Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

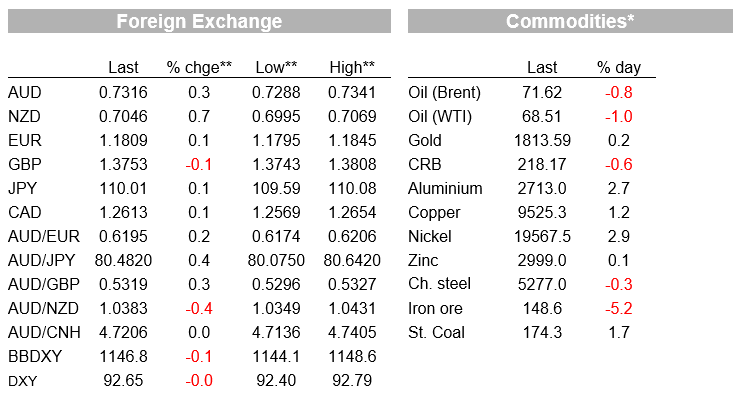

Month end flows interrupt week-long USD depreciation trend but AUD and NZD have done enough work to suggest a base is now in after failing to take a hit from weak China PMI data.

Famous last words perhaps, but we have seen enough by way of positive price action in the AUD and NZD since the 20 August lows to suggest that a base has now been formed for both two currencies. The failure to respond negatively to the weaker than expected China PMI data yesterday morning supports the view that a lot of bad news is now ‘in the price’. Partial reversal of Tuesday’s APAC session gains in overnight markets looked to have been very much a month-end affair that saw across the board demand for US dollars and which should prove inherently temporary.

Earlier Tuesday, around the time Australia was shutting up shop for the day, the USD was under quite intense downward pressure, bolstering our confidence that after a fairly successful attempt by Fed chair Jay Powell last Friday to distance the subject of Fed rate hikes from decisions about tapering QE bond purchases, and before that evidence of a loss of some momentum in the US economy, albeit at least in part covid related, the USD uptrend is over for the time being at least.

Prior to the lead in to the 4pm London time month-end foreign exchange fixings, a little more negative news for the USD – and US bond yields – came from a much softer than expected Conference Board August Consumer Confidence reading. At 113.8 down from a (downward revised) 125.1 in July, this was a lot weaker than expected and corroborates the message from the earlier University of Michigan readings that the US consumer is much less ebullient than earlier in the year.

A combination of higher prices (still much in evidence across a swathe of incoming US data) and doubtless too the resurgence in delta-strain Covid-19 infections – and hospitalisations– are taking a toll. How temporary this will prove to be of course remains to be seen. We also had a softer than expected Chicago PMI print, 66.8 from 73.4 (68 expected) but which is a volatile month-to-month number due to the lumpy nature of Boeing aircraft orders, obviously down in August.

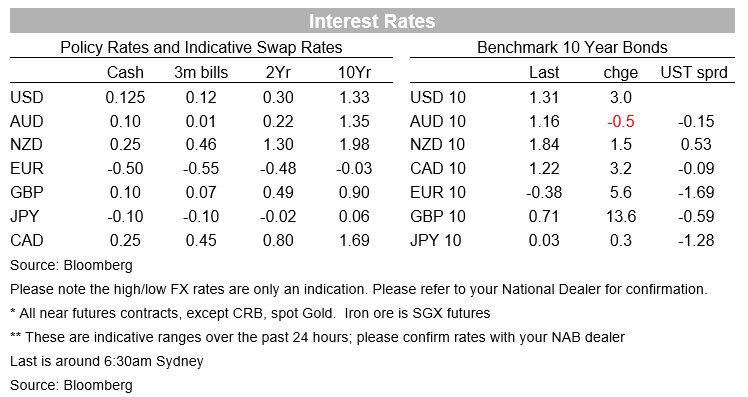

Other economic data to note from overnight included stronger than expected Eurozone August CPI inflation data, headline up to 3.0% from 2.2% previously and 2.7% previously and core to 1.6% from 0.7% and 1.5% expected. Following the data, ECB Governing Council members Holzmann (Austria) and Knot (Netherlands) were both out suggesting that the improvement in the inflation outlook might mean the ECB can afford to add less stimulus, the suggestion being that the full extent of the EUR1.8tn Pandemic Emergency Purchase Programme (PEPP) might not be needed. The 9 September ECB meeting is building up to be an interesting one, including as it will updated ECB staff economic forecasts.

The message from the EZ CPI and subsequent central bank commentary was not lost on the Bund market where 10 year yields rose by 5.6bps. This in turn dragged US Treasury yields higher to end the New York day up 3bps to 1.31%, having fallen to a low of 1.27% in the immediate wake of the aforementioned US consumer confidence data.

Also of note on the economic front, Canada’s Q2 GDP figures came in very much weaker than expected at -1.1% on an annualised basis so about -0.25% q/q, against 2.5% (annualised) expected. This might mean the Bank of Canada defers a further tapering of its QE bond purchases when it meets next week. The numbers took out a bite our of the CAD, down 0.1% overnight versus net gains on the day of 0.7% and 0.25% for NZD and AUD respectively.

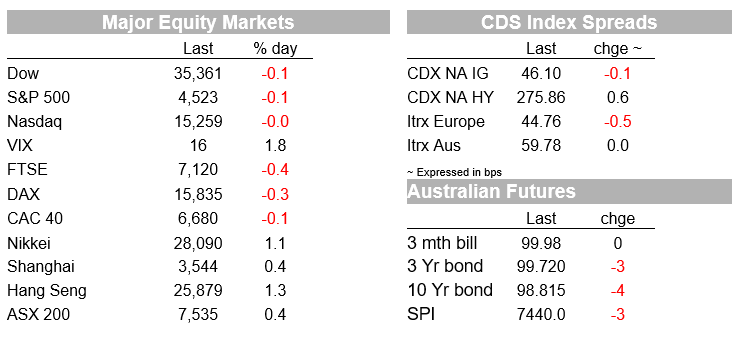

US equity markets were at the weakest early in the New Your session and immediately following the consumer confidence data, but the subsequent intra-day rally didn’t get far and by the close the S&P500 is down 0.13% and the NASDAQ -0.04%. Energy (-0.7%) and IT (-0.6%) were the main drags on the S&P, while Real Estate (+0.6%) and Consumer Discretionaries (+0.4%) performed best. Energy has suffered in conjunction with lower oil prices, WTI crude off 1% or 70 cents. This is despite API inventory data reportedly showing a 4 million barrels draw last week (though a rise in gasoline and distillate stocks).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.