market’s expectation for Fed easing in the second half of this year, highlights how investors have become increasingly concern over a severe US economic slowdown that now has been exacerbated by the likelihood of tighter credit conditions from the current banking woes . In contrast, speaking on Friday and over the weekend, Fed speakers express confidence on the macro prudential tools implemented to stabilise the banking sector while also defending the decision to lift the Funds rate to 4.75%-5%, given the need to curb high inflation despite concern over banking strains. Inflation is high. Demand hadn’t seemed to come down. And so, the case for raising was pretty clear,” Richmond Fed President Thomas Barkin was quoted as saying in an interview with CNN. “Continued appropriate macroprudential policy can contain financial stress, while appropriate monetary policy can continue to put downward pressure on inflation,” Bullard said in St. Louis.

Of note Bullard, who has been very good at calling the Fed hiking trajectory in this cycle, said that he raised his Fed Funds projection to 5.625% for 2023 , consistent with three more rate hikes this year and putting him in a group of three members at that rate, but not as high as the most hawkish member who projected a fourth additional hike. Bullard said there could be a downside scenario (with a 20% probability) where financial stress gets worse, but that wasn’t his base case.

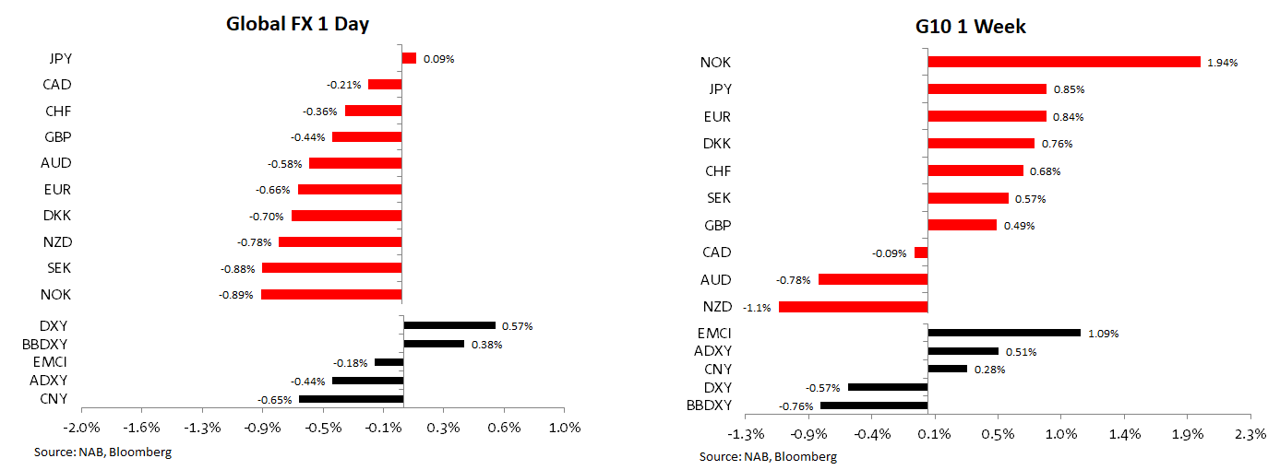

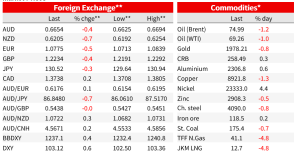

Moving onto currencies, the USD was broadly stronger on Friday with JPY the only G10 that managed to outperform the greenback . USD/JPY edged 0.10% down to ¥130.6 with the move lower in core yields favouring JPY. On Friday Japan inflation release for February revealed a welcome decline in the headline reading, helped by the government energy subsidies. But more importantly from a BoJ perspective the rise in the core core reading (ex fresh food and Energy) showed underlying price pressures are still rising, indeed for the core core reading this was the fastest pace of inflation in over four decades. In our view the data is yet another piece of evidence that suggests the BoJ ultra-easy policy is inappropriate and counterproductive. Our base case is that YCC will be abolished by the middle of the year, after the Bank has details from wage spring negotiations ( Shunto and Rengo), but inflationary pressures may force Governor Ueda to act sooner. Tokyio’s CPI on March 31st is going to be an important data release to watch.

