We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

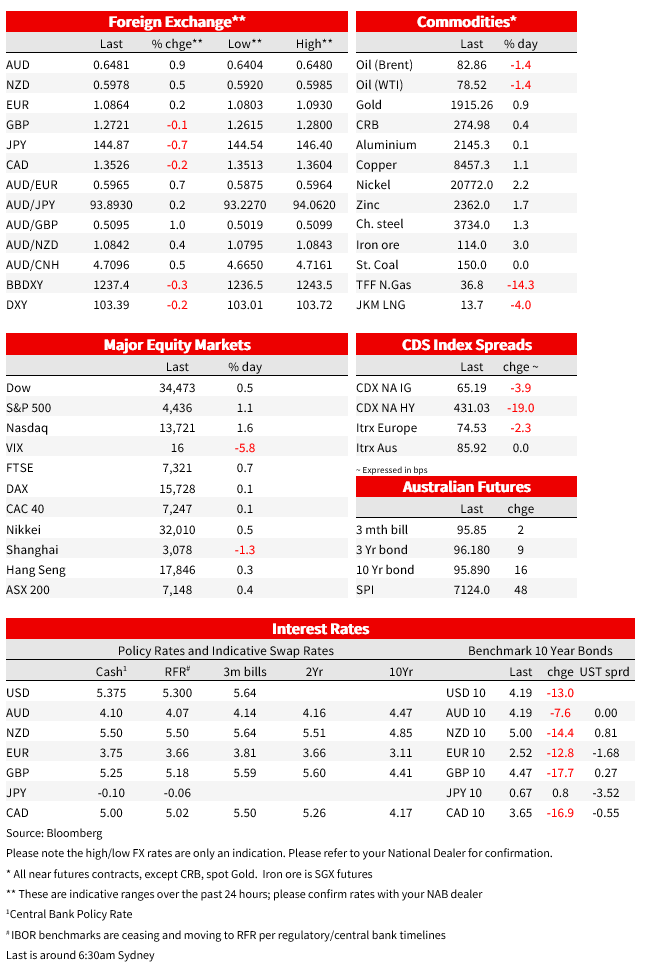

Yields were generally lower globally as PMI data came in softer than expectations, with deterioration most pronounced in German Services. The AUD was stronger, as were US equities, with tech leading once again ahead of much anticipated earnings from Nvidia.

NZ: Real retail sales (q/q%), Q2: -1.0 vs. -0.4 exp.

GE: Manufacturing PMI, Aug: 39.1 vs. 38.8 exp.

GE: Services PMI, Aug: 47.3 vs.51.5 exp.

EC: Manufacturing PMI, Aug: 43.7 vs. 42.7 exp.

EC: Services PMI, Aug: 48.3 vs. 50.5 exp.

UK: Manufacturing PMI, Aug: 42.5 vs. 45.0 exp.

UK: Services PMI, Aug: 48.7 vs. 51.0 exp.

CA: Retail Sales ex auto (m/m%), Jun: -0.8 vs. 0.3 exp.

US: Manufacturing PMI, Aug: 47.0 vs. 49.0 exp.

US: Services PMI, Aug: 51.0 vs. 52.0 exp.

US: New home sales (k), Jul: 714 vs. 704 exp.

EC: Consumer confidence, Aug: -16 vs. -14.5 exp.

Yields were generally lower globally as PMI data came in softer than expectations. German services saw a sharp deterioration, but across the US and Europe PMIs generally pointed to a slowdown. Yields were sharply lower, with the US 10yr down 13bp, matching the decline in 10yr German yields. An initial rise in the DXY on the back of euro weakness was fully reversed, with the DXY down 0.2%. The AUD was 0.9% higher to 0.6481. Equities were stronger, led by tech ahead of much anticipated earnings from Nvidia. Those earnings result out after hours did not disappoint.

European PMIs showed relative resilience in services fading. The preliminary Eurozone services PMI came in at 48.3 from 50.9 and 50.5 expected. The Manufacturing index remained firmly in contractionary territory, but lifted from 42.7 to 43.7, but the balance was a fall in the composite to 47.0 from 48.6. The release followed the lead in from French and German numbers, with the German services PMI doing much of the heavy lifting in the eurozone services outcome, showing a large dip from 52.3 to 47.3. Under the hood, input cost and selling price inflation tick higher due in part to upward wage pressures, but inflationary pressures do remain far lower than much of the last couple of years. The pace of decline goods prices charged moderated. UK PMIs also undershot expectations with the composite index falling into 47.9 from 50.8 in July.

Soft PMIs have seen expectations of a September hike by the ECB pared. The market is now pricing 8 bp, down from 14 bp at the start of the week. Markets will be looking to President Lagarde speaking on Friday at Jackson Hole for further guidance. Bund yields fell sharply across the yield curve with 10-year yields declining 13 bp to 2.52%. 10-year gilt yields fell 17 bp to 4.46% which is the largest one-day move lower since the US banking stress in March.

Declines in European yields were mirrored in the US. 10-year bonds rallied, with yields down 13 bp to 4.19%, while the 2yr yields was 7bp lower at 4.97%. Softer US data didn’t help the cause. US PMIs were also weaker than expected with the composite falling to 50.4 from 52.0 but investors will be looking for confirmation in the more closely watched ISM surveys released at the start of September. July new home sales increased to 714k, a touch above expectations for 705k and leaving the upward trend of the past year and bit intact.

In currency markets, the euro was down around 0.5% following the PMI data, but reversed during the US day alongside a broadly weaker dollar to be 0.2% higher at 1.0863. The dollar was down 0.2% on the DXY, with stronger against only the GBP among G10 currencies, and even there by less than 0.1%. The yen was 0.7% higher, sending USDJPY back below 145 alongside the pullback in yields. USDJPY was asl low as 144.54 overnight but starts our day around 144.87.

The Australian dollar was top of the G10 leaderboard, up 0.9% over the day and currently around its intraday highs. The aussie is currently around 0.6481, its highest since 15 August after an earlier intraday low of around 0.6411. The move higher came alongside the rally in US yields and strength in US equities. The NZD was 0.5% higher. Weak retail sales constrained the Canadian Dollar performance, up a comparatively narrow 0.2% over the day.

Nvidia earnings after hours, which had been the focus of much speculation this week, did not disappoint. Nvidia shares rallied 9% after hours, following a 3.2% rise in the regular session after the company saw Q3 revenue of $16bn against analyst expectations of $12.5bn and provided a stronger than expected outlook for Q3 revenue. Even before the result, equities were higher and led again by tech. The S&P500 rose 1.1%, while the Nasdaq was 1.6% higher in regular hours.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.