We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

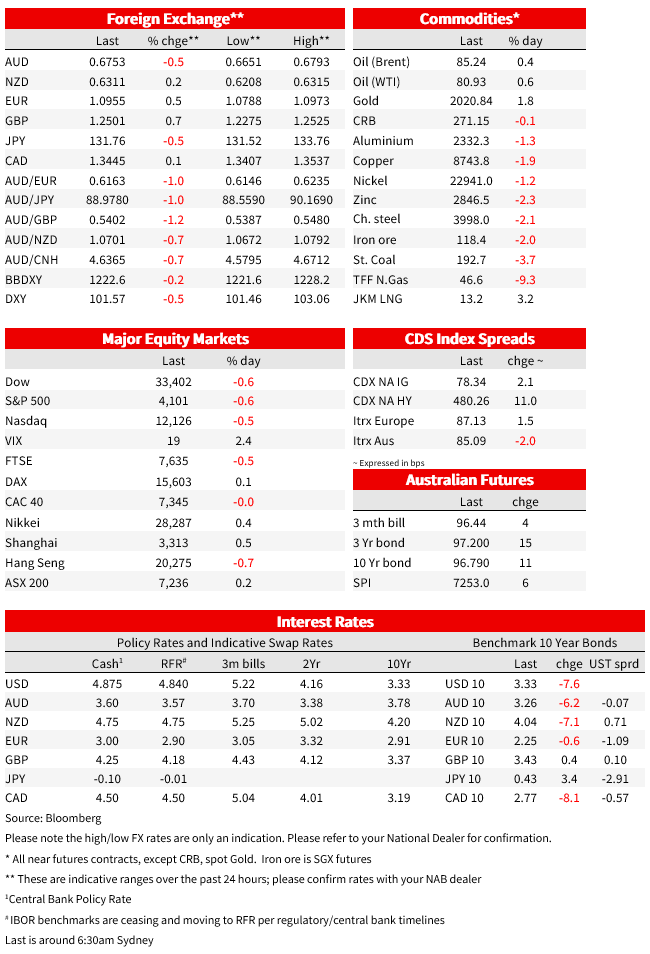

A softer than expected JOLT report shook the market overnight, triggering a bull steeping in the UST. The USD fell with JPY along with European currencies outperforming. Commodity linked currencies lagged the move with AUD the notable underperformer, following yesterday’s RBA decision to pause it tightening cycle. US equities ended a four day rally with pro-cyclical sectors underperforming.

NZ: NZIER Business Opinion Survey

AU: RBA cash rate target (%), Apr: 3.6 vs. 3.6 exp.

US: JOLTS job openings (m), Feb: 9.9 vs. 10.5 exp.

A softer than expected JOLT report provided a shock to the market overnight, triggering a bull steeping in the UST curve with the front end of the curve leading a decline in yields. The USD also fell in index terms with JPY along with European currencies outperforming. Commodity linked currencies lagged the move with AUD the notable underperformer, following yesterday’s RBA decision to pause it tightening cycle. US equities have ended a four day rally with pro-cyclical sectors underperforming on the day. Finland officially joins NATO, triggering furious response from the Kremlin.

The number of US job openings in February fell by 632K to 9.9 million, the lowest level since May 2021 and well below market expectations for a smaller decline of about 300k relative to the unrevised January number. Of note too, the job openings to unemployed ratio, one of Fed Chair Powell’s favourite indicators, also fell to 1.67, the lowest since November 2021. The quits rate (voluntary job leavers as a ratio of employment) edged up to 2.6%, albeit still down from its peak of 3.0%.

The decline in Job openings confirms the softening in US labour demand evident in the Indeed job postings data. The February JOLT figures also confirm US labour demand is trending down with the NFIB survey suggesting further declines should be expected over coming months.

The data triggered a big decline in UST yields with front end rates leading a bull steeping of the curve. The 2y rate declined 12bps on the day to 3.84% while the 10y rate fell about 7bps to 3.33%. Pricing for the next Fed meeting in May edged down to a near 50/50 bet on a 25bps hike. Focus will turn to Friday’s key employment report, where the consensus to picking a further moderation in non-farm payrolls growth to 240k. Tonight the ISM services is also going to be important with any signs of weakness particularly in terms of prices paid, employment and new orders sub-indices likely to favour an extension of the recent decline in UST yields.

The USD also fell in index terms (BBDXY -0.24%, DXY -0.51%) after the JOLT report with JPY and European currencies the outperformers. The pound climbed to a 10-month high (1.2525), up 0.7% on the day and now trades just above the 1.25 mark while the Swiss franc climbed to the strongest since August 2021, up 0.72% over the past 24 hours. The euro also joined the party, gaining 0.53% and opens the new day at 1.0953. The decline in UST yields also favour JPY with USD/JPY down 0.54% to ¥131.71.

Commodity linked currencies lagged the move reflecting their pro-growth sensitives, something that was also evident within commodities with Gold the notable outperformer (+2% to $ 2,020.43) while metals and bulk commodities retreated, Aluminium -1.13% iron ore -1.73%. The AUD was the notable commodity link FX underperformer, down 0.63% relative to levels this time yesterday. The AUD now trades at 0.6752, but of note it has retained about half of the previous day’s gains , relative to the monthly low recorded on March 10 (0.6565), the AUD is still in an uptrend with a break above the 0.6780/90 area the near term challenge if this uptrend can head above the 68c mark. The RBA decision to pause its tightening cycle in April did not help the aussie, the move was broadly in line with expectation but there was a notable tone down in the hawkish guidance by the Bank with prior phrasing of further tightening will be required replaced with further tightening may well be needed. This suggests that the RBA has probably downgraded its forecasts for growth and/or inflation from the February Statement on Monetary Policy when a cash rate of 3.75% was seen as being required to achieve the return of inflation to 3% by mid-2025. Governor Lowe speaks today, just after midday Sydney time with the market hoping he will expand on the Bank’s rationale to pause alongside an update on the economic outlook and policy bias (see more below).

Looking at other commodity linked pairs, NZD has been relatively flat, hovering around 0.63, within an approximate 0.6275-0.6315 range, NOK is down 0.12% while CAD extended it recent gains, up 0.22%.

US equities have closed the day lower with the S&P500 down 0.58% while the NASDAQ is 0.52%. Looking at the S&P 500 sectors, pro-cyclical shares are the notable underperformers with industrials down over 2% while Energy, materials and financials fell between 1% and 1.5%. Earlier in the session, European equities closed mixed with gains and losses between -0.5% and +0.25%.

In other news, Finland officially joined NATO on Tuesday. The WSJ noted Russian Defense Minister Sergei Shoigu told a military conference in Moscow that the West was escalating its confrontation with Russia. He reminded participants that Belarus would soon have the ability to strike enemy targets with tactical nuclear weapons after Mr. Putin said last week that Moscow planned to base the Iskander-M missile system there. While Kremlin spokesman Dmitry Peskov separately told reporters that Finland’s accession to NATO compelled Moscow to take unspecified countermeasures to ensure its security.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.