Rising artificial intelligence could see as much as half the work being done today automated within 20 years and organisations need to know how to get ready, an AI expert tells NAB’s Transaction Banking customer event series.

Article

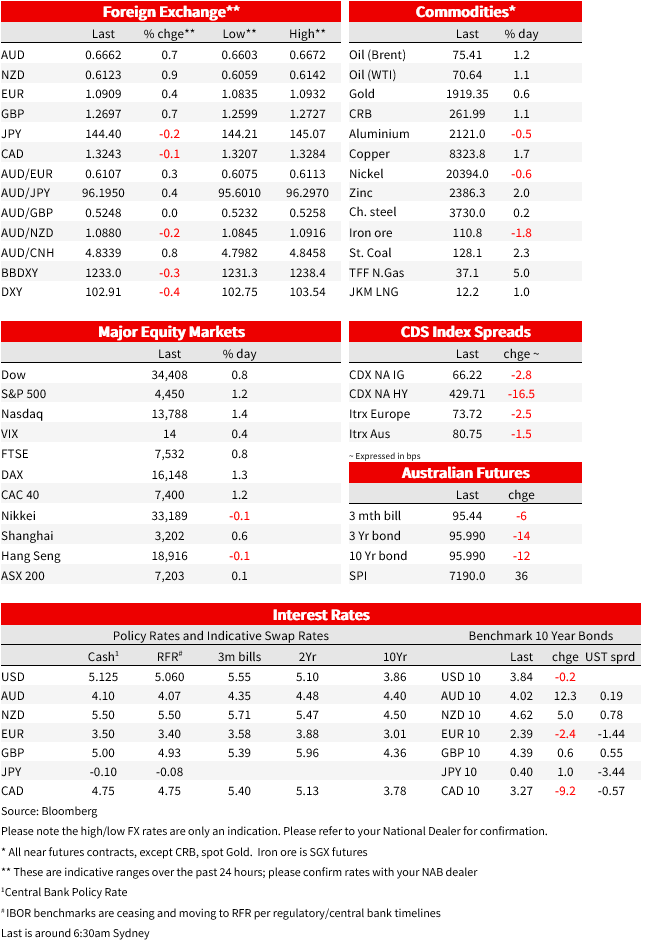

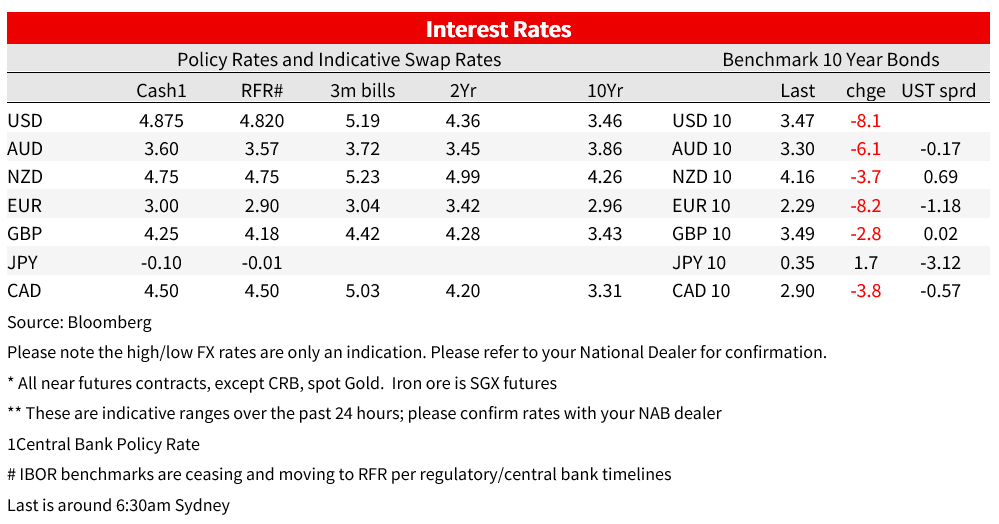

A softer than expected US Core PCE Deflator (0.3% m/m vs. 0.4% expected) helped push yields lower on Friday (US 10yr -8.1bps to 3.47%).