With attention on Deutsche Bank, the euro was the weakest of the key majors Friday night, falling from 1.0830 to 1.0760. That said the Euro did manage to climb 0.84% on the week and from a technical perspective the pair has room to retest 1.10 again. Looking at other European pairs, NOK was the big underperformer on Friday, down .89%, but on the week it was the strongest G10 pair, up 1.94% after the Norges Bank surprised with its hawkish rhetoric.

Heightened equity and rates market volatility, symptomatic of risk aversion, did not help the AUD and NZD at the end of last week. NZD fell 0.78% on Friday and was the biggest underperformer on the week, down 1.1%, the kiwi starts the new day just below 0.62. The AUD fell 0.58% on Friday and lost 0.78% on the week, the second worst performer on the week. The AUD also had to contend with softer iron ore prices (more below) and starts the new week at 0.6655.

Economic data data continue to play second fiddle to the bigger issues facing the market , but for the record, the NY Fed’s underlying US inflation gauge slowed to 4.75% in February from 5.1% in January, to reach the lowest rate since October 2021.

PMI data showed Euro area business activity growing faster than expected, driven by growth in the dominant services sector, with weaker growth for manufacturing – the services PMI rising to a ten-month high of 55.6, while the manufacturing PMI dropped to a four-month low of 47.1. Relative strength in services versus manufacturing was also a feature of the US and UK PMIs. There was no sign of the turmoil in the banking sector impacting on activity, although that should come in the face of tightening lending standards.

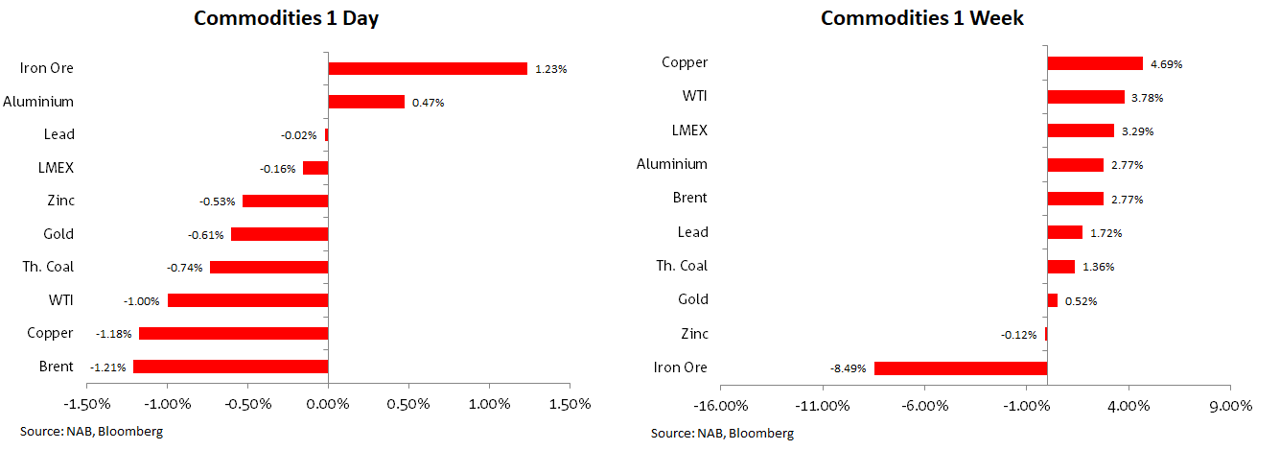

Commodities had a soft end to the week with oil and copper prices down over 1%. Iron ore has remained volatile with the market still trying to ascertain the degree of the demand coming from China. Iron ore gained 1.23% on Friday, but was the weakest commodity on the week, down 8.5% to $ 118.5.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.