Firmer consumer and steady outlook

Insight

There has been little top-level news flow over the past 24 hours, which has seen markets relatively calm by the standards of recent weeks.

There has been little top-level news flow over the past 24 hours, and the lack of any substantive developments in the banking backdrop has seen markets relatively calm by the standards of recent weeks. The US dollar is broadly weaker, with the AUD and NZD up over 0.8%. Yields are generally a little higher, while the S&P500 has closed slightly lower.

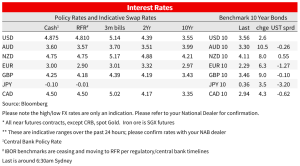

US 2yr yields held a move above 4% amid no further evidence of stress in the banking system. The 2yr is currently around 4.04% after an intraday high of 4.07%, up 4bp on the day. The 18 bp range in the 2yr yield over the past 24 hours the narrowest since 8 March. The 10yr was 3bp higher at 3.56%. The market now prices a fed funds rate 54bp below its current level by the end of the year, from 61bp yesterday. Rates across Europe are also higher, with 2 and 10-year German bunds up 6bps.

In FX markets, the backdrop of little new newsflow has seen the dollar 0.4% lower on the DXY. The AUD was up 0.8% to 0.6706, towards the top of the G10 leaderboard over the day. NZD was 0.9% higher to 0.6251. The Euro was 0.4% higher, while the USD lost 0.6% against the yen to 130.7.

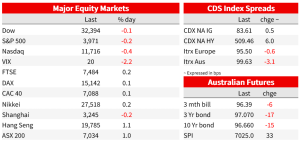

The S&P500 closed only slightly in the red , down 0.2%, after paring losses of 0.6% earlier in the session. IT and communication services led declines in the S&P 500, while the Nasdaq was 0.4% lower. Energy stocks outperformed, up 1.4%, with oil extending gains. Brent oil was up another 0.8% after yesterday’s 4.3% gain. A legal dispute between Iraq, Kurdistan, and Turkey has halted around 400,000 barrels a day of flows, constricting global supplies. Elsewhere, European bourses were generally slightly positive, the Euro Stoxx 50 up 0.1%.

Congress began hearings on recent bank turmoil, with Fed and FDIC official hinting at regulatory and capital rule changes. Federal Reserve Vice Chair for Supervision Michael Barr said, “I anticipate the need to strengthen capital and liquidity standards” for banks with assets larger than $100 billion. FDIC Chair Martin Gruenberg said “ the prudential regulation of these institutions merits additional attention, particularly with respect to capital, liquidity and interest-rate risk.” The ed will enhance stress tests and the FDIC will on May 1 lay out options for potential changes to deposit-insurance coverage.

The St Louis Fed’s Bullard added his voice to the chorus of central bankers making a distinction between the response to financial stability concerns and the response to inflation. “In my view, continued appropriate macroprudential policy can contain financial stress in the current environment, while appropriate monetary policy can continue to put downward pressure on inflation. ” Bullard notes that he finds equity prices are less useful in assessing financial conditions and the impact of monetary policy than credit spreads and the dollar. He also distinguished financial conditions from financial stress, with a rise in financial stress pinned on the fact that “not all financial entities have adjusted their businesses appropriately to the changing interest rate environment.”

To drive home the point further the Fed can’t abandon its inflation flight on fear of financial instability alone, consumer confidence rose. It’s early days for the full impact of credit tightening to be evident for households, but Consumer Confidence suggested the consumer had taken little notice of recent bank failures. T he survey was mostly conducted after the failure of SVB. Consumer Confidence from the Conference Board rose to 104.2 from 103.4, above consensus for 101.0. The gain was in the expectations component, up 2.6 to 73.0, while the present situation index dipped 1.9 to 151.1. On perceptions of the labour market, jobs easy versus hard to get edged down to a still high 38.8. Muddying the picture somewhat is the contrasting signal from the University of Michigan survey released just over a week ago, which dipped to 634 from 67.0. Elsewhere, US January house prices showed a 0.2% m/m gain on the FHFA index and a 0.4% m/m fall on the CS 20-city index, a moderation of earlier declines.

In Australia yesterday, retail sales data showed a 0.2% m/m gain in February , in line with consensus. Looking through the volatility of recent months alongside shifting seasonal patterns, retail spending has been broadly flat at elevated levels since September last year. With some softer goods spending excluding food offset by more robust spending on food and cafes and restaurants. For the RBA, the data shouldn’t argue against a hike in April in the context of strong employment and NAB Business Survey. The Monthly CPI indicator today is the last data point on the RBA’s watchlist ahead of the April meeting.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.