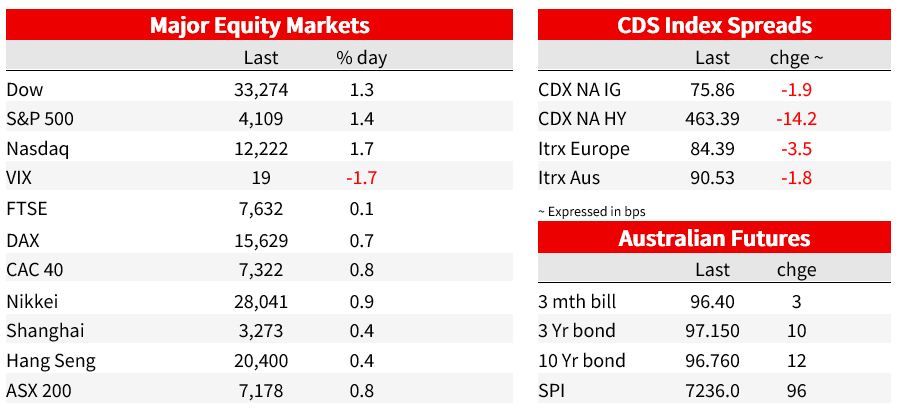

A softer than expected US Core PCE Deflator (0.3% m/m vs. 0.4% expected) helped push yields lower on Friday (US 10yr -8.1bps to 3.47%). Notwithstanding that, markets still price around a 58% chance of the Fed hiking rates again in May which is still being guided by Fed officials, before seeing 61bps worth of cuts in H2 2023. Risk sentiment was positive, buoyed by strong Chinese PMIs (Non-manufacturing 58.2 vs. 55.0 expected, and highest since May 2011), and an alleviation of fears around US regional banks (small bank deposit flows turned positive by 5.8bn after the prior week’s -196.4bn, and on lower borrowing from Fed emergency facilities). Equities rose with the S&P500 +1.4%. Yields as noted above fell with the 2yr -9bps to 4.03% and 10yr -8.1bps to 3.47%. The USD rallied on month end demand with DXY +0.4%. Most pairs were weaker, including the AUD -0.3%. The CAD as exception with USD/CAD -0.2% with Monthly GDP beating (0.5% m/m vs. 0.4% expected, Statistics Canada estimate a 0.3% m/m lift in February which could mean Q1 GDP growing at an annualised pace of 2.8%, compared to the BoC’s projection of just 0.5).

Hitting the wires late last night was headline that OPEC+ announced a surprise oil production cut of 1.1m a day starting next week. The news as lifted commodity currencies with USD/NOK -0.4%; USD/CAD -0.1% and AUD +0.1% in early trade. The production cut, coming at a time of an uncertain global demand environment clearly shows OPEC was not happy with the movement in the oil price which had fallen over recent months. Saudi Arabia said the cuts were a “precautionary measure aimed at supporting the stability of the oil market”. Russia also said its own production cuts it was implementing from March to June would continue until 2023, meaning from July all up there would now be about 1.6m barrels a day less crude on market. Looking to the rest of the week, the RBA and RBNZ meetings will be the key focal point. Then to US Payrolls on Friday, but bond and equity markets will be closed, meaning we will have to wait until next week for the full market reaction.

First to the US PCE data. The Core PCE Deflator came in one-tenth softer than expected 0.3% m/m vs. 0.4% expected; ditto the annual at 4.6% vs. 4.7% expected. The Headline Deflator was broadly as expected at 0.3% m/m, though the annual was 5.0% y/y vs. 5.1% expected. Importantly alternative core measures were encouraging with Powell’s glamour stat of Core PCE Services Excluding Housing at 0.3% m/m and 4.6% y/y, the rate as the Dallas Fed’s Trimmed Mean 4.6% y/y. One word of caution though is that while the monthly figure is encouraging, the level of inflation is still too high. Across the pond Eurozone Core Inflation was as expected at 5.7% y/y, though Headline was softer at 6.9% y/y vs. 7.1% expected.

Regional US Fed President Collins said the PCE inflation figures were roughly in line with what she had expected. Collins also noted that recent banking issues were “likely to see at least some” credit tightening, something she factored in when submitting her economic projections at last week’s meeting. That last remark is important in that some FOMC members had already incorporated some credit tightening into their forecasts. Looking ahead to the jobs report at the end of the week, Collins said it was unlikely to change her outlook. The Fed’s Williams also spoke on Friday, noting the “the economic outlook is uncertain, and our policy decisions will be driven by the data”. Policy right now is in a “ slightly restrictive stance” and “stresses in parts of the banking system are likely to result in a tightening of credit conditions that will in turn reduce spending by businesses and households”. Key will be “the magnitude and duration of these effects, however, is still uncertain.” And Williams “will be particularly focused on assessing the evolution of credit conditions and their effects on the outlook for growth, employment, and inflation”.

As for regional banking indicators, my BNZ colleague Jason Wong notes Fed data showed $88.2b in outstanding borrowing from the Fed’s traditional discount window, down from $110.2 the previous week and $152.9b during the week of peak-distress. Outstanding borrowings at the Fed’s new emergency Bank Term Fund Programme rose from $53.7b to $64.4 over the week. The data suggested that the acute phase of the bank liquidity crisis was over, but the economic impact of tighter lending conditions remains ahead. Commercial bank deposits fell by $126b in the week ending March 22. Deposits for small banks rose $6b after the massive $196b outflow the previous week, and large banks saw an outflow of $90b (although this could reflect a re-categorising of some of SVB’s balance sheet from a large bank to a small FDI bridge bank). In separately released data, market money funds have seen $300b of inflows in the three weeks to March 29, taking a fair chunk of the money leaving the banking system and these large flows pose an ongoing risk to the banking system.

Also out of the US PCE figures were the income and spending figures, which were mixed. Nominal income of 0.3% m/m vs. 0.2% expected, while real spending was as expected at -0.1% m/m. There was other data too, including the Chicago PMI at 43.8 vs. 43.0 expected; still remaining well below the 50 breakeven level. The final-version of the Uni Michigan Consumer Sentiment was revised lower to 62.0 from 63.3, while the inflation expectations were mixed with the 1yr at 3.6% vs. 3.8% expected, and the 5-10yr was 2.9% vs. 2.8% expected.

Finally, China’s PMI suggests we should stop doubting the strength of the economic rebound. The Non-manufacturing PMI rose to 58.2 vs. 55.0 expected, and is now at its highest level since May 2011. The Manufacturing PMI was also solid at 51.9 vs. 51.6 expected. It appears at this stage that the growth target of around 5% should be easily hit. While woes in the property sector remains, the WSJ notes a private indicator of new-home sales showed a second consecutive monthly gain in March – sales at the 100 largest developers rose 29% y/y (see WSJ: .

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Rising artificial intelligence could see as much as half the work being done today automated within 20 years and organisations need to know how to get ready, an AI expert tells NAB’s Transaction Banking customer event series.

Article

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.